NHF Snapshot

Packer Capacity

Fall supplies could still be troublesomeBy Steve Meyer

Hog harvest capacity could be tight again this fall. That is news that really shouldn’t be news since one would expect the hog processing sector, through the individual decisions of its participants, to maintain just enough capacity to handle peak fourth quarter needs while minimizing the cost of idle hours in summer months.

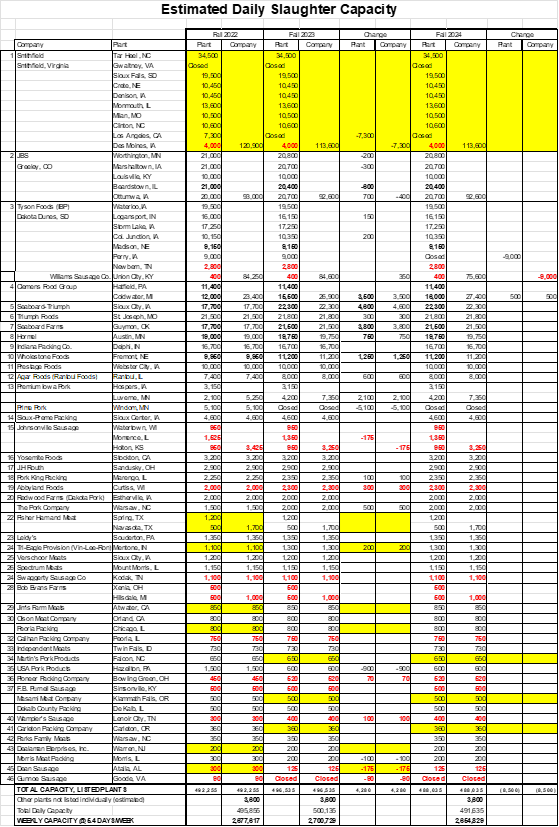

The changes in maximum throughput rates in 2023 were numerous but added up to a net gain versus the fall of 2022. See Table 1.

Some highlights of 2023 are:

The closure of Smithfield’s Los Angeles, California plant in February. Originally owned by Clougherty Packing and then by Hormel Foods, this plant was old and poorly located relative to hog supplies. The latter factor became even more problematic when Smithfield decided to cease live hog production at most of its Utah farms in 2022.

The May 2023 closure of the Prime Pork plant in Windom, Minnesota. Canadian owner Hy-Life had purchased the plant as an expansion and diversification move to complement and support its successful operation in Neepawa, Manitoba. The plant’s financial performance was never as good as hoped.

Capacity gains at a number of plants that were allowed to move to higher chain speeds by USDA after portions of the New Swine Inspection System were thrown out by a Minnesota judge in 2021. The plants authorized to operate at higher line speeds are bolded in Table 1.

A significant expansion at Premium Iowa Pork’s Luverne, Minnesota plant that doubled its capacity and pushed the company’s total capacity to 7,350 per day.

Small changes at a number of other plants, including a 500 head per day expansion at The Pork Company in Warsaw, North Carolina. The biggest reduction among these other plants occurred at USA Pork Products in Hazelton, Pennsylvania, which reduced capacity from 1,500 to just 600 head per day.

Gunnoe Sausage, a sow harvest plant in Goode, Virginia also closed in 2023.

For the third straight year Smithfield Foods declined to respond to our survey. The company had cited antitrust and environmental litigation as the reason for their non-responses in the past. I used other industry sources to estimate the capacities of Smithfield’s plants. No significant changes were noted other than the previously mentioned closure of the Los Angeles facility. Beyond Smithfield and the other three companies shaded yellow, the response rate to this year’s survey was the best ever. Many thanks are due the companies that participated.

I have included an estimate of Fall 2024 capacity in this year’s table to highlight the impact of the announced June closure of Tyson’s Perry, Iowa facility. That plant has long been rated at 9,000 head per day with joint ventures with Nippon Meats and other strong export relationships over the years.

The sum of the 2023 changes resulted in a gain in normal weekday capacity of 4,380 head per day to 496,535 head per day in the listed plants. Adding an allowance of 3,600 per day for state-inspected and non-listed federally-inspected plants would put total daily capacity at 500,135 head.

When I first started doing this survey back in the 1990s I discovered that there were minimal to no hog price impacts when weekly slaughter totals ran roughly 5.4 workdays or less. I have always estimated “normal” capacity to include enough Saturday shifts to reach this 5.4 days of throughput. That practice put weekly capacity last fall at 2.701 million head. The largest weekly total last fall was 2.689 million.

The closure of the Perry plant and a small announced increase in throughput at Clemens Food Group’s Coldwater, Michigan plant will put capacity at 491,635 per day and 2.655 million head per week this fall. The calendar provides a bit of help this year, however, with an extra slaughter day in both the third and fourth quarter adding about 1.5 percent to the potential quarterly throughput. Allowing for that in the weekly figure puts capacity at 2.694 million head. Fall supplies could still be troublesome as I currently expect four weeks of over 2.7 million head with a peak of 2.768 million in early December.

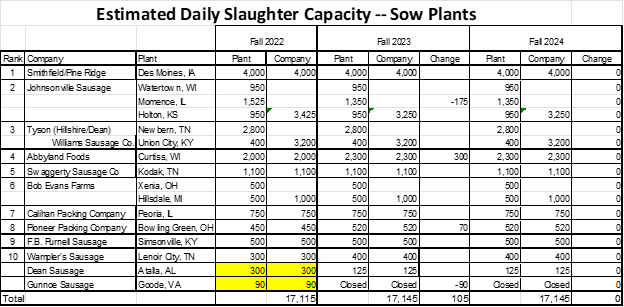

It is important to note also that capacity for a pig isn’t necessarily capacity for any pig. Market hog and sow/boar plants operate in generally exclusive spaces with few animals from either group moving through plants for the other. Sow/boar plants and their capacities are shown in Table 2. 2023 saw very little change in sow/boar plant capacity with a reduction at Johnsonville’s Momence, Illinois plant and the closure of the Gunnoe plant and increases at Abbyland’s Curtiss, Wisconsin plant and Pioneer Packing in Bowling Green, Ohio. No changes have been announced thus far for 2024.

I do not include a weekly slaughter capacity estimate for sow plants simply because the operating rates of these plants are quite variable. Some work four days per week. Others work five. Few work Saturdays. Plants change from four to five depending on market conditions. Should the entire sector work five days, it could handle upward of 85,000 head. U.S. sow/boar packers have slaughtered over 70,000 head in one week on only two occasions since January 2020. The most recent previous occurrence of over 70,000 head in one week was January 2009. Suffice it to say that sow/boar capacity is not a limitation for the U.S. industry.

Slack in the sow/boar space, however, implies that barrow/gilt capacity must be very tight. I estimate barrow/gilt capacity at 2.605 million last fall and 2.596 million for fall 2024 even allowing for the extra slaughter days.

My current forecasts would put barrow/gilt slaughter above this capacity level in 11 weeks in the fourth quarter. The sector can handle some over-run versus capacity by adding Saturday shifts and working more hours on weekdays but several weeks will exceed 5.4 day capacity by roughly 100,000 head. High capacity utilization rates will likely put serious pressure on negotiated hog prices this fall.

Meyer is a lead economist with Ever.Ag.