Latest from Farm to Fork

By Steve Meyer

My outlook for pork and hog markets remains guardedly optimistic for the foreseeable future given a number of recent developments. Continued strong pork and hog prices, however, will not likely translate to strong profits given high costs of feed and other inputs. A number of factors are preventing output expansion, a fact that may keep hog and pork values higher than would normally be expected following a period of strong profits. There are a number of issues that could derail any of those statements.

Such is my frame of mind as of early July 2022. Let’s explore the issues in some detail.

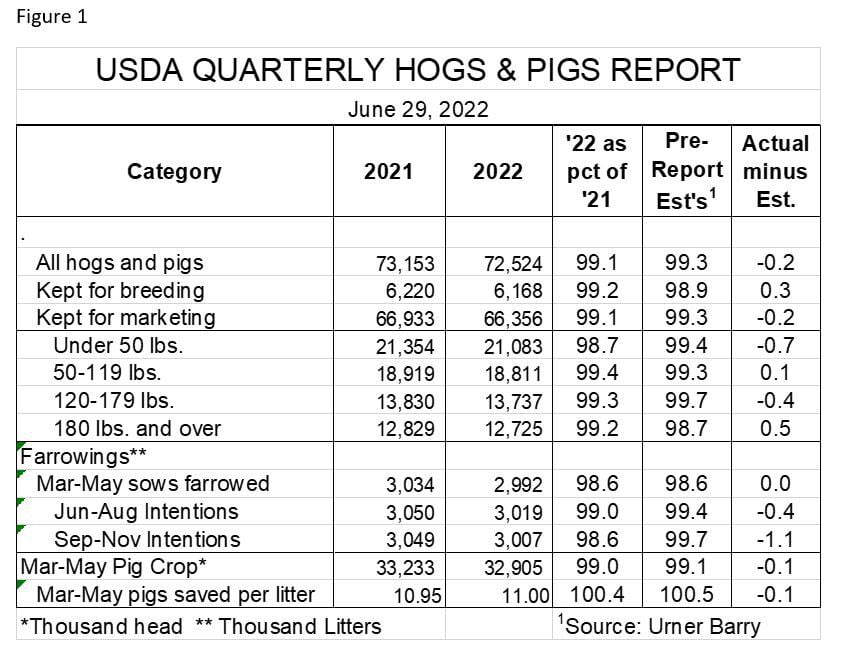

My main takeaway from USDA’s June Hogs and Pigs report is that U.S. hog supplies are not expected to grow for the foreseeable future. Key data appear in Figure 1. USDA’s estimates were very close to the average responses of analysts surveyed by Urner Barry prior to the report. In fact, the two sets of numbers agreed more in this report than for any in recent memory, leading me to conclude that the report was neutral, a conclusion borne out by Lean Hogs futures prices in the days following the report’s release.

The most important takeaway from this report is that the industry has not moved into expansion mode in spite of very good profits in 2021. A continuation of no year-on-year growth of the breeding herd and productivity challenges imply that U.S. market hog numbers will be lower than one year earlier through the first half of 2023.

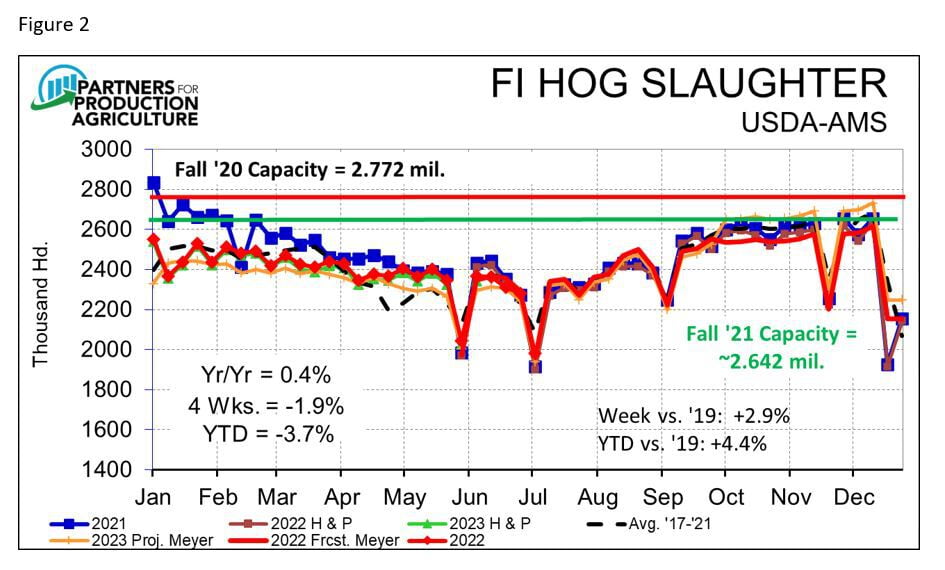

The reductions may be small enough that more imported Canadian pigs (especially market hogs) could push slaughter slightly higher in some weeks and months but the increases will be small if they happen. My weekly slaughter forecasts as well as that implied by the USDA report appear in Figure 2.

One important feature of Figure 2 is that packing capacity should not be a significant challenge this fall. U.S. plants can handle about 25,000 head more hogs per week than the Fall 2021 capacity shown on the chart due to line speed waivers that have been granted to five plants so far. More waivers may be coming that would provide yet more capacity. Labor challenges have diminished significantly as 2022 has progressed allowing virtually full utilization of capacity and much fuller value capture from processing operations.

