Short-term and long-term effects

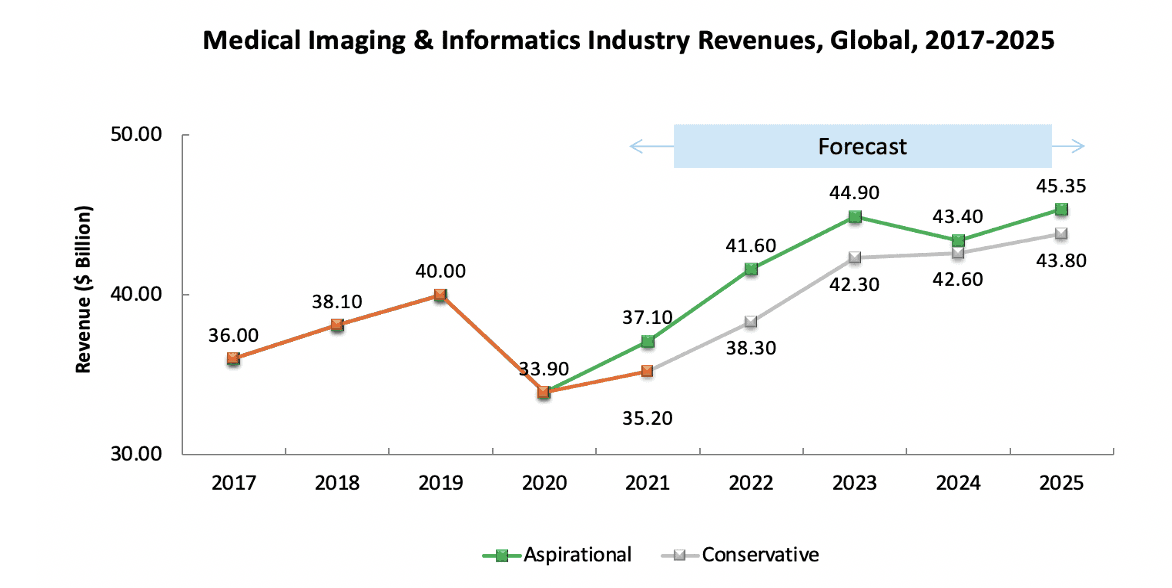

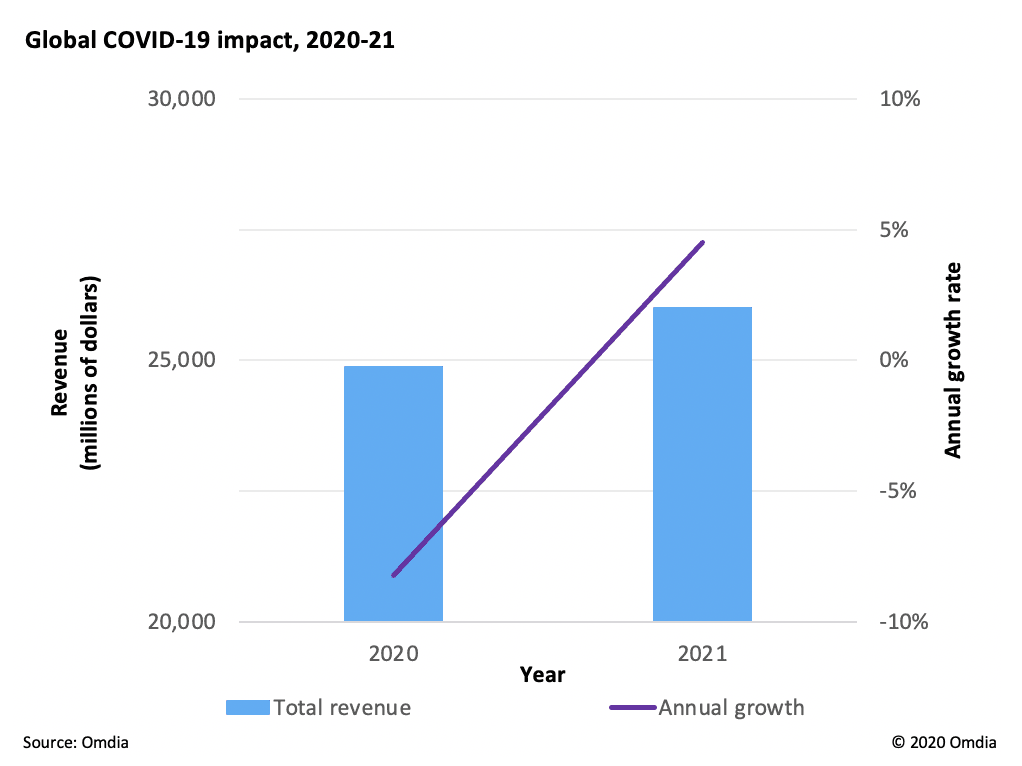

From 2017 to 2019, the medical imaging industry was growing and adding US$2 billion every year, according to Frost &. Sullivan. However, due to the pandemic in 2020, there was a drop of about 15 per cent in revenue.

Most hospitals that have been affected by the pandemic are financially struggling. There is a drop in the gross margins for hospitals which have impacted capital expenditure planning and budgeting. Due to the pandemic, hospital budgets were diverted away from nonessential equipment to increase spending on COVID-19 related equipment.

Procedural volumes reduced significantly, as people started avoiding visiting medical facilities due to the fear of contracting the virus, thereby causing huge losses for hospitals. Government shutdowns also caused severe supply chain disruptions.

Medical imaging equipment roughly occupies about 50 per cent of a hospital’s capital expenditure budget. With the number being so heavy, most hospitals will look at not spending a big chunk of their budgets on medical imaging, which is one of the topmost areas where hospitals look to cut costs.

The current situation is uncertain, with countries like India battling its second wave. How will this impact the consumption or the procurement of medical imaging will depend on the pandemic. Considering all of these factors, Frost & Sullivan has given an aspirational range, an optimistic view, and a conservative range, which is a pessimistic view. The imaging industry’s growth trajectory will most likely be within these two ranges.

Source: Frost & Sullivan

As per the aspirational scenario, after witnessing a drop in revenues in 2020, the medical imaging industry is likely to achieve 85-90 per cent of 2019 market revenues in 2021.

Until 2022, the medical imaging industry won't reach the highest levels it did in 2019. Post that the market will continue to grow. There could be a minor drop in 2024, which is cyclical in nature, with hospitals sometimes delaying purchasing imaging equipment.

Due to the pandemic, Original Equipment Manufacturers (OEMs) are continuing to revise guidance every quarter based on the previous quarter's performance, therefore making it difficult to predict how the market will grow.

