The past two years have brought absolute chaos in the commodity markets and unfortunately, it’s not over

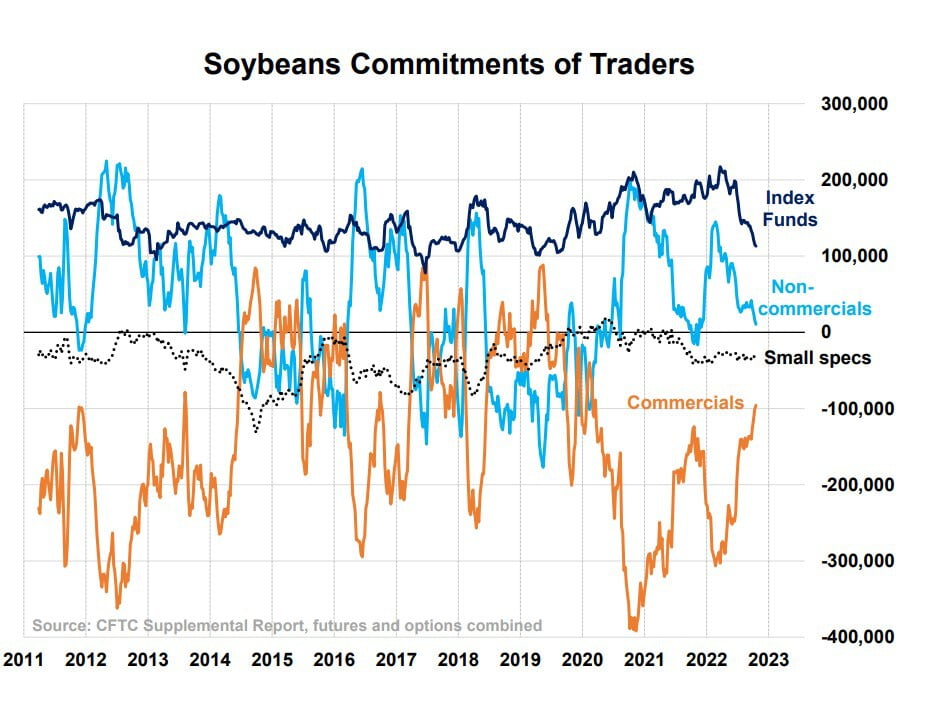

By RICHARD BROCK, Brock & Associates Over the past two years, we have all witnessed a pandemic, a war in Ukraine and the craziest political environment any of us have ever witnessed. Combine that with soaring inflation and interest rates that we haven’t seen since the 1980s. The result has been absolute chaos in the commodity markets and unfortunately, it’s not over. The two charts below reveal some interesting observations in the commodity markets. First let’s take a look at the Commitments of Traders report for soybeans. This report is released weekly by the CFTC. It shows the net positions of the following four categories of traders: Index funds (who are always long), Commercials, Non-Commercials (often referred to as “large specs”, this category includes speculative commodity funds), and Nonreportables (sometimes referred to as “small specs”). What’s taking place now is very interesting in that all four groups are decreasing their net positions towards their smallest positions in years. Very few people are playing the game anymore. For example, since March, index funds have gone from being net long over 217,000 contracts to only just over 113,000 contracts as of October 18. They’ve cut their position almost in half. Why? The only logical answer is that investors have pulled their money out of these funds and are instead going to more conservative investments where they can make 4-5% with no risk. Also, it could reflect a change in the majority of opinions from being bullish commodity prices to bearish.