Production cost are high and will remain so for the foreseeable future. Costs are a key determinant of supply but that influence is long term in nature. Short run costs changes do not shift the supply of hogs because decisions regarding today’s hog supply were made months ago. In the short run, today’s higher costs of feed impact only profits.

Expectations for production costs and the costs of building materials, labor, etc. are all limiting producers’ response to today’s higher prices. I do not expect any appreciable growth in output through 2023 unless productivity challenges (primarily the number of pigs saved per litter) are solved.

World pork supplies are lower and hold the promise of tightening further. Germany’s output is significantly lower in the wake of its African swine fever challenges. Dutch farmers are under intense government pressure to reduce output of a number of commodities, including pork. China’s pork supplies are, according to government report and supported by recent price increases, tightening.

U.S. and Canadian pork sellers should see growing opportunities into 2023. The primary hurdle to growing exports is the value of the U.S. dollar which has increased sharply as world tensions have risen on many fronts. Any easing of those tensions should allow the dollar to fall making U.S. product a better value for export customers.

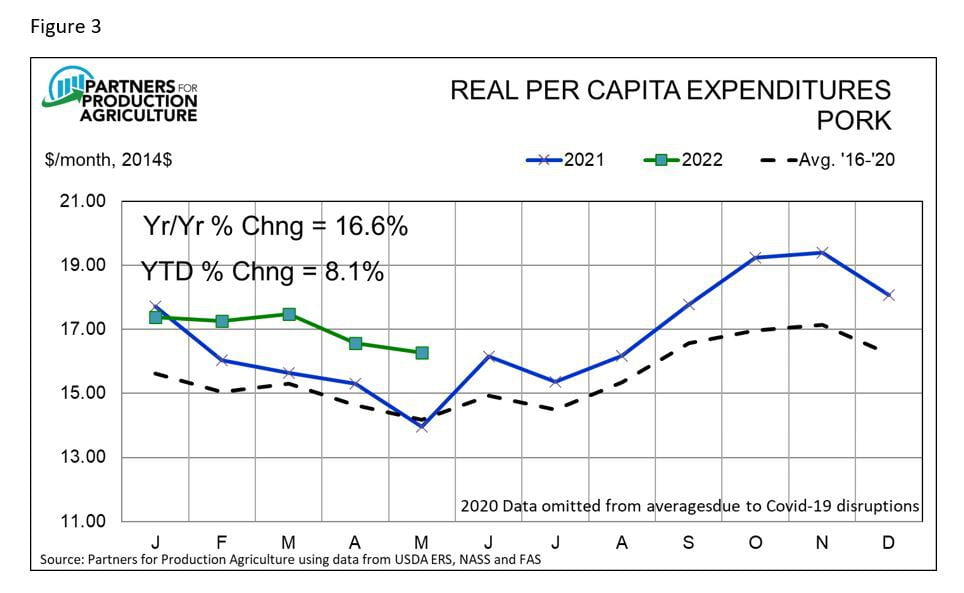

Amidst all the supply issues, though, is the bright, bright beacon of U.S. meat and pork demand. Real per capita expenditures for pork (a measure of the status of pork demand) has grown steadily since 2018. It gained 5.4% in 2021 and is up 8.1% year-to-date through May. See Figure 3.

Note that this does not mean that Americans are eating more pork. Per capita pork availability/consumption has been between 51 and 52 retail pounds per person from 2018 through 2021 and is expected to remain in that range this year.

But Americans have demonstrated a willingness to pay higher and higher prices – even adjusted for inflation. Selling the same quantity at higher prices means demand is strong.

Why has this happened? Economic theory tells us that the demand for a product is determined by consumer income levels, the prices of competitor and complement goods and consumer tastes and preferences. In practice, complement goods have insignificant impacts on pork demand and income levels are very marginal contributors. Prices of beef and chicken have been strong, contributing to strong pork demand.

There is no way to directly measure of tastes and preferences so any demand changes not explained by other factors are attributed to this very important driver of consumer behavior. Using that default approach, it is safe to say that tastes and preferences have improved for all meats in recent years, especially since the pandemic when it appears that U.S. consumers began consuming more meat at home.

So what do I expect for pork and hog markets? A lot more of what we have seen since May. And that says a lot since we would normally expect significant price declines in Q4. I won’t say prices will remain where they are but if demand holds its recent strength and pig supplies fit the June Hogs and Pigs report, it appears this year’s seasonal downturn may be smaller than usual. The return of China as a buyer of U.S. pork would add to that strength.

What are the risks? First and foremost would be a trade-impacting foreign animal disease such as ASF, FMD or classical swine fever. Those are always the biggest risks facing a country that exports a sizable portion (in our case 25% of carcass weight output) of production.

Second on the list would be an issue that hurts demand. An example would be the “swine flu” scare of 2009 that scared consumers, hurt demand and robbed producers of their normal summer price rally.

Third on my list would be the loss of a packing plant for any appreciable period of time. The capacity situation is not tight this fall but neither is there much slack. Smithfield’s closure of its Los Angeles, CA plant should not impact this fall as it is slated to cease operations in early 2023. The loss of this plant may have consequences for 2023 if other plants cannot add throughput ability.

Meyer is a lead economist with Partners for Production Agriculture.