The importance of a purchasing plan

Analyst Richard Brock shares his views on the market

By Richard Brock, Brock Associates

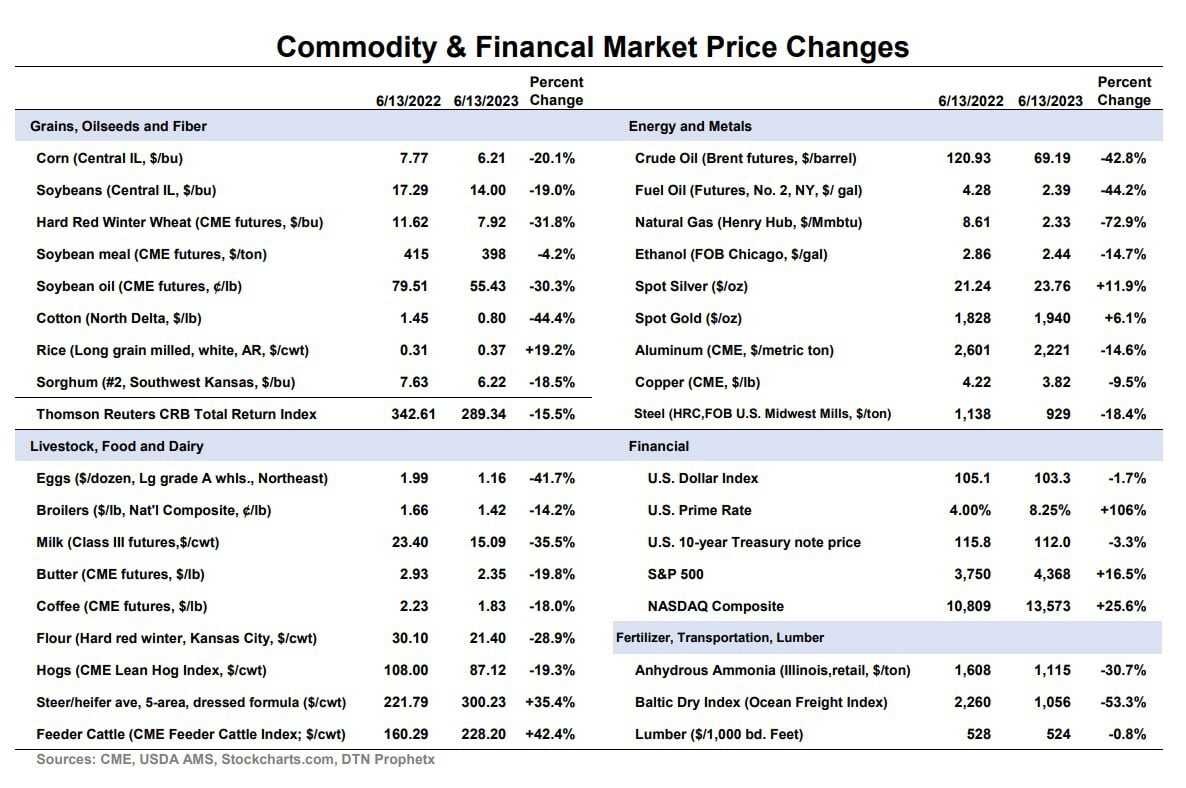

Whether you are a farmer selling ag commodities, a feed manufacturer, or an end-user of feed commodities, today’s price volatility underscores the importance of having a well-defined risk management plan. The table outlines some of the significant price changes that have occurred in just the last twelve months. On the grain side, farmers’ profits are being squeezed. Over the past year, corn is down 20%, soybeans are down 19%, and hard red winter wheat is down 31%. Eggs are down 41%, broilers down 14%, and milk is down 35%. A steep drop in energy prices has also been to the benefit of end-users with crude oil down 42% and natural gas down 73%.

The price drops have created very good buying opportunities for feed companies, but one price change that is hurting both buyers and sellers is the price of money … over the past year, the prime lending rate has gone from 4.00% to 8.25%.

What now?

So much for history. Hindsight is a wonderful thing in commodity trading. Here are my thoughts on several commodities over the next few months:

Corn and soybean complex: By harvest time, unless a major production disaster occurs, expect corn and soybean meal prices to be lower. Over the next 3-4 weeks, however, unless rain comes back into the forecast there could be and most likely will be a significant price rally in corn and soybeans. Should it occur, it is an opportunity for producers to catch up on selling and not one for buyers to panic.

Cattle and hog prices: They are going to go in opposite directions. The cattle and feeder cattle market, in my opinion, has seen a price peak for the year. The dramatic move to the upside discounted supply shortages very quickly and more importantly, hurt demand. Due in large part to diminishing beef supplies, USDA is projecting U.S. per capita beef consumption to drop by 7.8% next year, which would be to the lowest level in over 60 years. Per capita pork consumption is relatively inelastic and rarely changes much at all. Per capita poultry consumption is more elastic, and since it is the best buy in the grocery store per pound of protein, per capita consumption keeps climbing higher every year.

While cattle prices in the futures market have discounted the bullish news, the opposite is true in the pork industry. The sharp drop in prices during the spring has resulted in a modest increase in sow liquidation. Pork production will continue to decline into the third quarter before rebounding in Q4. Buyers of pork should be aggressive on any dips, and sellers should be standing on the sidelines watching.

Richard Brock is owner and president of Brock Associates, an agricultural marketing advisory service and publisher of The Brock Report, a 20 page weekly fundamental and technical newsletter. His firm, now with seven offices, manages grain sales on over 700,000 acres throughout the U.S. and is an advisor on purchasing strategies for many large poultry, pork, dairy and food companies. Brock is on retainer with several agri-business firms for his input on strategic planning. He writes a monthly column for Delta Farm Press and Feedstuffs magazines and speaks at over 50 conventions and conferences per year.