Extreme price volatility ahead

It’s always difficult to make money when grain prices are flat with very little movement. That is not going to be an issue over the next few months, says Richard Brock.

By Richard Brock

One of the keys to profitability in the feed industry, one of many, is price volatility. It’s always difficult to make money when grain prices are flat with very little movement. That is not going to be an issue over the next few months.

I’m writing this the day after Israel started attacking Iran. It’s important to know that because by the time you read this, in such a volatile world, who knows what could be going on. Every day is different now. As a result of the fighting in the Middle East, however, energy prices have risen sharply. That is probably not yet over. It is interesting, however, the impact on agricultural prices is. We expect following impact on commodity prices:

Soybean oil will be extremely strong. That will help the soybean complex and drag meal along. Meal doesn’t have the fundamentals to rally alone but the soybean oil will contribute.

Corn prices will have a minimal impact. Spread prices are running now at about 80% of carry which is an indication that commercial companies are anticipating a big crop. It will be a good year to be in the storage business.

Livestock prices are going to be under pressure. After a major extended bull market in both cattle and hogs, the move appears to be winding down. Nothing is confirmed yet but there is much more downside risk in cattle and hog prices at current levels than there is upside potential.

Wheat Will Be a Surprise

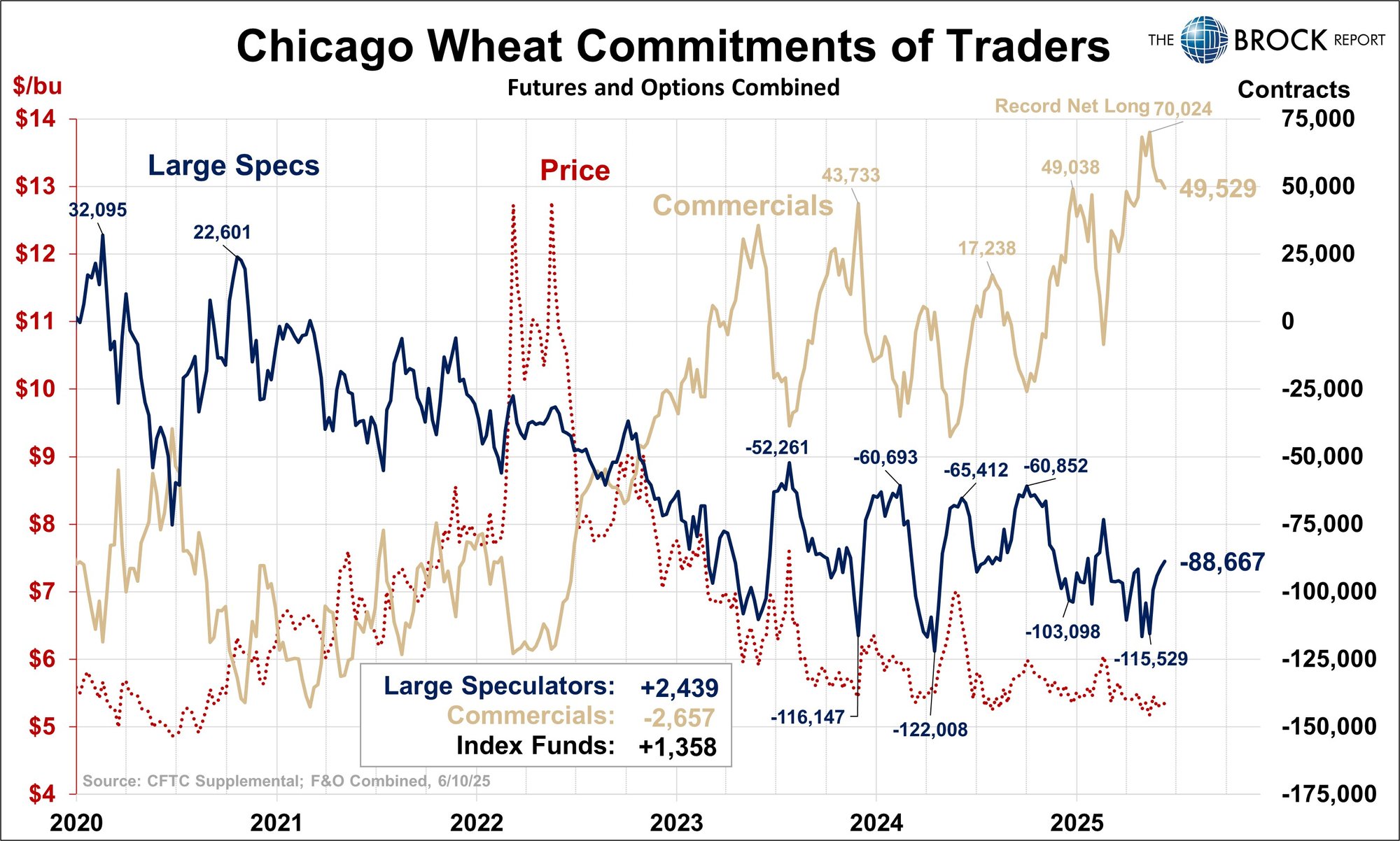

It seems as though most of the trade continues to be bearish wheat. I think that’s the wrong side of this market. Markets bottom out on bearish news. Wheat is a classic example.

The Commitment of Traders report below is very useful. Note that commercial companies currently have a record net long position in wheat. The short position is held primarily by large specs—the commodity funds. When commercials are on one side and the commodity funds are on the other, expect the market to turn in favor of the commercial position. In this case, if they want to own wheat I want to own it with them. This is a bear market that has run its course. For those of you who buy wheat or wheat related products, it is time to be aggressive. The upside potential on wheat prices far exceeds the downside risk.

Richard A. Brock is Chairman of Brock Holding Company which is comprised of Brock Associates, an agricultural marketing advisory service and publisher of The Brock Report, established in 1980 and Brock Investor Services (futures and options brokers). The firm, based in Milwaukee, WI, now has six offices and manages grain sales on approximately 800,000 acres throughout the U.S. and is an advisor on purchasing strategies for many large poultry, pork, dairy and food companies.