Market Outlook

Producers face Prop 12 enforcement, sliding domestic demand and possibly cheaper feed

By Joseph Kerns

This changes everything. How often have you heard that referenced to an abrupt change in directive – normally triggered by a catalyst. There are, of course, some events that really do change everything. September 11th, Pearl Harbor, JFK in Dallas – all of these are moments of inflection that are easily identifiable.

Does the recent ruling by the Supreme Court regarding Proposition 12 fall into this category? In the immediate wake of the declaration, it is tough to distance ourselves from the most recent pronouncement that will impact our future. I suspect in a few years we will look back and recognize it as an event that bent the curve, but it will not rise to the threshold of significance that we feel in the present.

The bottom line of Prop 12 is the creation of two curves – one for California and one for the other 48 states if you throw in the verbiage of Massachusetts Question 3 – for both supply and demand. I suspect the California directive (and those of the same ilk) will result in higher prices for pork. The burden is likely to fall predominantly on working-class families and the contrast result is more product availability for the rest of us.

A little math would indicate that pork per capita consumption in California is over 60 pounds while the U.S. average is closer to 50 pounds. Pork is a popular cultural item with the Hispanic community which explains this situation. This will result in higher prices for those in California and more product for the rest of us that will have to clear the market.

This event is a mere week old as of this writing, here is what we think we know so far:

After communication (Tuesday, May 16) with Dr. Elizabeth Cox, animal care program manager for California Department of Food and Agriculture, we learned the following:

The date at which the definition of "housed in a cruel manner" changed was Jan. 1, 2022. That is in the statute.

The court's stay was on enforcement of Prop 12, not the effective date of Prop 12. By that court order, enforcement was initially delayed to "180 days after the publication of final rules." Final rules were published Sept. 1, 2022 so enforcement could have commenced on March 1, 2023. The parties to that lawsuit and the court agreed to delay that date to July 1, 2023 given the pending SCOTUS case.

Enforcement will begin on July 2, 2023 according to Dr. Cox. Since the definition of sow housing changed 18 months ago, no product or pigs will be "grandfathered in." All product sold in California beginning July 2, 2023 must be from sows housed in a manner compliant with Prop 12.

Dr. Cox did say that CDFA's focus over the next seven months will be on getting sellers and suppliers certified per the requirements of the Prop 12 rules. As an industry, we have one of two paths — Accept the ruling, discern its impact and move on — or take an inventory of resources, evaluate the potential opportunity for success and decide whether or not to fight the ruling.

There is a third option with legislation recently introduced by Chuck Grassley of Iowa that would usurp the ruling. I have no way of handicapping the potential success of such an effort.

This is a storyline that will continue to evolve and is well in the psyche of pork producers. More than a little conversation fodder for the upcoming World Pork Expo.

Outside of the hand-wringing over Prop 12, pork producers have another issue at hand. Demand. Specifically, domestic demand. After riding a favorable wave in the post-COVID environment, we have are now experiencing sliding demand coming off the high water mark of 2022 which was an all-time record for meat expenditures.

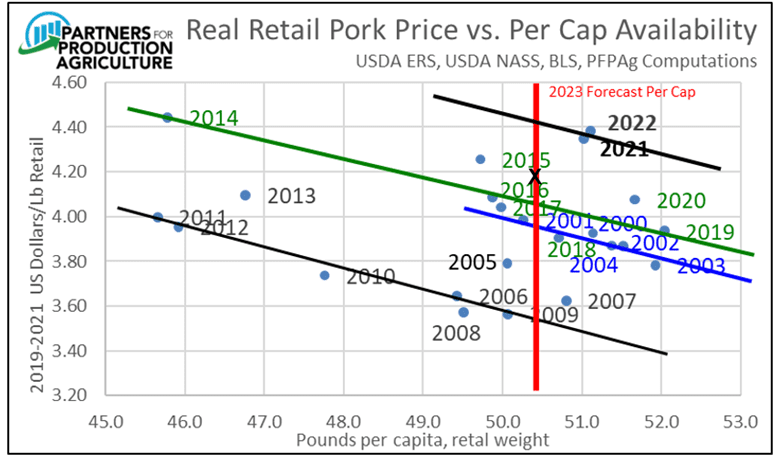

Note the work from Dr. Steve Meyer indicating the favorable experience of the past two years (black demand line) has given way to the previous pre-COVID demand curve (green line) with an X placed where we currently stand. We may not like it, but it does fall reasonably well into the oft trodden history of previous years.

If there is “good news” in this, it is that we are not alone in the shift. Pork, beef and chicken are all experiencing the same phenomenon to some degree or another.

You may read that and note that beef prices are high and not giving much ground. True. If demand for beef would have held at last year’s levels we would be trading that product even higher today given the reduction in supply. The economic reality of our current scenario is supported by the data and, unfortunately, does not appear to be an aberration.

I would like to tell you we see this one changing, but I can’t do that and remain intellectually honest. Product is having a difficult time staging anything that resembles support. Cold storage stocks and bids have us on the blunt end of negotiating power. Pigs currently crossing the border from Canada are anticipated to pick up in volume in response to their economic woes and plant closures.

In short, we need to remain in a defensive posture as long as pig supplies are ample relative to North American shackle space and domestic demand adjustments are not working in our favor.

That comment about shackle space and pig supplies has been off the table for the past couple of years as a static herd and good pork demand played nicely together – we have not held our breath too much coming into the fall.

2023 looks to be a bit tighter. The likely loss of capacity at Windom and a general trend toward better productivity on the farm are shrinking our margin of error into the category of “aware”. We are not in a crisis mode or anything remotely close to the debacle of 2016, we are just not as carefree as we have been in the past couple of years.

Finally, the best news for the pork producer may be in the form of cheaper feed costs. I put that qualifier in italics on purpose as we are in the early stages of the growing season with an atmosphere that is quickly transitioning from the last three years of La Nina into what appears to be a run the other direction to a strong El Nino.

El Nino years are characterized by cool and wet conditions across much of the grain producing areas and are associated with good yields. The timing of this one is important (we are currently in a neutral state as the transition occurs) as rains in August would prove beneficial to both corn and soy whereas dryness through the tail end of the growing season coupled with wet conditions at harvest would be much tougher.

The USDA released their first glimpse of the 2023/24 balance sheet and indicated an average corn price of $4.80/bu – roughly $1.50 per bushel less than what we have experienced the past couple of years. This would be a bit of welcome relief to the pork production sector, but it is probably not enough salve to heal the wounds of the lower price for our products.

Fat prices have softened, soybean meal is well off its highs, DDGS are begging for a bid. Animal ag is probably not going to see record high feed prices in the 2023/24 marketing year, I believe the USDA values – if realized – likely represent good ownership values.

Kerns is the CEO and founder of Partners for Production Agriculture.