Law of economics still work

From what the trade was expecting prior to the release of the May crop report, overall production in carryover supplies came in lower than expected. Analyst Richard Brock digs in.

By Richard Brock, Brock AssociatesOn May 10 the USDA released the May WASDE report. It confirmed the laws of economics are alive and well. Keep the price of any commodity (in this case corn and soybeans) too high for too long and users will find a way to use something else and growers will find a way to grow more. Get the price down for an extended period and usage will go up.

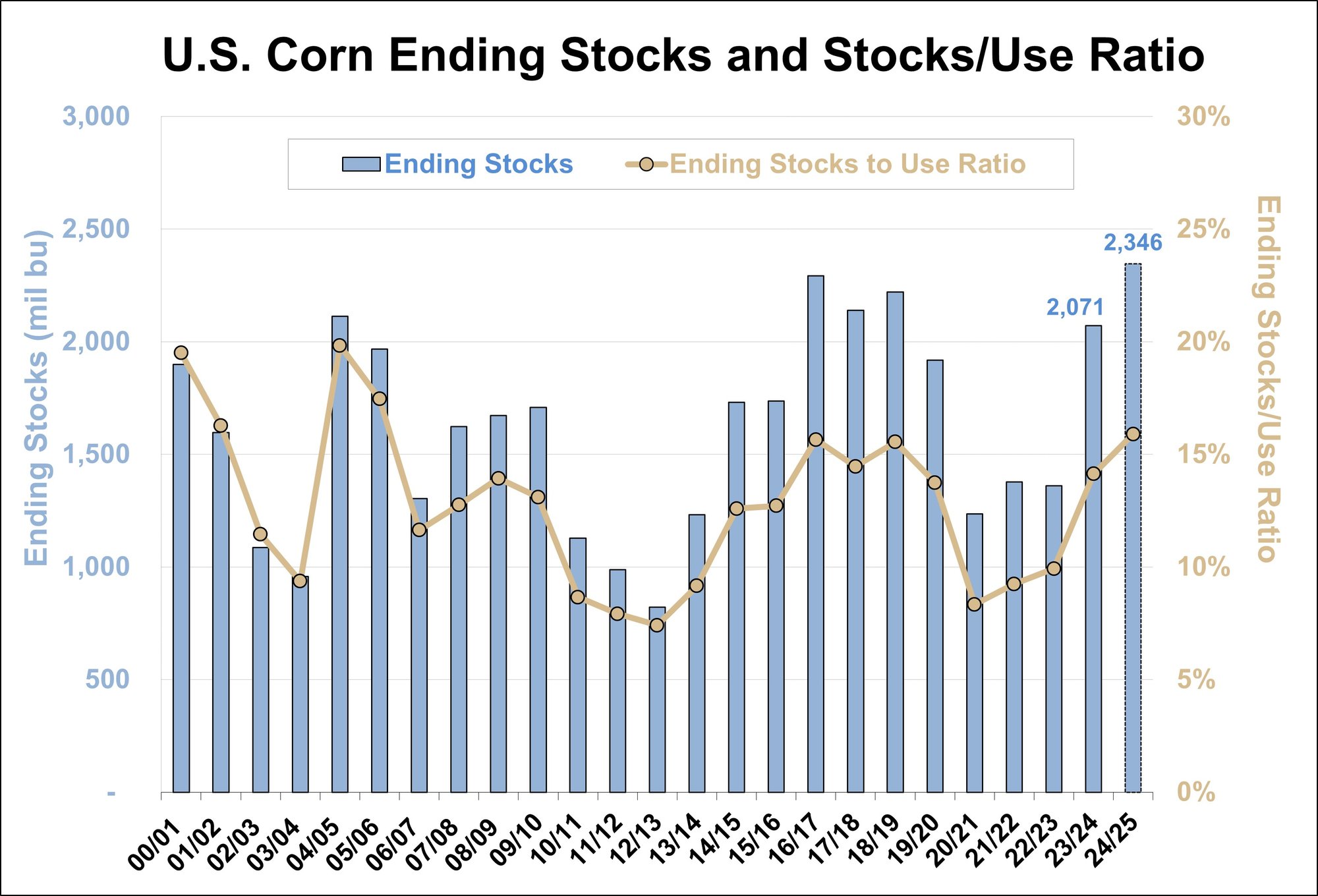

More specifically, in the report released on the 10th of May, USDA increased feed usage of corn from 5.7 billion bushels in 2023/24 to 5.75 in 2024/25. In 2022/23 it was 5.486. Exports have gone from 1.66 billion bushels in 2022/23 to an estimated 2.2 billion this year. They lowered the expected average price from $6.54 per bushel in 2022/23 to $4.65 for the 2023/24 crop and $4.40 for the 2024/25 crop. With December 2024 corn futures trading at $4.95 as I write this, it will require some very serious production problems for corn futures to go much higher than they are now. Certainly, possible in the short-term until the crop gets entirely planted, but from what we can see right now I would expect the highest price for corn futures between now and harvest to occur between now and mid-June.

