January crop report a game changer

It is going to be a very volatile time in corn prices this spring and summer, says analyst Richard Brock.

By Richard BrockIt’s the commodity business. Things can change fast. January was a good example. Since August 26, May corn futures rallied 76 cents and the cash corn basis improved over 25 cents in most areas and thus farmers were receiving more than a dollar per bushel for cash corn in mid-January than they were in early September. That changes not only cash flows but attitudes even more so.

There is a big difference between bull and bear markets in corn. A bear market needs no news at all. Bear markets fall from their own weight. Bull markets need new bullish news almost every day. The corn market over the last several weeks has been overwhelmed with bullish news. That has kept the drive to higher prices going longer than expected and now the question on everyone’s mind is whether or not the move is over.

What changed? The January crop report lowered the yield on this past year’s corn crop from a previous estimate of 183.1 bushels per acre to 179.3. That in turn lowered the total crop by 276 million bushels and resulted in an ending stocks number going from 1.738 billion bushels to 1.54 billion bushels. Possibly one of the biggest changes made in one report in over 10 years.

More importantly it lowered the stocks-to-usage ratio to approximately 10%, which raised the expected average price of corn by nearly 70 cents. Now instead of farmers hoping to average only above $4.00 per bushel, the expectations are in the high $4.00 and low $5.00 range. That is the difference between losing money and making a little.

World has changed as well

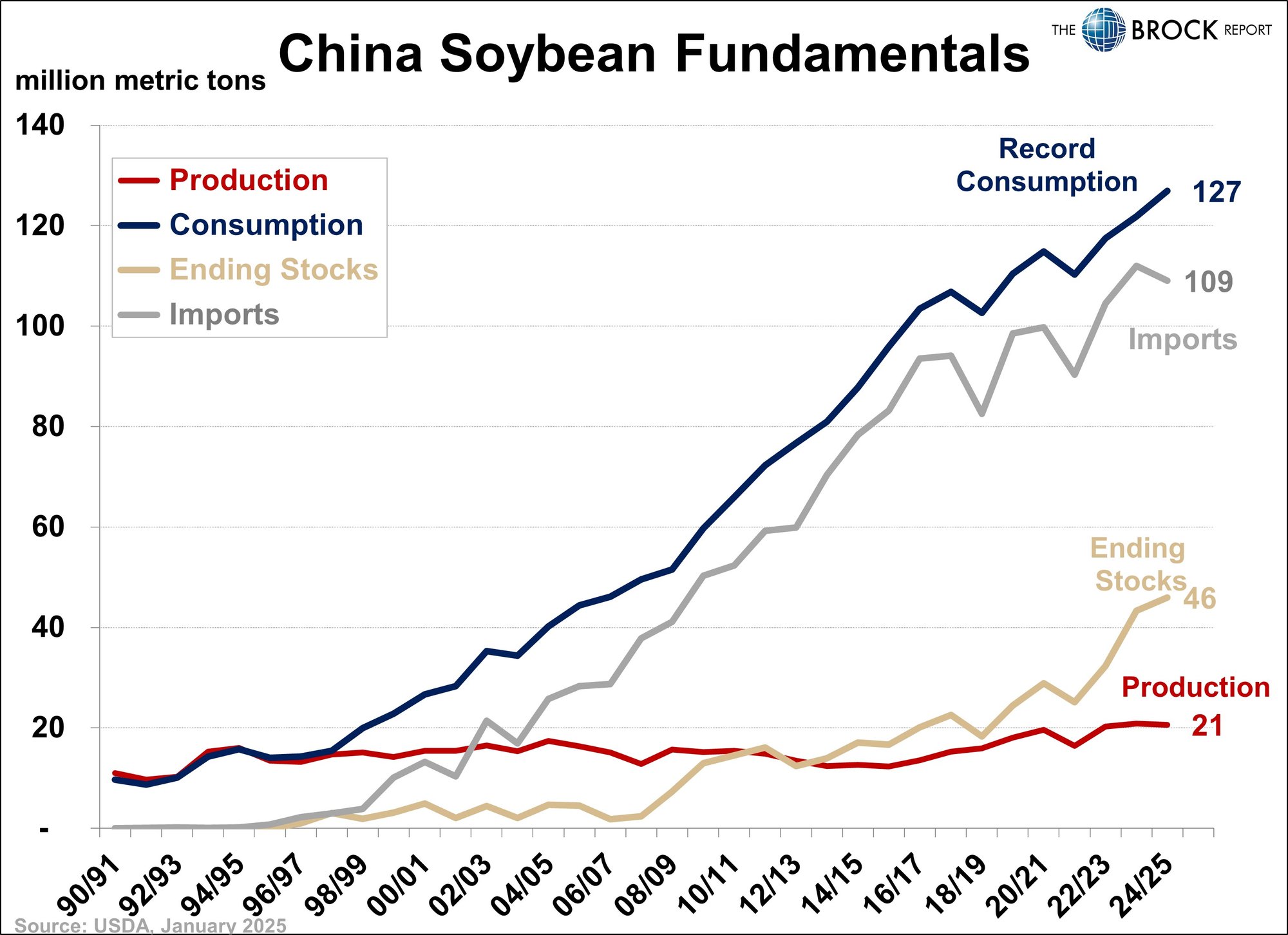

The graph below shows China corn fundamentals. The country is having record consumption but also record production. Note that ending stocks, however, are 65% of usage whereas here in the U.S. our stocks-to-usage ratio is now 10%. Clearly policies changed in China starting at about 2012. One has to wonder why the Chinese government wants such a large supply of corn. Could it be for food security? Or is it for military security in case of a war?

Another point of interest is imports. China has reneged on import levels of corn that were agreed upon with Trump in his last administration. Imports have gone from a high of 30 million metric tons in the 2020/21 marketing year to 13 million in this marketing year. Will Trump be able to get this corrected? Who knows?

Volatility is back

What is guaranteed with these changes is extreme price volatility. Two months ago, it appeared as though corn prices would go in the doldrums and stay in a long flat trading range. I doubt that will happen now. History indicates that the next month with high odds of corn making a top for the marketing year will not happen until May. Odds go up a lot in June. But since 1970 the top in the corn market has occurred in January only twice and in February only once. Prices may chop around but the overall bias over the next three months will be to the upside. This is coming in spite of almost everyone expecting corn acres to shoot sharply higher, possibly switching all the soybean acres that crossed over a year ago now going back to corn. Four million acres plus. That’s the bearish news but it’s also expected. It is going to be a very volatile time in corn prices this spring and summer.

Richard Brock is Chairman of Brock Holding Company which is comprised of Brock Associates, an agricultural marketing advisory service and publisher of The Brock Report, established in 1980 and Brock Investor Services (futures and options brokers).