Corn and soybean prices - Seasonal price lows are likely established

Economist Richard Brock explains why now is not necessarily the time to get bullish but it is time to quit being bearish

By Richard Brock, Brock Associates

The world is in chaos. Between the war in Ukraine and the horrific situation in Israel, the rest of the world is in intense fear of what else might happen. Whether we like it or not, worldwide chaos creates concern about grain supplies and many companies and countries want to make sure they have adequate inventories in case supply chains break.

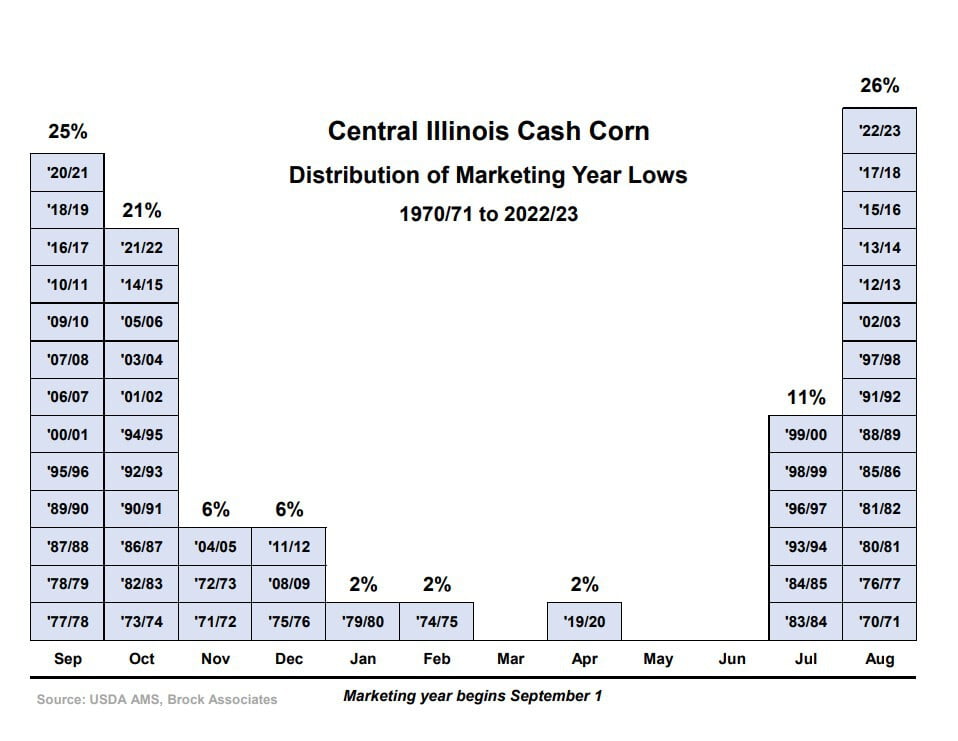

This all plays into the seasonal tendencies of corn and soybeans. As can be seen on the graphics below, since 1970, cash corn prices in central Illinois made their lowest price of the marketing year during the month of September 25% of the time, and during October 21% of the time. In other words, corn prices hit their lowest price of the marketing near before November 1 in almost half of the past 52 years.

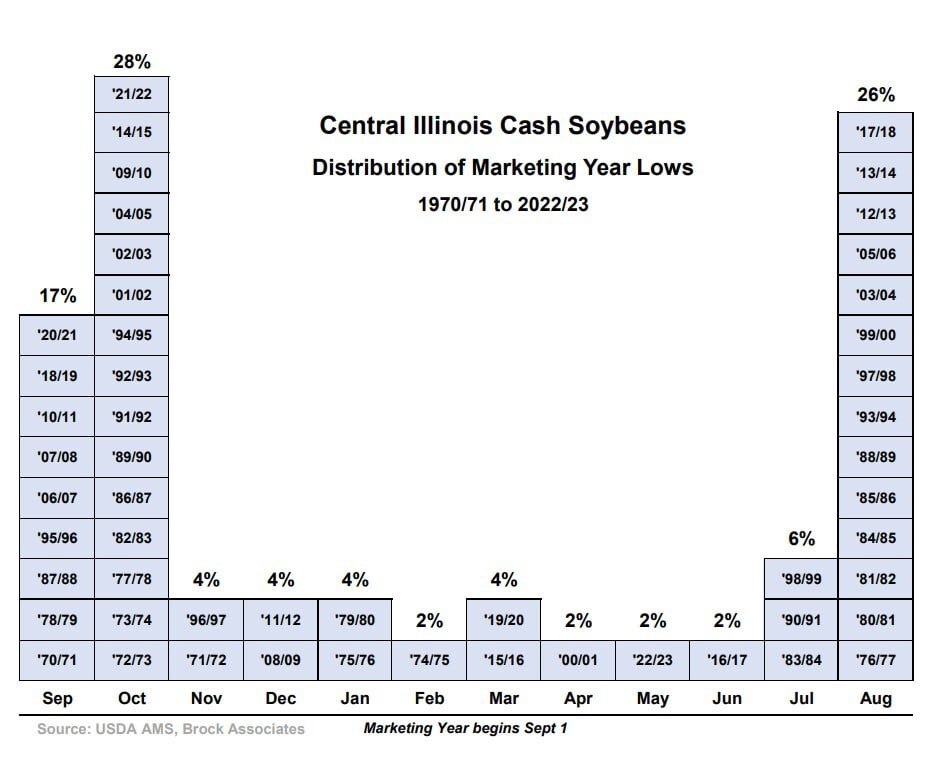

The marketing year lows for soybeans occurred in a similar fashion. The lows for soybeans occurred during the month of September 17% of the time and during October and 28% of the time. 45% of the marketing year lows occurred prior to November 1. I believe that the chances are high that the marketing year lows are already in for both corn and soybeans.

October Crop Report

The October 12 USDA Supply & Demand report sent corn and soybean prices flying. There was really nothing bullish, but the lack of bearish news at very low price levels was enough to spark major buying. With an expected average price of cash corn in central Illinois of $5.00 per bushel for this marketing year and cash corn prices trading in most areas around $4.50, It was only logical that the lack of bearish news was going to send prices higher.

Soybean supplies are tight. Our ending stocks projection for 2023/24 is 237 million bushels compared to the USDA’s projection of 220 million and a 268-million-bushel carryout in 2022/23. Ending stocks of 237 million bushels translates to an ending stocks-to-usage ratio of 5.6%. That’s low. That makes this market vulnerable to upper price moves.

On the bearish side however, price levels above $13.00 have already discounted much of the bullishness from the anticipated demand for renewable diesel. One plant has been built so far and many others are either under construction or on the drawing board. Between plant expansions and new construction, a total of 1.762 billion bushels of additional annual crush capacity has been announced to come online by 2026. But it’s going to take time before that additional demand materializes—if it does at all.

The Bottom Line

It’s not necessarily time to get very bullish corn, soybean, and soybean meal prices, but it is certainly time to quit being bearish. The downside potential from a buyer’s point of view is now outweighed by the upside price risk. A month ago, we didn’t feel this way. But a month ago, the market was a lot higher than it is now. It’s time to shift gears and jump on the friendly side of grain prices. Manage accordingly.

Richard Brock is owner and president of Brock Associates, an agricultural marketing advisory service and publisher of The Brock Report.