World in chaos

The good news is that everyone has to eat. Historically, wars have had limited impact on agricultural commodity prices.

By Richard Brock, Brock Associates

War is raging in Gaza. It is overshadowing the war in Ukraine. The U.S. is in political chaos—even worse than normal. It’s got to the stage where I’m afraid to watch the news and am considering going back to my childhood and watching cartoons. More entertaining and will probably sleep better at night.

Unfortunately, that is not reality. We all need to know what is going on and hopefully what we are seeing and believing is true. That’s not always the case. In last week’s November Crop Report the USDA threw a zinger by increasing corn yields by 1.9 bushels per acre. That’s a shocker that sent corn prices lower for two days—but only two days.

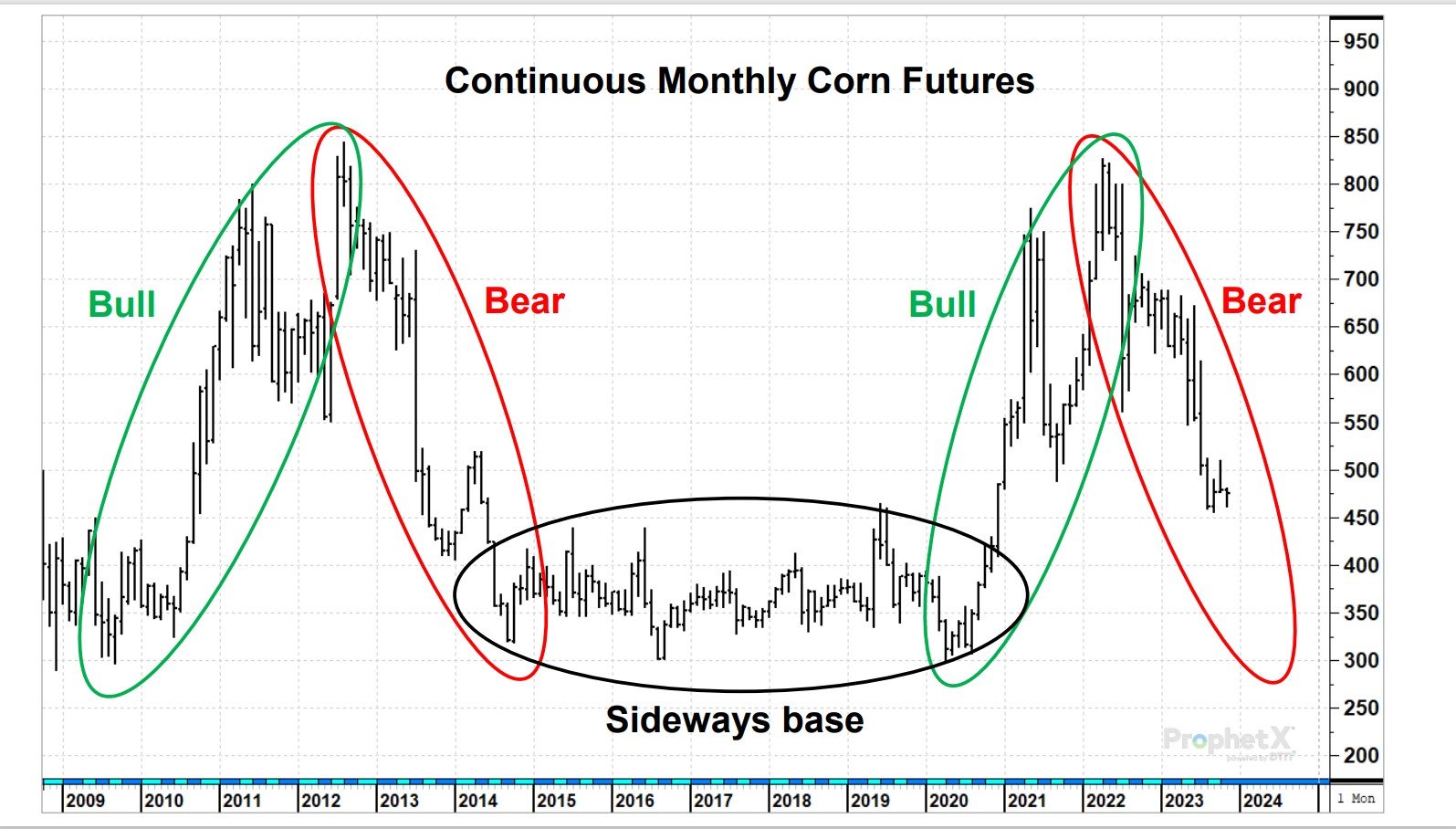

The chart below, while only covering the corn market back to 2009, shows two distinct bull markets, two distinct bear markets and one sideways trading range market that lasted from 2014 to 2020. For those of you in the feed business, recognizing how long these trends last is significant. How you manage purchasing programs is even more significant. The last bear market in corn lasted from 2012 to 2014. This one started in 2022 and will likely bottom in 2024 if it hasn’t already.

Impact of War on Prices

The good news is that everyone has to eat. Historically, wars have had limited impact on agricultural commodity prices. The ones that are going on now will not drastically impact shipping channels or production since none of the countries involved are very large at grain production. Some can claim that Ukraine is a large producer of wheat and corn, but their production has always gone through the Black Sea routes or to eastern Europe. Their war has resulted in us picking up essentially no new corn exports at all.

Throughout all this, the demand for poultry is going to remain very strong. Pork pricing has been competitive. Beef at the retail level is not competitive. That is showing up in lower per capita consumption on the beef side, increased demand for poultry, and flat demand for pork.

On the purchasing side for corn, with a projected ending stocks-to-usage ratio of over 15%, this is not going to be a runaway bull market. It could be a market making a bottom, but certainly not one ready to start a bull move to the upside. There will be some blips to the upside but before any major upward price move is going to occur, the corn market needs to go through a base-building phase. This one will not likely be

as long as the last one, which was six years, but two to three years could certainly be expected.

It's time to get ready for the winter doldrums in grain prices overall. The primary influence for soybeans now is South American weather where the state of Mato Grosso in Brazil is experiencing a significant drought. The next 10 days are going to be important in that country. If rain does not occur soon, soybeans and soybean meal are going to catapult to new highs. Manage accordingly.