Market Outlook

Expansion unlikely as pork encounters new headwinds

By Brian Earnest

As 2023 began, animal protein producers had two concerns at top of mind: Not only the impact that a shrinking beef cow herd would have on overall availability of meat and poultry, but also the degree to which softening real incomes in the face of rampant inflation would have on consumption. Through the first half of 2023, most accounts suggest that supplies of animal protein remained ample and that retail demand remains good but is softening.

While domestic market conditions during the first half of 2023 have largely dispelled any talk of extreme pessimism for animal protein producers, pork has seen no shortage of challenges. Harvest rates exceeded expectations, but retail prices remained stubbornly high, and domestic pork consumption trailed expectations.

On the export front, China’s hog herd rebounded, resulting in dampened global market opportunity. Fortunately, U.S. pork has found growing market opportunity in Mexico this year.

To top it all off, SCOTUS upheld California’s Prop 12, which will likely put dent in domestic offtake, the size of which is still unclear. Add in high feed costs, and the result for producers was extremely poor margins.

As is usually the case, the path forward is not entirely clear. Historical trends suggest that the opportunity for any significant uptick in domestic pork consumption looks rather modest. Over the last 10 years, U.S. consumers have managed to add only about 4 pounds of pork to their diet annually, but current consumption levels are the same as they were 20 years ago.

The best argument for a bullish price move is to point to the beef market: Cattle supplies are likely to continue to fall through 2025 or 2026, suggesting (all else equal) a widening gap in U.S. red meat production vs. consumption trends.

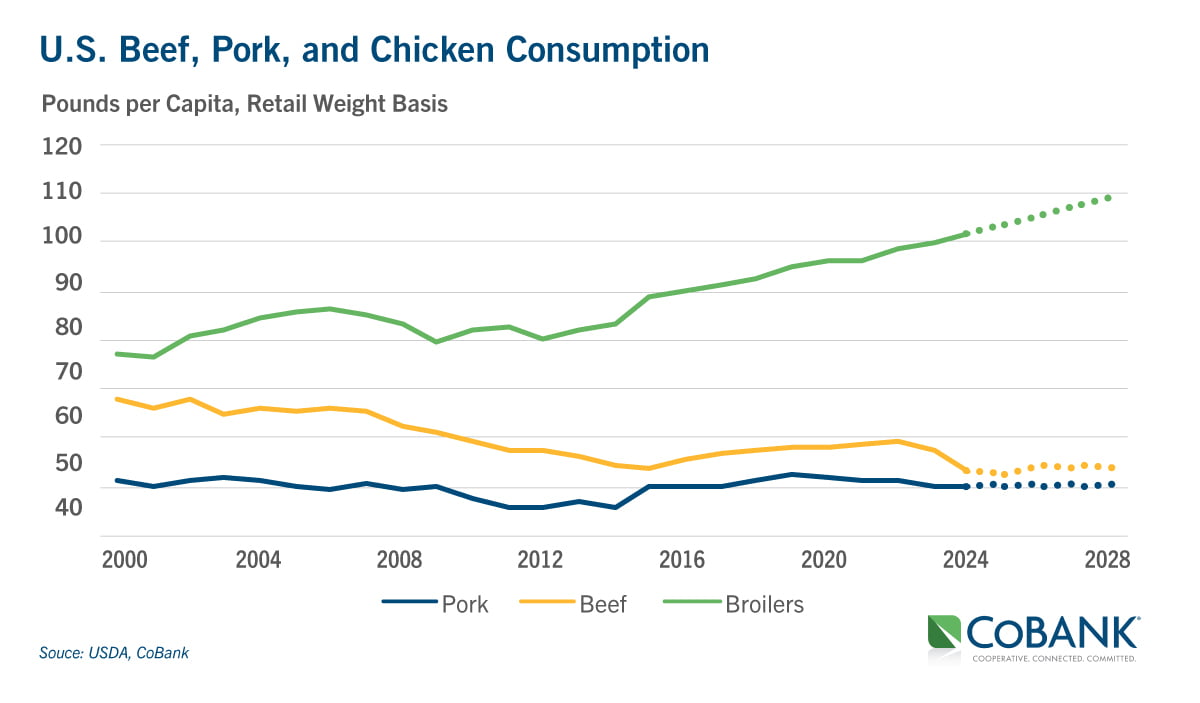

From 2016 to 2022, U.S. animal protein consumption rose an average of 1% annually. Pork made strong gains in market share early on, but chicken consumption has grown by nearly nine pounds (10%) per capita in that period. Due to the supply shortage, beef consumption is forecast (by USDA) for a major contraction next year, a trend that will develop more fully later this year.

