The military aircraft market is projected to generate $1.34 trillion in demand for maintenance, repair and overhaul (MRO) over the 10-year forecast period. Annual demand is expected to increase at a 1.12% CAGR from $127.7 billion in 2023 to $141.1 billion in 2032, slightly ahead of the wider 0.5% aircraft fleet growth. This trend is being driven primarily by the higher MRO costs associated with the technologically advanced aircraft being delivered over the course of the decade.

The vast majority of the demand will be generated by Western made aircraft types which account for $1,069.8 billion or 79.9% of overall demand.

Driven by the size of its fleet and high readiness requirements the U.S. military alone is expected to spend $550.8 billion on MRO activities over the period accounting for 41.2% of the global total.

The regions with the fastest growing MRO demand are Asia-Pacific at a 1.81%, CAGR and South Asia at 1.33% however many of the individual countries with the fastest growing MRO demand are expected to be in Europe. Poland, Finland and Belgium are among the countries where maintenance spend is expected to expand at a CAGR in excess of 4%, primarily driven by the modernisation of each country’s combat aircraft fleet through the period

With 1,563 deliveries scheduled between 2023 and 2032, Lockheed Martin’s F-35 is the biggest driver of change in MRO demand. Annual MRO demand generated by the F-35 is expected to increase from $7.1 billion in 2023 to $16.3 billion by 2032. As a result, the F-35 family alone is expected to generate 11.6% of all annual MRO spend globally by the end of the forecast.

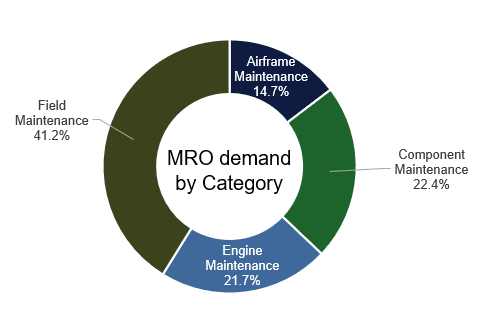

41.2% of all MRO demand is expected to be generated at the unit level as field maintenance, the largest single category worth $551.4 billion. Engine MRO activities are valued at $291.0 billion, components at $300.5 billion and airframe maintenance at $196.3 billion.