Market Outlook

By Steve Meyer

I wish I had something new and exciting to offer about the U.S. hog and pork outlook for 2023. I feel like I have written and said the same thing about our business for the last two years. It would be nice to write about something different and I’m sure it would be nice for you to read about something different. But the past two years have been pretty good so I have to remind myself that this repetitive discussion could be worse: The industry could have found itself in a train wreck.

So I will quit complaining and try to update you on the conditions that are getting a bit old but still provide room for optimism.

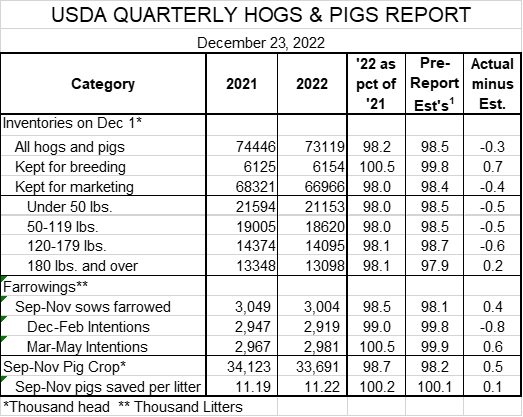

USDA’s December Hogs and Pigs report indicates that hog numbers have not increased. See Figure 1. In fact, most numbers in the report were smaller than one year ago and every number was reasonably close to analysts’ pre-report estimates.

The latter implies that the USDA inventories and expectations were “in the market” at the time of the report. Cash hog markets have been generally sideways since the report’s release while futures have fallen sharply as the February contract has reconciled the huge premium it held to get more in line with spot prices.

One number in the report deserves a bit of attention: The Dec 1 breeding herd of 6.154 million, 0.5 larger than one year ago. This is the first quarter in which the breeding herd has grown, year/year since 2020.

Furthermore, average litter sizes remain flat while we know that the herd’s genetic potential for larger litter sizes continues to grow. March-May farrowing intentions match the larger breeding herd suggesting that supplies from September forward could increase versus one year earlier. This is especially true if producers are finally able to raise all of the pigs these sows are capable of producing. Disease and labor challenges have, we believe, been the reason for the difficulties and both of those appear to be lessening to some extent.

For the year, I expect 2023 slaughter will be very close to the level of 2022 with quarters 1 through 3 seeing lower numbers and Q4 seeing growth of, perhaps, a bit more than 2%.

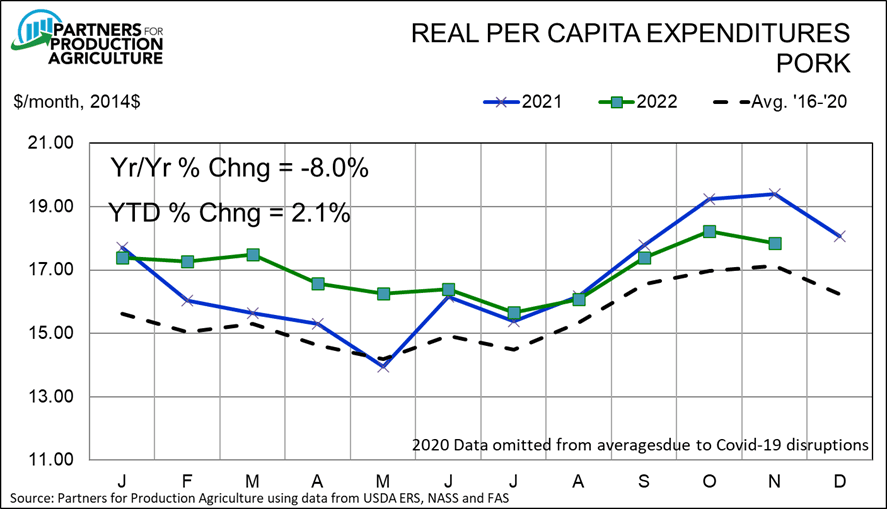

The industry’s saving grace over the past two years has been robust domestic consumer-level demand and the good news is that, though down slightly in Q4 2022, it still appears strong. Figure 2 shows our monthly calculations of real per capita expenditures (RPCE) for pork, a measure of the status of consumer-level pork demand.

