Farm incomes stronger than expected

In early September, USDA released an update on farm incomes. Most analysts were expecting some rough numbers but it was not nearly as bad as expected, according to Richard Brock.

By Richard Brock

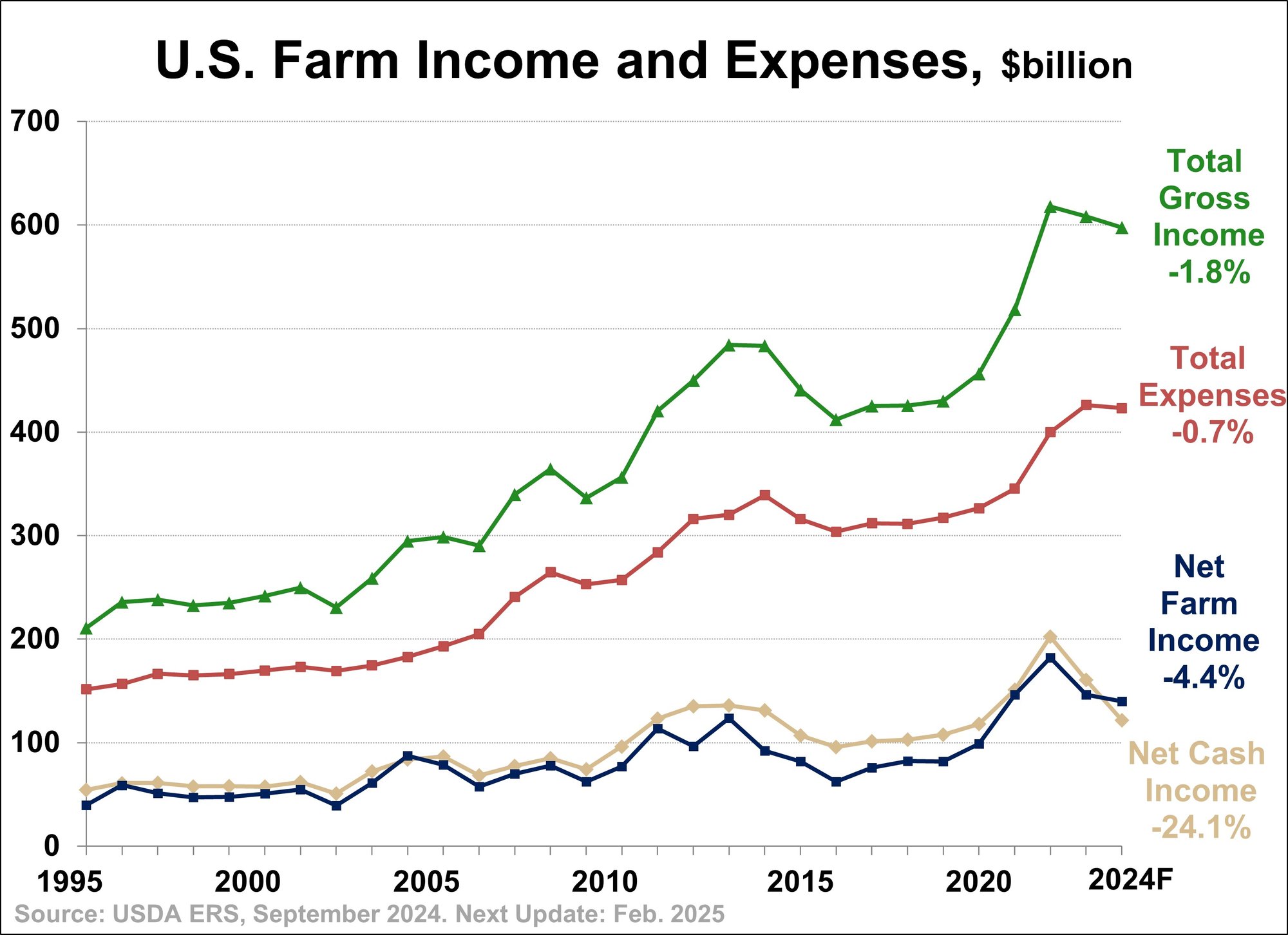

In early September the US Department of Agriculture released an update on farm incomes. With the collapse of the grain markets, most analysts were expecting some rough numbers but it was not nearly as bad as expected. As the graph indicates, net farm income is expected to be down 4.4% this year while net cash income is down 24.1%.

As is almost always the case, there is a huge spread between the top 20% of producers who know how to market and the bottom 20% who have never figured it out.

As everyone in the livestock industry recognizes the past 12 months have been challenging for the pork industry. Those who are vertically integrated are doing fine but for pork producers who are not vertically integrated, the price spreads have been challenging. The dairy industry was challenging in the first half of the year but prices have rebounded very strongly and they are now doing well. The beef industry, with total cattle numbers at the lowest level since 1952, is having its share of ups and downs. The last time that feeder cattle were trading at a $64 premium to fat cattle was in 2015. That resulted in a substantial decline in cattle prices. Many in the industry are making the assumption that it cannot happen with the low number of cattle. It can happen and most likely will. What the market will find out is the world has a shortage of $90 cattle which we had in 2020, but we are not going to have a shortage of the $180 variety.

For grain producers this is a year of opportunity. No one gets ahead on a net basis when corn is at $8.00. Everybody is doing well enough. But when corn goes to $3.60 those who are poor marketers might be fortunate to survive. It results in tremendous opportunities for grain producers who have managed well. Consider the following:

The number of farmland sales is down substantially, approximately 60% from a year ago in the Midwestern states. But prices are holding steady. Approximately 84% of the land owned in the state of Iowa is owned debt free. Forced liquidation sales don’t happen if there is not a significant amount of farmland with high debt.

Cash rents are also holding steady. Most cash rents are negotiated from right now until December 1. Producers are not going to want to run the risk of losing farmland by underbidding the rents. When it is all said and done, only in very few isolated areas will cash rents decline.

Prices of used farm equipment have plummeted. Early auctions that have happened within the last six weeks has seen declines of combines and tractors drop by 60% of what they sold for new a year ago.

New equipment prices are very soft. Dealers do not like paying 9% carrying cost on one million dollar+ combines and large tractors at almost the same price. Deals are being cut everywhere. For the farmer with cash who is not fully equipped, the opportunities are big.

Year-end pre buys of chemicals, farm equipment and in some cases seed, will be down. Early sales of seed, however, are showing no declines in prices and strong demand. Fertilizer prices have bottomed. Thus there will be some prebuys but the reality is not that many farmers are going to need to prebuy in order to save on income taxes. This is a very different year than the previous three years.

Putting It All Together

Grain prices peak on bullish news and bottom on bearish news. A month ago the news was as bearish as it could get. Both corn and soybean prices have made significant bottoms at probably the lowest prices of the year. We certainly hope so. The upside may not be substantial. But the reality is buyers of corn and soybean meal should base their decisions on the fact that the market is done going down and buyers should be aggressive. Don’t ever buy because you think prices are going higher. You make buying decisions because you think prices are done going down. This is a year where buyers of feed should be aggressive early.

Richard Brock is Chairman of Brock Holding Company which is comprised of Brock Associates, an agricultural marketing advisory service and publisher of The Brock Report, established in 1980 and Brock Investor Services (futures and options brokers). The firm, based in Milwaukee, Wis., now has six offices and manages grain sales on approximately 800,000 acres throughout the U.S. and is an advisor on purchasing strategies for many large poultry, pork, dairy and food companies.