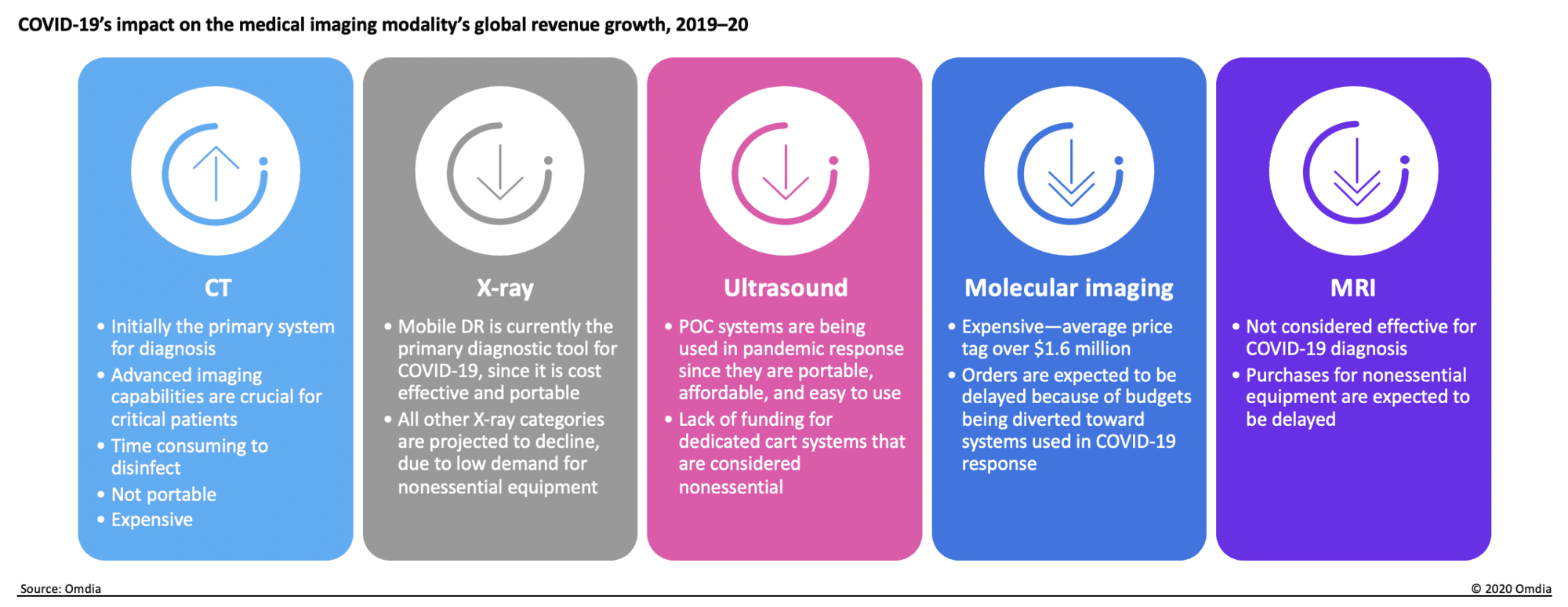

It is important to note that some of the imaging modalities were used for the management of COVID-19 patients. Frost & Sullivan found that digital radiography, CT and point of care ultrasound segments witnessed unprecedented growth (8-15 per cent) in 2020.

A similar trend will be seen in 2021 due to the pandemic persisting in large regions of the globe for a significant amount of time.

These modalities will continue to see positive growth trends. The two modalities that suffered a lot were MRI and mammography. They are expected to gradually return to 75-80 per cent levels of pre-COVID-19 revenues.

Interventional X-ray is expected to reach pre-COVID19 growth, as it is needed to address the pent-up demand for surgeries and procedures. It is a modality that is primarily used in operating rooms and helps in guiding the surgery. Because many elective procedures were delayed or postponed in 2020, the buying of this modality also suffered. But there is only a certain limit to which elective procedures can be postponed. The cases will start to pile up and there will be a greater number of patients who would need urgent care. This will give rise to a demand for interventional X-ray.

Moreover, most hospitals would be looking towards informatics as this will assist the radiology department in cutting costs. Informatics provides the data, analysis, and insights about how well a department is doing and utilising its assets and how productivity can be improved. To track all of this there is an increased need to invest in informatics. The demand for technologies such as enterprise imaging will be highlighted in the post-pandemic period. It is the route for achieving efficiency and will play a key role that will lead to the better performance of the segment.

Hospitals have had to take countermeasures to limit the virus spread, which has impacted the medical device market. These include:

Disinfection of scanning areas and equipment – This has slowed patient volume, as the procedure takes longer.

Modification of the working environment

Accessibility to appropriate personal protective equipment (PPE)

Monitoring of radiographers' health

Suspension of system installations – To stop the spread, nonessential work, including on systems in the early stages of installation, was suspended. This measure is forecast to drive a significant decline in unit shipments.

Furthermore, the COVID-19 outbreak is affecting supply chains and disrupting manufacturing operations around the world. In Western Europe, a primary concern faced by medical suppliers has been the logistical challenges caused by the driver shortage and assurance of the health and safety of the available drivers and their infrastructure.

The pandemic has caused manufacturers to pivot their manufacturing capabilities toward critical care systems to meet the high demand.

According to Omdia, as markets stabilise, much of the pent-up demand from delayed equipment purchases in 2020 will be met in 2021 and 2022. Procedural volumes are expected to rebound as patients return to normal healthcare routines.

Also, governments are expected to increase expenditure to revamp healthcare infrastructures to safeguard against future pandemics.

Some of the challenges that are likely to arise include the fact that healthcare providers will most likely face severe budget constraints owing to the elevated spending to combat the pandemic. Moreover, the resurgence of cases in many nations will hinder the recovery process by forcing healthcare systems to continue to divert resources to address COVID-19 patients. Also, delays in the vaccine approval process and vaccine distribution challenges are set to increase the length of the pandemic.

According to Frost & Sullivan, the postponement of procurement in the pandemic years can lead to higher purchasing in subsequent years leading to a US$45 billion market in 2025. However, the uncertainty of the pandemic re-emerging in sequential waves can create a permanent dent in the sales leading up to US$43.8 billion in annual revenues in the year 2025.