NHF Snapshot

Market Outlook

What the hog crush spread is telling us in front of harvestBy Domenic Varricchio

As we approach harvest, hog producers should be thinking about potential feeding margins on the horizon. I like to look at what the board says hog feeding margins are into next year. The CME provides hog producers the ability to hedge feeding margins by using what’s known as the hog crush spread.

The relationship between the purchased inputs value and the sold finished hog value is known as the gross feeding margin (GFM). This gross feeding margin can be hedged/traded by combining the following futures positions: long corn, long meal and short hogs. That’s known as a “hog crush spread.”

Note that hog crush spreads don’t take into account some variable factors such as rate of gain, operating overhead, death losses, transportation, additional ration ingredients and veterinarian bills. When this hog crush spread position is taken, a producer is betting that feeding margins are at a profitable level and that the spread between grain inputs and hog value will narrow. As the spread narrows (declines), the hedger makes money.

A reverse hog crush spread would be selling corn, selling meal and buying hogs. In this instance a hedger/speculator would be betting that hog feeding margins improve. The reverse hog crush spread makes money when the spread widens (goes up). This means hog values are gaining versus their grain input values.

In their research and product development whitepaper labeled “An Introduction to Hog Feeding Spreads” by Jack Cook, the CME recommends using the following ratio of grain inputs to hog values. They assume one part soymeal (100 tons or 200,000 pounds) coupled with three contracts of corn (15,000 bushels or 840,000 pounds) will produce the equivalent of seven lean hog futures contracts (280,000 pounds). For our purposes, we’ll consider the June25 hog crush spread, which consists of three March25 corn contracts, one March 25 Soymeal contract and seven June25 lean hog contracts.

