Narrowing the odds

Current odds do not favor a record-breaking yield or a collapse on yield, says Richard Brock

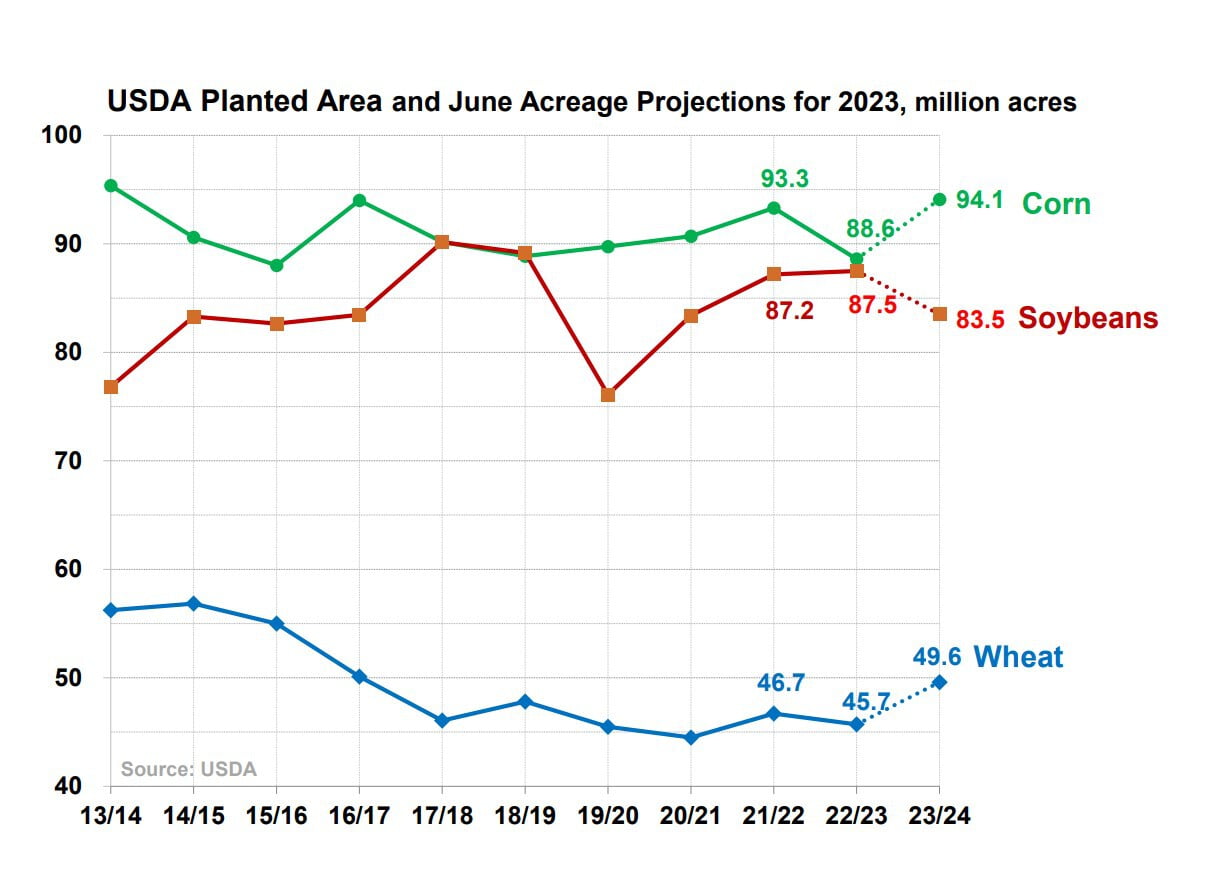

By Richard Brock, Brock AssociatesNow that the growing season for corn and soybeans is past the middle of July, we can start narrowing the price ranges for both commodities. The USDA threw a zinger at everyone recently by changing the planted acreage of both corn and beans significantly from the March Intentions report. They added 2.1 million acres to corn bringing the total planted acreage to 94.1 million acres and lowered soybean plantings by a whopping 4.0 million acres dropping the planted acreage to 83.5 million acres.

As the graphic indicates, this is the highest planted acreage in corn since 2013. 83.5 million acres of soybeans is the lowest since 2020.

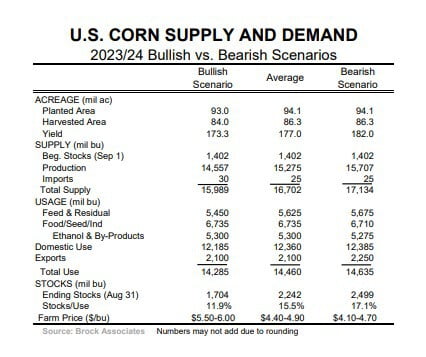

Bullish vs. Bearish Scenarios

In the graphic showing our Bullish vs. Bearish scenarios, the middle column shows Brock Associates average estimate for the corn supply/demand balance sheet for 2023/24. In the bullish scenario, let’s assume that the USDA overstated planted acreage and the final number comes in at 93 million acres with a harvested acreage of 84.0 million. Let’s also assume a much lower yield and peg it at 173.3 bushels per acre. Weather conditions throughout the Midwest at this stage do not lend credence to a yield any lower than this. Under this scenario, our estimate is that ending stocks would drop to about 1.7 billion bushels with an ending stocks-to-usage ratio of 11.9%. Even under this scenario the average price of corn in central Illinois would struggle to get above $5.75.

On the other hand, let’s assume the rains keep coming and the national average yield ends up at 182. This would be our bearish scenario. The ending stocks-to-usage ratio would jump to 17.1% and cash corn prices in central Iowa would likely start with a “3”.

The much more likely scenario would be a yield of 177 which would result in an ending stocks-to-usage ratio of 15.5%. Only two times in recent history has the stocks to usage ratio been this high. Those years were 2016 and 2018. In both of those years, the national average cash price for the marketing year was $3.50, give or take a dime.

The Bottom Line

Current odds do not favor either a record-breaking yield on the high side or a collapse in yield on the low side. As in almost any growing season, there is some corn that is in great shape, and some in very poor shape, but the majority is average to slightly above. Also, genetic improvements to corn for drought resistance has removed much of the concern that plagued corn crops 20 years ago. At this stage, the bulls in the corn market need to start betting on an early frost.