Through November, total pork RPCE is up 2.1% for the year. The past three months have been progressively lower relative to last year but remember that October, November and December 2022 were the highest months on record for pork RPCE. Falling short of those lofty levels should be no shock and, I think, little cause for worry.

The questions is what might consumer-level meat and pork demand do from here. I have two major concerns. First, pork and meat demand could fall due to inflation-impacted real income levels. Second, the apparent positive shift in pork and meat tastes and preferences could wane.

But there are potential positives, too. Beef prices have risen and could become explosive if rains come for the Texas-to-Montana beef cow belt and drive heifer retention this spring. More heifers for the cow herds mean fewer heifers in feedlots and an already tight beef supply could get much tighter.

Chicken companies have already shown signs of reining in their production increases of last summer suggesting that prices will rebound from their recent low levels. And it is very possible that those tastes and preferences remain strong and the economy overcomes all of the storm clouds.

Where domestic demand has been a positive force, exports have been a drag on the wholesale demand for U.S. pork since mid-2021 and will finish 2022 nearly 10% lower, year/year. Virtually all of that decline is due to lower shipments to China and prospects of those returning to African swine fever-driven levels are, in my opinion, practically nil.

Shipments to Mexico remain strong and U.S. product should enjoy some price advantages to EU product in other markets such as Japan and Korea given output reductions on the continent and the recent fall in the value of the U.S. dollar.

U.S. Dollar Index futures are down nearly 9% since reaching 20-year highs in September. Barring any significant trade interruptions, our colleague Brett Stuart of Global Agritrends expects exports to increase 2.8% this year. He also expects surging imports (up more than 50% since 2020) to fall by about 15% this year.

Finally, costs of production were record high in 2022 and show little sign of abating in 2023. Iowa State University’s estimated costs for Iowa farrow-to-finish operations averaged $95.12/cwt carcass in 2022.

Our experience is that ISU’s estimates are about 5-8% lower than costs at the average farrow-to-finish operation so I would peg that figure at $100-$103. Adjusting current futures prices for current large positive basis levels for corn and soybean meal, my expectation for 2023 average cost is very much the same.

Biofuels policies at the federal and state levels are a primary driver of these higher grain prices and they are not going away. Demand for renewable fuels has increased the value of all vegetable oils, pulling soybean prices and, in turn, corn prices higher. Future increases in the output of sustainable aviation fuel will add fuel to that fire (no pun intended) and support ethanol values as well.

There simply aren’t enough acres to grow enough crops worldwide to meet this higher demand at “old paradigm” grain and oilseed prices.

Will yield gains eventually push prices lower like they did in the 2010’s following the ethanol shock on grain prices? Maybe. But that will take time so livestock and poultry producers must at least change their expectations for the next three to five years and adjust their critical levels for price decisions.

About the only exception is soybean meal. U.S. crushing capacity is on track to increase by about 20% over the next few years in response to higher soybean oil prices. More oil means more meal and we fully expect soybean meal prices to fall sharply in the future. But the plants have to come online to make that happen.

Risks abound. ASF is still rampant on the island of Hispanola, just 100 miles from Puerto Rico. La Nina is changing to El Nino so crop conditions in North and South America will change versus recent years. China has relaxed its draconian COVID policies so its economy may rebound. Or it may not.

Who knows what a split government, and even an apparently split majority in the House, may do or not do. Will the Federal Reserve stick to its guns in stopping inflation? What will the next mutation of porcine reproductive and respiratory syndrome bring and when will it come?

It looks like there are plenty of potentially exciting things after all. Thank goodness they haven’t happened yet and thus allow me to write this boringly similar essay. Happy New Year.

Meyer is a lead economist with Partners for Production Agriculture.