Soybeans a More Dramatic Shift

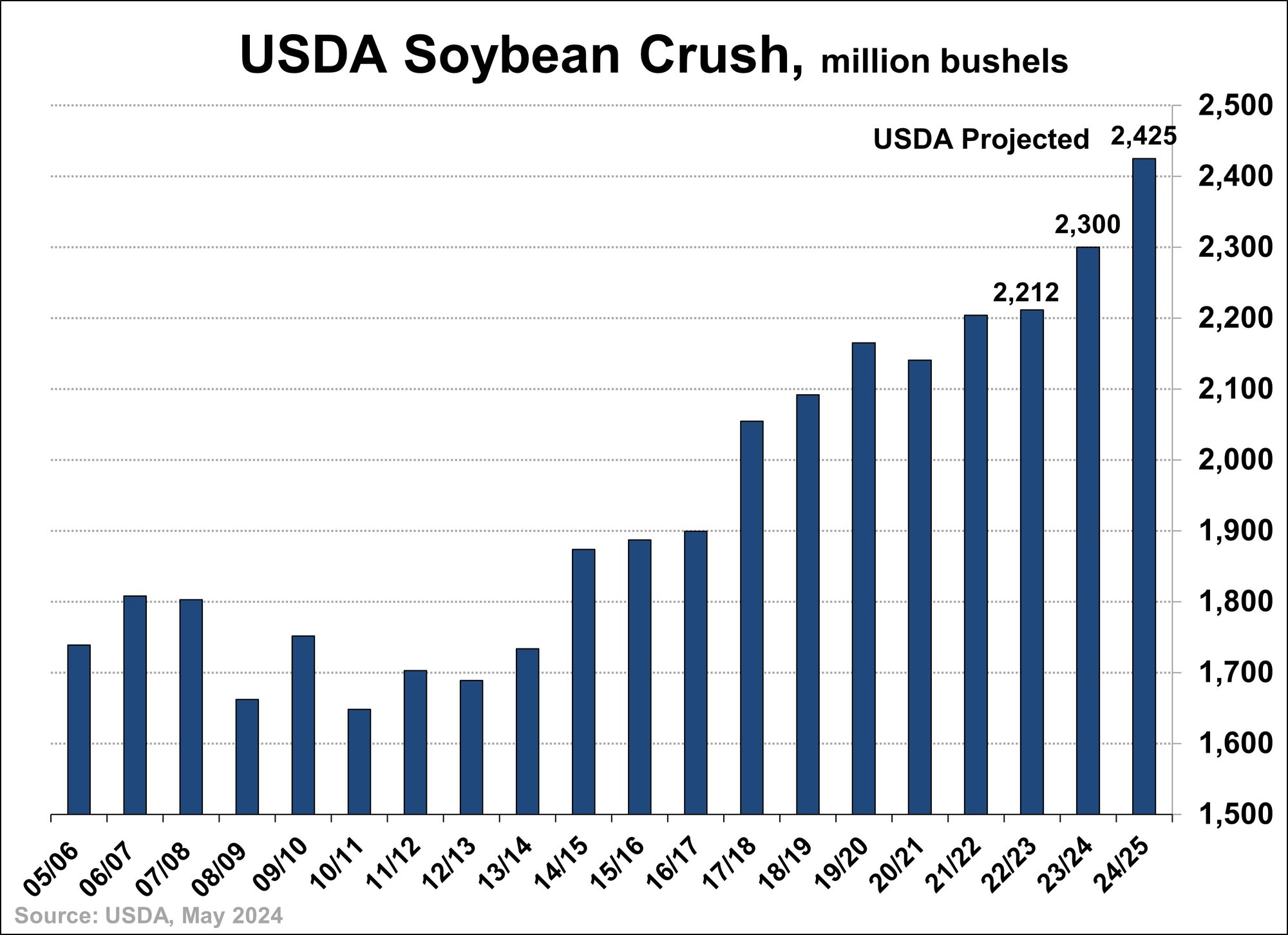

In the 2022/23 marketing year soybean crush was 2.2 billion bushels. 2.3 billion during this marketing year and is forecast to be 2.425 billion for the 2024/25 season. In addition, the USDA forecast exports to increase from 1.7 to 1.825 billion bushels. Even with that, carryover is expected to increase from 340 to 445 million bushels. This compares to only 264 million in the 2022/23 crop. The expected average price for the 2024/25 crop is now forecast by USDA to be $11.20 per bushel. November 2024 soybeans are trading at $12.05 as I write this. One does not need a calculator to recognize that soybean prices are overpriced relative to the supply and demand balance sheet.

Soybean meal prices are even more obvious. The carryover of soybean meal in 2022/23 was 371,000 short tons. This year is 400,000 and the 2024/25 crop is expected to be 450,000. Average price of soybean meal this year estimated at $380. For the new crop it is expected to average $330. December soybean meal is trading at $375 as I write this. As is the case in both corn and soybeans, we feel confident that there is more potential for the market to go down than there is to go up.

Putting It All Together

From what the trade was expecting prior to the release of the May crop report, overall production in carryover supplies came in lower than expected. Still big but not as big as was built into the market. These are not bullish balance sheets, just less bearish than expected.

This is not going to result in a bull market in corn, soybeans, soybean meal or soybean oil. It will allow some stabilization in price and may also limit significant downside from this price level. Market tops peak quickly and drop fast. Market bottoms take a long time. This one will not likely be any different.