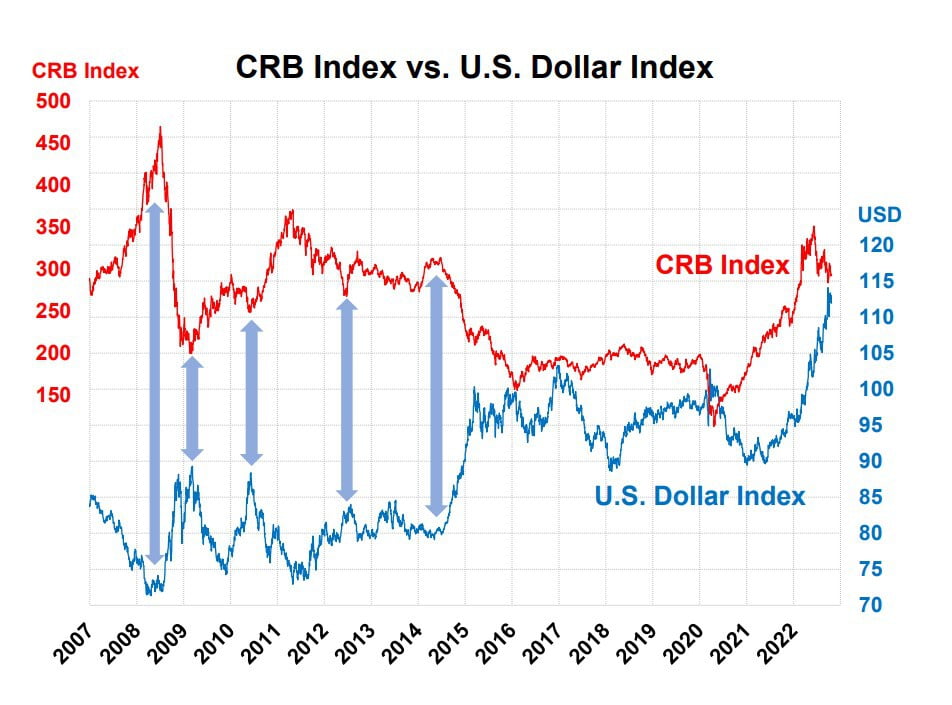

During the same time frame, the Commercial category has gone from being short over 300,000 contracts to short only 100,000 contracts. And the Non-commercials (large speculative funds) have gone from being long approximately 140,000 contracts to just 11,000 contracts as of October 18. With very few people now playing the game, it becomes easier to understand why the soybean market can have 25 cent price ranges every day because it no longer takes much to push the market around. This is not a healthy environment for markets. All markets need liquidity to facilitate hedging and trading. That is starting to go away. Strong U.S. Dollar Up until about a year and a half ago, there was usually a very predictable relationship between the U.S. dollar and the Thomson Reuters CRB Index. The two series usually exhibit a strong inverse correlation. Note in the chart for example, the dollar rallied sharply from 2008 into 2009 while commodity prices dropped like a rock. As time progressed through 2015, a strong dollar resulted in weak commodity prices and vice versa. This inverse relationship continued until mid-2021. Since then, the dollar skyrocketed to 20-year highs while the CRB index climbed to 11-year highs. The world changed fundamentally since 2021, and the two series exhibited a strong positive correlation that lasted until June of this year. The question now is, will the traditional relationship between the U.S. dollar and commodities continue perform as they have historically (i.e. remain inversely correlated) as the world economy starts to weaken?

Interest rates have now risen to levels not seen since the 1980s, making the U.S. dollar and U.S. denominated assets more desirable relative to many other alternatives. Demand for commodities has increased substantially in a (mostly) post-Covid world. Higher demand for protein (livestock), grain for ethanol and other usages, lumber, steel, and most everything else has risen sharply. Technically, the value of the U.S. dollar looks like it has already made a top. But we don’t think it will drop sharply, however, because the U.S. dollar is still the safest currency in the world. If the world enters a recession, will this have a negative impact on all commodity prices as typically happens in a recession? This is certainly a scenario that we all should be considering in our businesses. It is hard to find anyone involved in agriculture that thinks corn or soybean prices can go down. The industry is full of bullish sentiment. That may be the case, but let us remember that those were the same attitudes that existed in 2008 and 2012 before grain market prices took a big dive. Markets always peak on bullish news, not bearish news.It will be interesting to see what the world looks like 12 months from now.