Getting ready for commodity price doldrums

Markets are up. Markets are down. What's ahead? Richard Brock shares his insight on what he sees for upcoming commodity prices.

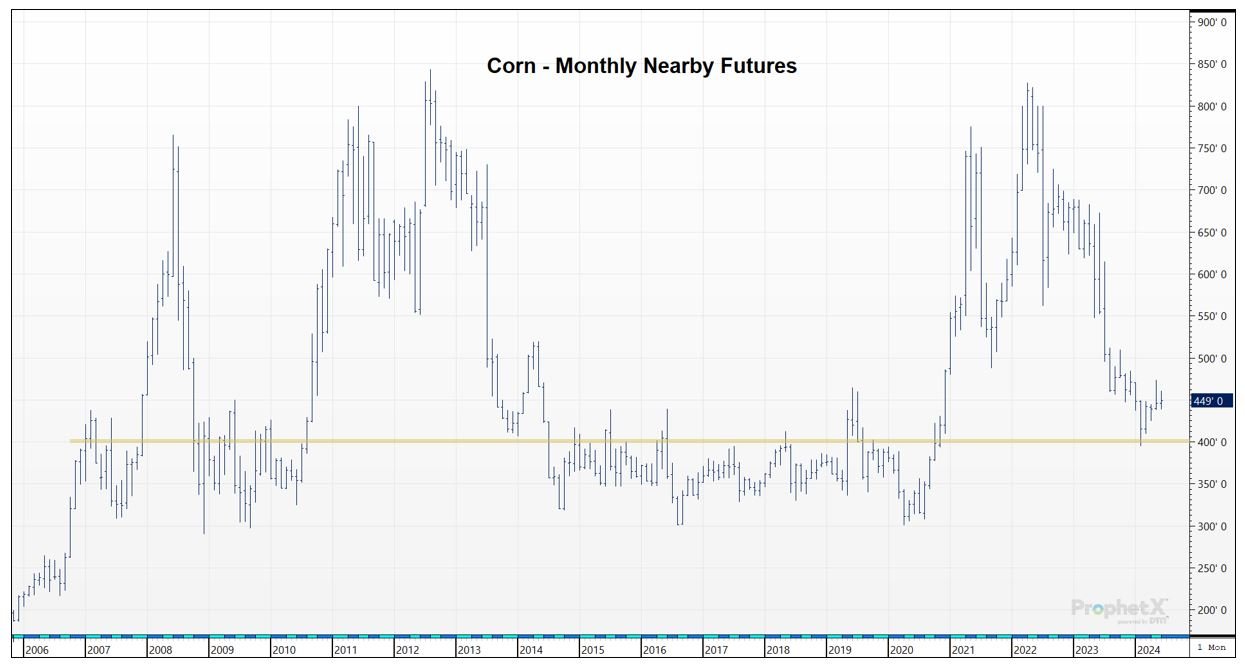

By Richard Brock, Brock AssociatesThe chart tells a very important story. The price pattern starting in 2022 is almost identical to the price pattern that started 10 years earlier in 2012. 2013 lines up with 2023 and 2014 lines up with 2024. Now the question is will 2014 – 2020 repeat itself?

Impossible to tell for sure but we think the odds are reasonable once the corn market finds a bottom, and we don’t think it has yet. Prices will have to go through a base building phase. It could take two to three years, possibly longer. With a stocks-to- usage ratio of over 14% (a carryover of 2.1 billion bushels) time will be needed to increase usage. There are only three years since 2007 that the stocks-to-usage ratio has been higher than this year. Those years were 2016, 2017 and 2018. In 2016 and 2018 the stocks-to-usage ratio was slightly over 15%.

The good news is for the grain merchandizing business where corn prices have gone from being inverted in the years of 2021 and 2022 to near carrying charges. Grain elevators are now making back many of the lost profits of three years ago. But markets that have now shifted to carrying charges are the first indication that corn prices are going flat.

As this is written, the good-to-excellent ratings of the corn crop are higher than they have been in years. Ratings always come down from where they start but with the central Midwest being in very good shape and more than adequate moisture, it is unlikely that carryover is going to diminish much this year.

How low is low?

The first target is the old resistance which is now support at $4.00 per bushel in the nearby futures. It is only a guess, but I would have to think that $4.00 will hold any selloffs. To expect corn to go into a trading range of $4.00 to $4.80 would be a realistic expectation.

Soybeans and soybean meal could do the same. The lows of all these markets may well be in but supplies are too large for any meaningful bull market. Price volatility will not be as high as it was from 2020 to 2023.