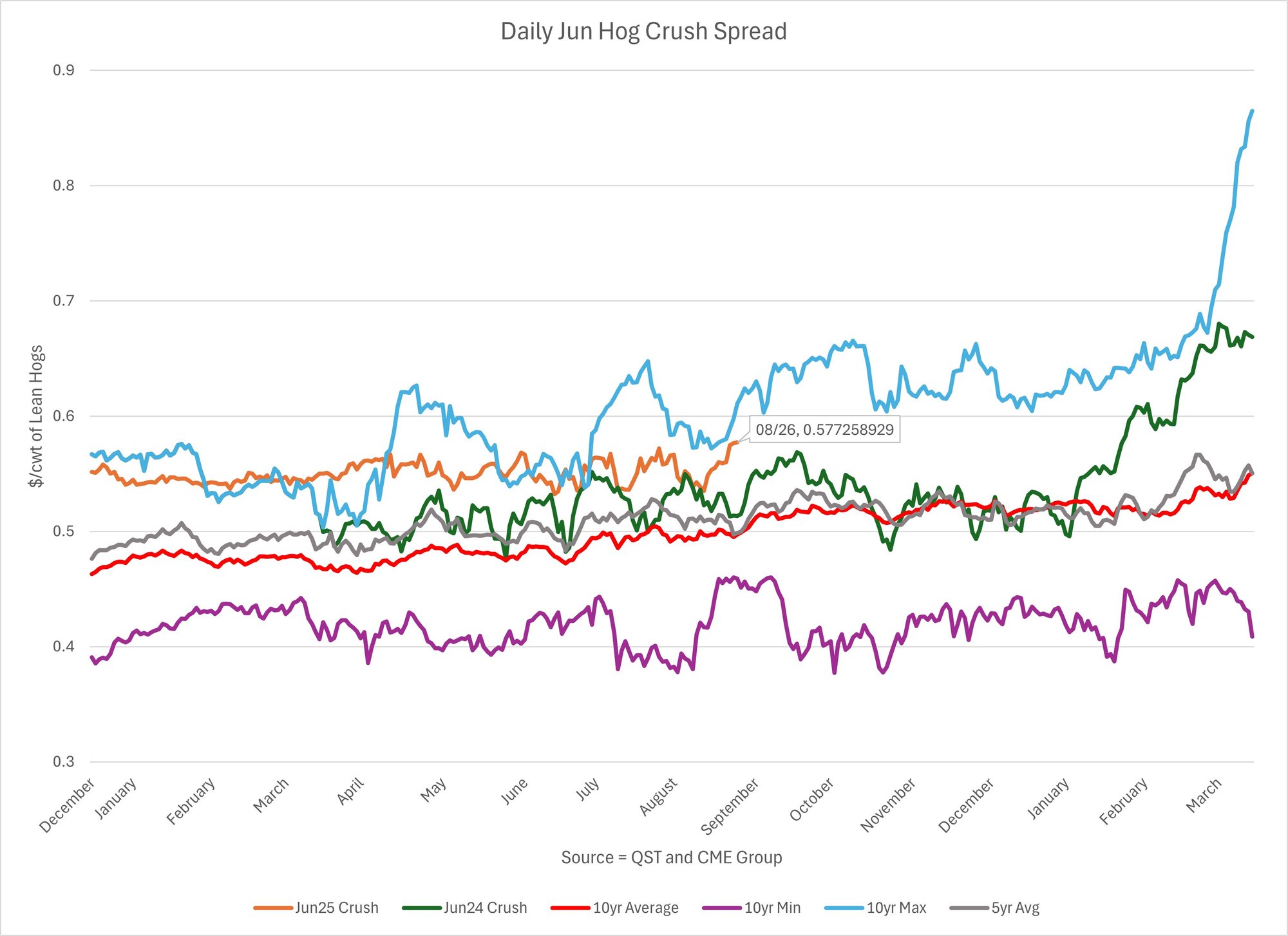

Before reading on, let’s remember that the hog crush spread is really a gross feeding margin spread. The higher the spread, the more margin there is to feed hogs. I quote it in $/hundredweight of lean hogs. The June25 hog crush spread is trading at the second highest level in 10 years as of Aug. 26, 2024. It is at $0.5773/cwt. Only 2015 offered a better feeding margin at this date on the calendar, which was $0.61/cwt.

The 10-year average for the June25 hog crush spread at the end of August is around $0.497/cwt. The 10-year median price for the June25 hog crush spread at the end of August is around $0.483/cwt. These statistics show us that the current June25 hog crush spread is around $0.08 to $0.10/cwt above the long term average and median price.

The market is paying producers more to feed hogs into next summer. Put another way, grain prices look cheap relative to June25 hog prices. With this conclusion, hog producers have a decision to make: is it time to lock in feed needs? With a potential La Nina weather pattern developing for the winter, South American grain production may not be as large as last year. Additionally, the Black Sea corn crop has seen a terribly hot and dry growing season.

As we move past harvest here in the U.S., it is this writer’s opinion that grain prices run a bigger risk of going up from these levels over time. The hog crush spread reinforces this conclusion at these current lofty levels. Combines will soon tell us the size of the U.S. crop and the USDA’s current guess is for a record national yield of 183.1 bushel/acre. Has the U.S. corn crop gotten as big as it will get on paper? Or do big crops get bigger into harvest? At the time of this writing March25 corn and soymeal are at contract lows at $4.06/bu and $304/ton. June25 lean hogs were trading at a one month high of $90.50/cwt.

The chart on the next page shows the Jun25 and Jun24 crush spreads as the orange and green lines respectively. Last year saw the crush spread peak out at the $0.57/cwt level around Sept. 20. It then broke down to carve out lows on Oct. 24 at around $0.484/cwt. On its surface this seems like a small swing in margins, but remember, we’re accounting for 280,000 pounds of hogs, so that was actually a $28,000 swing. (280,000 x .1) What’s that mean for your bottom line?

As we advance into harvest, hog producers should keep their feeding margins in mind. Higher crush spread levels can influence changes in feeding decisions and sow retention decisions. If we see the June crush continue to head higher, my guess is that we start to see more sows held back for breeding. This may lead to larger than expected hog supplies down the road.

At Pluto Commodities, we track these hog crush spreads daily. Like an alarm clock, we text out our hog market commentary every day at 7 a.m. to keep our customers informed. We turn our customers into confident hog marketers by offering daily and weekly commentary coupled with Buy and Sell signals. Take a 30 day free trial of our service now by calling 877-87-PLUTO or visit www.plutocommodities.com.

Citation:Cook, Jack (2009). An Introduction to Hog Feeding Spreads [White Paper]. Retrieved Aug. 28, 2024 from CME Group.

This material should be considered as the solicitation of trading strategies and/or services provided by the Andrew McCarty Inc. DBA Pluto Commodities noted in this presentation. These materials have been created for a select group of individuals and are intended to be presented with the proper context and guidance. Information contained herein was obtained from sources believed to be reliable but is not guaranteed its accuracy. These materials represent the opinions and viewpoints of the author and do not necessarily reflect the viewpoints and trading strategies employed by Andrew McCarty Inc. DBA Pluto Commodities. Commodity trading involves risks and past financial results are not necessarily indicative of future performance. Any hypothetical examples given are exactly that and no representation is being made that any person will or is likely to achieve profits or losses based on those examples. Andrew McCarty Inc. DBA Pluto Commodities is not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. This material does not constitute an individualized recommendation, or take into account the particular trading objectives, financial situations, or needs of individual customers. Contact designated personnel from Andrew McCarty Inc. DBA Pluto Commodities for specific trading advice to meet your trading preferences or goals. Reproduction without authorization is forbidden. All rights reserved.

Varricchio is an economist and co-founder of Pluto Commodities.