The global fleet of transport helicopters in military service will stand at 14,148 aircraft by the end of 2023 and is projected to grow to 14,950 by the end of 2032 as air forces seek to expand battlefield mobility.

The 2023 in-service fleet will consist of 12% heavy transports (MTOW above 40,000 lb.), 53.8% medium transports (MTOW of 15,500-40,000 lb.), 19.5% intermediate transports (7,000-15,500 lb.) and 14.7% light transports (less than 7,000 lb.).

Despite the inclusion of initial deliveries relating to the Future Long-Range Assault Aircraft (FLRAA) towards the end of the forecast the global fleet of Black Hawk helicopters which the new platform is set to replace is expected to grow. The ubiquitous UH-60 fleet is expected to expand at a CAGR of 0.1%, reaching 3,242 helicopters in 2032 representing 21.7% of the global RW transport fleet by that time.

The AW139/149/169/189 family is one of the fastest growing European RW transport families with a CAGR of 3.03% following recent source selections by Poland, Italy and Austria. Leonardo platforms are expected to generate $12.5 billion in MRO demand over the forecast relative to $10.7 billion for NHIndustries and $17.9 billion for Airbus.

European primes currently lack a heavy lift platform comparable to the Boeing CH-47, Sikorsky CH-53 and Bell-Boeing V-22. These platforms are expected to generate more than 92% of heavy transport MRO demand over the decade.

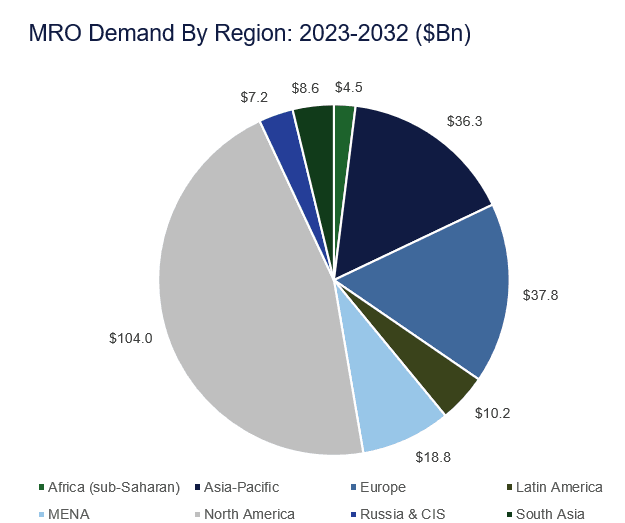

MRO demand generated by military transport helicopters will be $227.4 billion over the 2023-32 period.

Heavy transports will generate 29.8% of that demand, medium transports 50.8%, intermediate transports 14.7% and light transports 4.57%. After North America at 45.7%, Europe and the Asia-Pacific region will generate the most MRO demand, at 16.6% and 16%, respectively.