NHF Snapshot

Market Outlook

Feed costs down, demand improves, yet expansion remains limited By Brian Earnest

What a difference a year makes. It seems like just yesterday the U.S. pork sector was suffering from pains of weak demand and elevated operational costs. Falling feed costs have now played a significant role in improving producer profitability. But value at the meat case also appears to be benefitting pork and poultry disappearance. COVID-pandemic related savings has now been completely depleted, and consumers are more heavily relying on credit. We expect this to be a long-term opportunity for value-type animal protein offerings.

With feed costs down more than 25% in the second quarter, Iowa State estimates wean-to-finish operations averaged profits of more than $20/head for the period, a huge swing from losses of $40/head a year earlier.

Additionally, cutout strength witnessed during the first six months of 2024 and improved processor demand has brought with it a prolonged stretch of elevated hog prices. And exports are in outstanding shape, despite deglobalization in other industries. At the end of the day people gotta eat!

It has become quite a bit easier to be optimistic about the outlook for both producers and processors. Yet, cumulative sow slaughter was up 8.5% through the end of May. The pace is leading USDA sow slaughter forecast to reach 3.355 million in total during 2024, an increase of 5% YoY, besting every year since 2008.

So why are expansion expectations limited throughout the industry? Admittedly, some rebuilding, or cycling of the breeding herd is under way. But forefront limitation is that most of these variables are out of the control of producers, and uncertainty combined with higher operational costs and higher borrowing costs limit expansion. More importantly, the difficult past is tough to forget.

Following several years of disruptions from COVID-19 impact to consumer behavior, transformation to “normalcy” remains a work in progress. Purchasing behavior remains unstable. In 2020, domestic consumption shifted heavily to favor food at home, then came “revenge spending” when travel, leisure and all out food away-from home spending surged. Now as inflation has eaten away at consumer budgets from many angles, and consumers push back on a $15-$20 burger, the addition of bacon might become a luxury we can no longer afford.

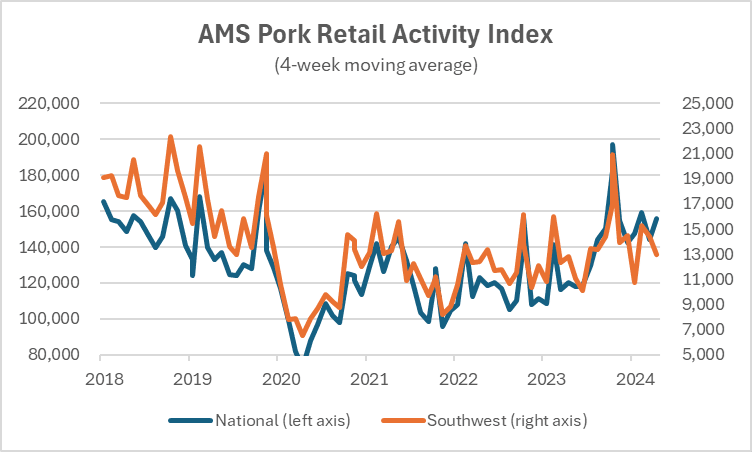

So too, the implementation of California’s Prop 12 has been a burden worth considering. From a competing meat standpoint, while retail prices remain firm, feature activity is worth considering. Data collected from AMS suggested a big up-swing in pork features towards the end of 2023 but has since subsided. Pork feature activity in California is now trending below the pace of the national average, whereas promotional activity within the state has historically almost always been higher (see Fig. 1).

From USMEF, we learned in May that marketing of pork loins is prevalent overseas. In doing so, U.S. exporters have added record value to hogs. From January – April 2024, exports added $66.28 to the value of every hog produced in the U.S. That amount is up 7% YoY and is up roughly $12/head from pre-COVID levels. Export markets absorbed 30.7% of all pork and pork variety meats during the first four months of 2024, which was record high.

Not too long ago, China was a top destination for U.S. pork exports, but the opportunity into China’s markets has declined in recent years as their efforts to rebuild domestic supplies exceeded expectations. For U.S. producers this has meant a 15% YoY January-April decline in pork exports to what was once the top destination. But even with U.S. pork exports to China in decline, U.S. pork and pork variety meat exports were valued at a record $8.16 billion during 2023, up 6% YoY and had reached nearly $2.9 billion, up 10% YoY during January-April 2024.

Mexico remains a top destination. Exports to the destination have been energized by reshoring of manufacturing and an expanding middle class that has bolstered the Mexican peso vs. the US. dollar. With U.S. holding an 85% share of Mexico’s pork imports, the market in general and any potential threats remain important. But while the share of U.S. pork exported deserves attention, marketing of pork items outside of bacon still has room to grow.

I recently heard that for the first time ever, Americans are now more likely to have an air fryer than a coffee maker in their kitchen. Chicken has latched on to this opportunity, offering wings, tenders, bites, etc. as an easy take-air-fry-serve option for consumers seeking access to the intersection of convenience and nutrition. This seems an obvious opportunity, with a not-so-obvious solution from pork. While bacon is the top consumed pork item in the U.S., I cannot help but to think there can be another pork item to utilize all these air fryers to satiate the U.S. consumer desire for variety. I am excited to see what comes next.

Earnest is a lead animal protein economist for CoBank.