Depending on how retail pork prices move (particularly on branded processed products) and how incomes fare, it seems chicken may again be well positioned for growth out front. However, broiler-type hatching egg layer productivity has eroded drastically this year, which could hamper U.S. broiler integrators’ expansion ability nearby.

In the latest quarterly USDA Hogs and Pigs report, most metrics are indicative of moderating hog supplies nearby, and contraction likely in the longer run. Farrowing intentions were down 4% for June-August, so it is unlikely to see growth. The is despite pigs saved per litter hit a new record on June 1, up 3.3% YoY, as porcine reproductive and respiratory disease and porcine epidemic diarrhea have been less prevalent this year. That being said, there was little evidence that a major contraction was afoot throughout the industry either.

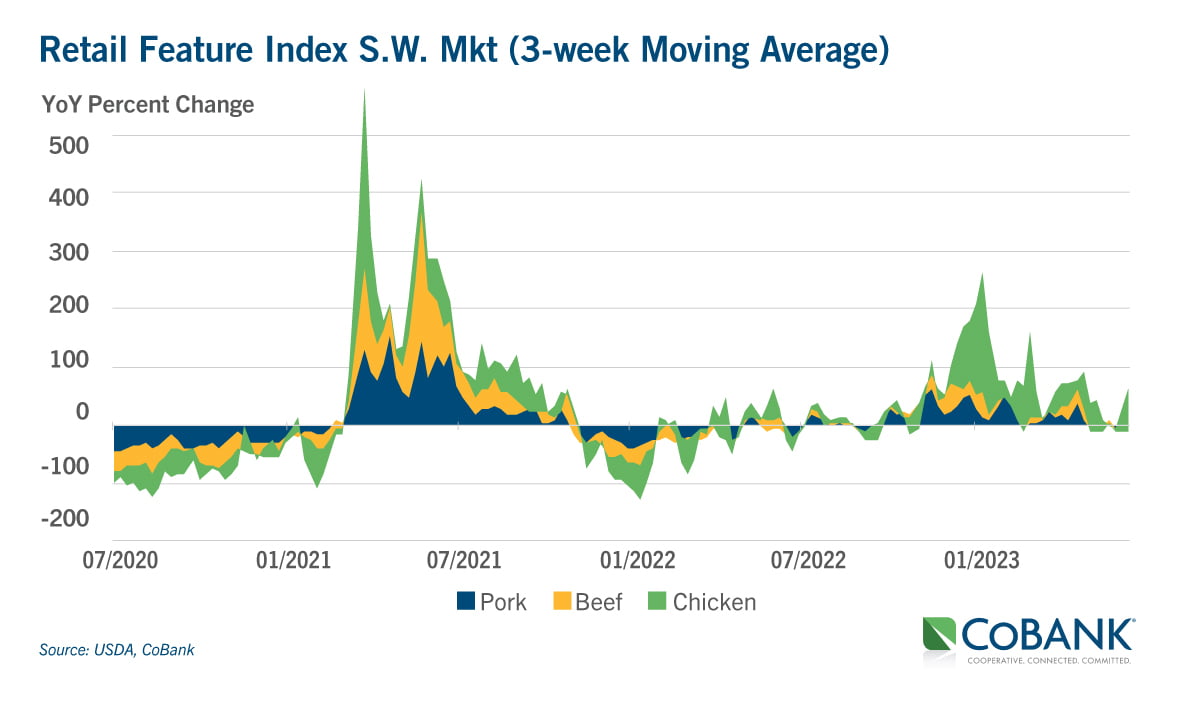

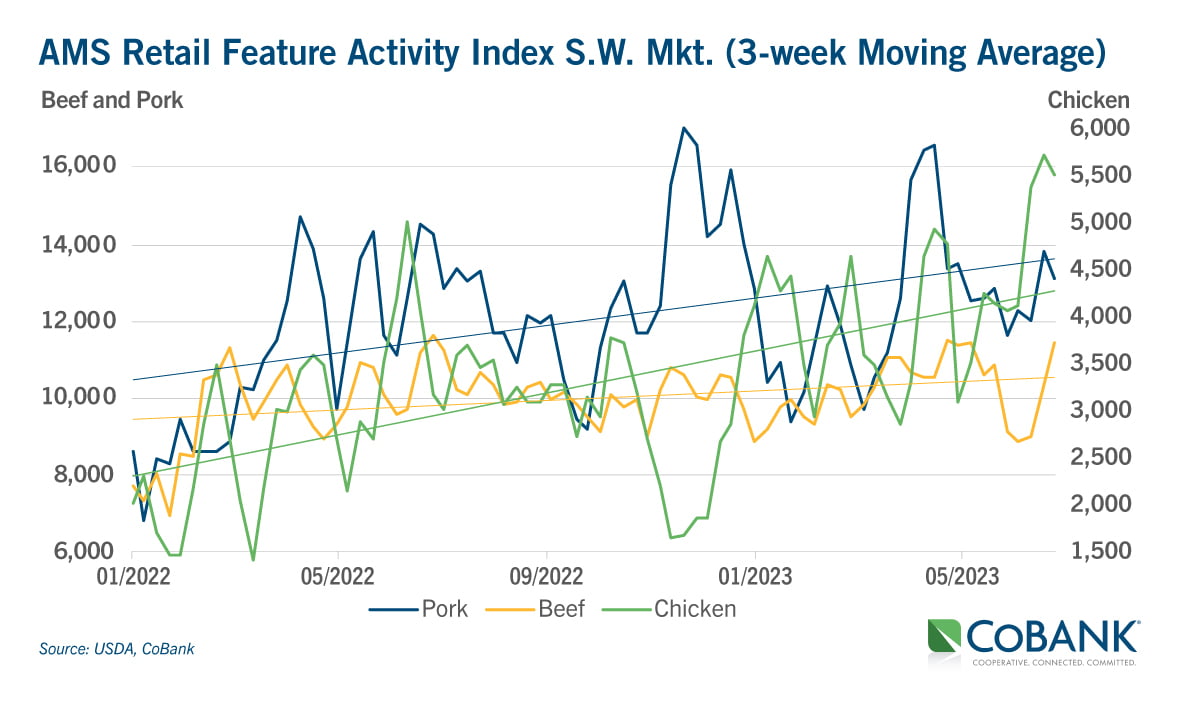

Meanwhile, recently upheld legislation in California suggests that residents there should soon be expecting dwindling pork offerings at grocery stores until the industry can ramp up efforts to produce hogs that comply with Prop 12 stipulations. Retail feature activity (reported by USDA-AMS) shows that the Southwest region has been strongly promoting pork products as of late. However, enforcement of Prop 12 will mean restricted whole pork meat flows into California, and pork ad space at grocery within the state will suffer.

Independence Day typically represents the peak of grilling opportunity and feature activity typically follows suit. While the Southwest region market featured plenty of pork, only the chicken index rose to the occasion this year, growing 74% YoY.

Though it appears pork retail-feature activity has seen some rebounding from 2020 levels overall, there is less optimism that pork will be on ad in California with any sort of significance. Still, this should leave ample opportunity for other regions to feature pork during BLT season.

The bottom line remains that with so many changes and developments in and around the pork industry, the outlook is murkier than ever. As a result of waning confidence in the market for hogs, and rising capital costs and interest rates, bankers are hearing very little interest from existing borrowers in adding new barns to the system. This suggests a prolonged deficit in pork compliant with Prop 12, and a market that will remain out of balance for the foreseeable future.

Earnest is lead economist for animal protein in CoBank's Knowledge Exchange research division.