May crop report full of surprises

The May USDA Crop Report released on May 12 was full of bearish surprises—at least on the surface, says Richard Brock

By Richard Brock, Brock Associates

The May USDA Crop Report released on May 12 was full of bearish surprises—at least on the surface. If Mother Nature cooperates and produces a large corn and soybean crop as the USDA has forecast, that will be the case. Much lower prices. But first the crop needs to be grown and that’s a long way off.

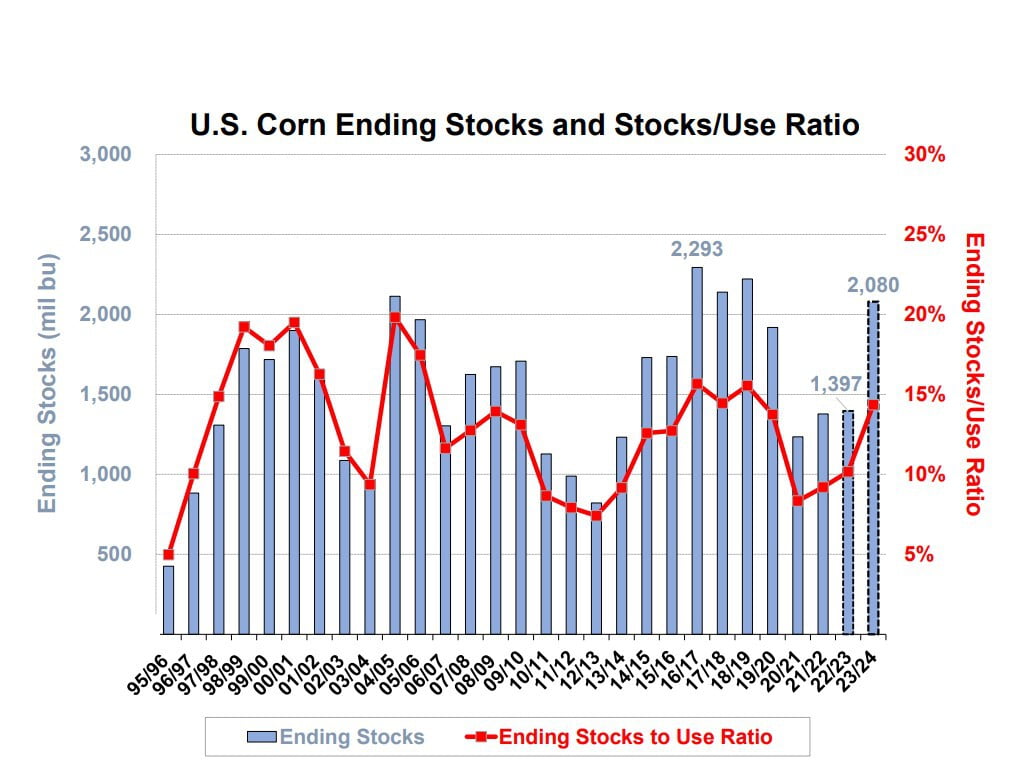

To begin with, the USDA is forecasting 92.0 million acres of corn will be planted this spring versus 88.6 million last year. The expected carryover is forecast to be 2.222 billion bushels. The highest in recent history was 2016/17 when the carryover was 2.293. As the graphic below indicates, our estimated 2022/23 carryover of 2.08 billion bushels is still sky high, but lower than the USDA’s. Both estimates are substantially above the 2022/23 crop carryout of 1.397.

For the past three years, major production problems have occurred in at least one of the top six corn producing states. Last year, Nebraska suffered substantial wind damage. The year before that, there were weather issues in Iowa and Minnesota. Not since the 2016/17 crop year have all top-six corn states been hitting on all cylinders. Time will tell if that happens this year.

A more negative factor that very few people are talking about is producers’ marketing strategies this year. For the last two years, it has not paid to be an aggressive forward seller. As is typically the case, after two years of selling early and it not working out, this year farmers are storing more corn (as a percentage of total March 1 corn stocks) than they have in the prior two years, and they have sold very little new-crop corn. That sets the stage for depressed cash prices at the end of this marketing season in August and going into September of the new crop.

World soybean supplies to shoot higher

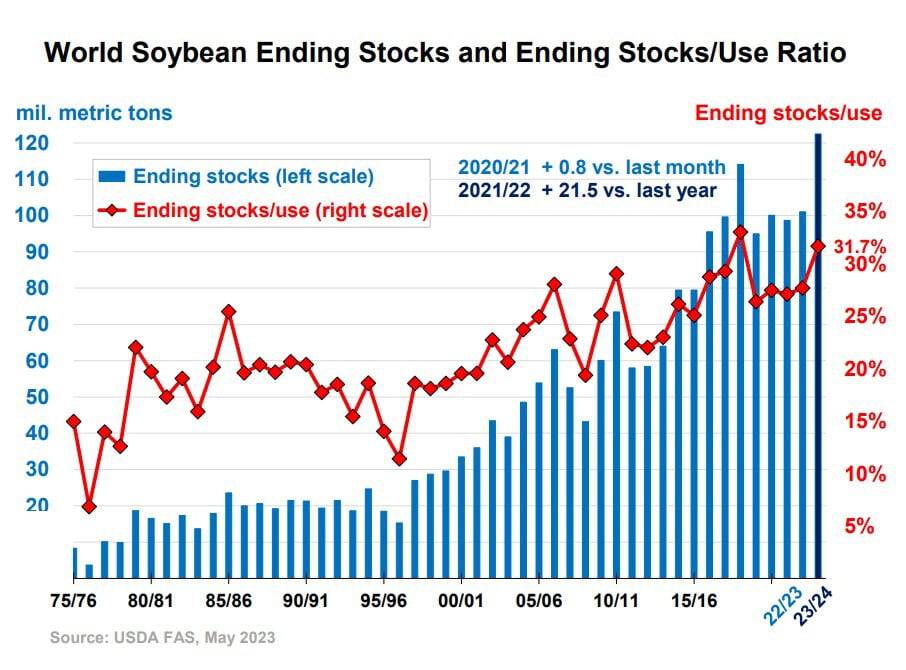

Another big surprise in the May Crop Report were the projections for world soybean production and 2023/24 carryout. Projected world soybean carryover is 122.5 million metric tons (mmt). That is a sharp increase from last year’s 101.0 mmt. Where is the increase coming from? United States soybean production in 2022/23 was 116.4 mmt but is projected to rise to 122.7 for the 2023/24 crop. Brazil’s 2023/24 production is projected to increase to 163.0 mmt from 155.0 mmt this past year. Almost all major world soybean producers are seeing significant increases which is typical after having two years of very high prices.

Eventually this will lead to significantly lower soybean and soybean meal prices. However, buyers should not count on seeing that soon. A late spring and excess moisture led to planting delays in isolated areas, but lost acreage and replanted areas should be more than offset by the majority of areas that got off to a timely start.

At this stage, my estimate would be that prices of corn, soybeans, and soybean meal will stay relatively firm until late June/early July. Could we be looking at a classic mid-summer high sometime near the 4th of July? Very possible. But longer-term, the odds favor lower prices.