The next six months are probably going to be even more volatile, says Richard Brock

By RICHARD BROCK, BROCK ASSOCIATESAs Thanksgiving approached, the corn basis in eastern Nebraska was 80 over December futures and in western New York, it was 30 under December. A normal basis in eastern Nebraska over the last few years has been 50 to 70 under, and in western New York, 30 to 70 over. About the time you think you’ve seen everything you’ve actually seen nothing.

This has made for a very challenging environment for livestock operations in the western Corn Belt. Paying such a premium is hurting bottom lines and more important, just securing enough corn can be a challenge. What happened? A good comparison is when companies who build hotels all act on the same survey of a city at the same time and conclude there is a shortage of hotel rooms. They all start building at the same time and in two years there is a surplus of hotel rooms. In this case, several industries, particularly the poultry industry, decided to construct facilities where corn was “cheap”. Then, all of a sudden, the demand for corn in the western Corn Belt for poultry, pork and ethanol is outreaching the supply. Combine that with the fact that in the last four years the western Corn Belt has not seen any increases in yields and production has been flat, while in the eastern Corn Belt, production has been strong. It has been strong in Ontario, Canada, and corn is coming in from the north. Two totally different environments than what existed three years ago.

On top of that, a 73-acre farm in northwest Iowa with no development potential sold for $30,000 an acre just a week ago. Two farmers each decided they had to have it. While that is an unusual sale, $16,000 to $25,000 per acre in the central Corn Belt has become commonplace.

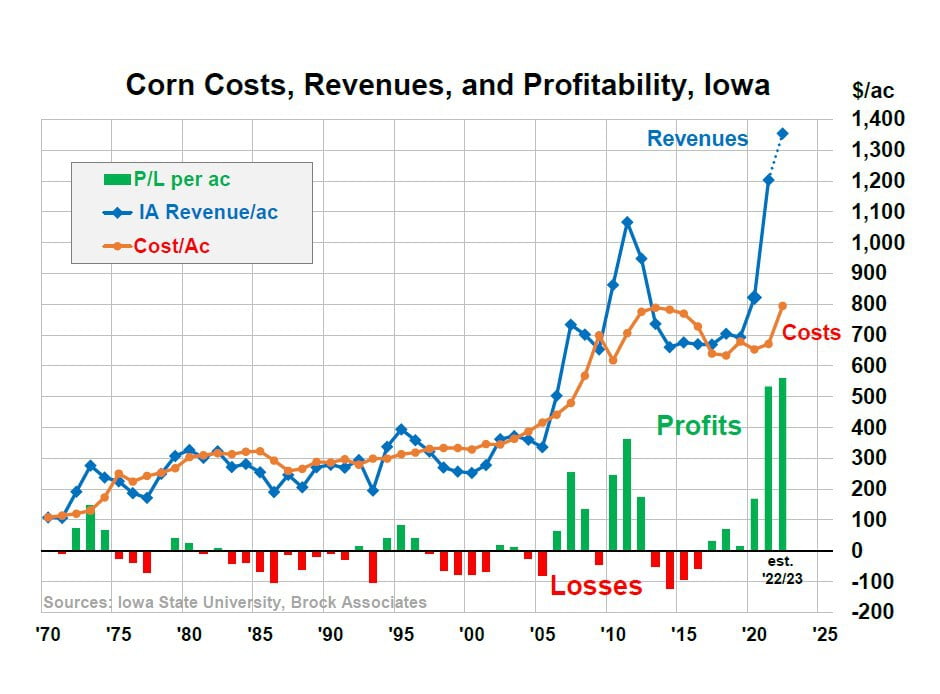

That could all change relatively soon. Profits in corn production run in cycles just like everything else. The chart below shows that corn producers have had six years of large profits. That’s the most in history. With rising input prices and declining corn prices, 2023 is going to be a different picture.

Issues for 2023

Here are just a few of the issues we need to take into consideration in agribusiness in 2023:

Higher interest rates—going to impact everyone’s bottom line.

Input and labor prices are sky high.

Electric vehicles—impact on ethanol usage. If some of the predictions are right, by 2027, 25% of the vehicles on the road will be electric. That would certainly cut back corn usage for ethanol which currently accounts for about 37% of total corn usage.

The green revolution will continue to have an impact on agribusiness.

Renewable diesel. How fast are plants going to get built? Will increases in soybean production in Brazil offset the increased usage here? Will it result in most of China’s soybean purchases coming from Brazil and not the U.S.?

Animal rights activists continue to make our industry more challenging.

Changes in consumer preferences. The growth rate of the organic food industry is slowing.

The economy, even if this administration doesn’t want to admit it, is in a deep recession. Massive layoffs in high-tech companies is changing the workforce.

The automobile industry is going to change quickly. Already the supply of new cars has ramped up considerably. No more sharp markups in price. The used car inventory is going to get very depressed, very soon, as online companies who have loaded up on higher priced vehicles will have to move them to the market at losses. Going to be a major change.

Inflation is stifling consumer demand. The housing boom is stalled. Developers have overbuilt condos and apartments. Could be a very depressed market, and very soon.

Changes are Happening

Just when we thought we’d seen all the changes that are possible, the next six months are probably going to be even more volatile.