September 1 marks the beginning of a new crop year for corn and soybeans. It couldn’t come any too soon.

By Richard Brock, Brock Associates

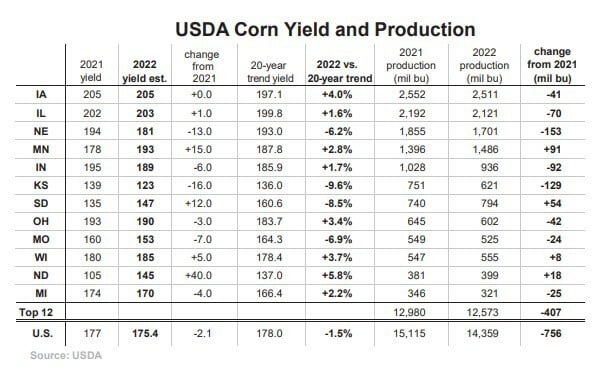

September 1 marks the beginning of a new crop year for corn and soybeans. It couldn’t come any too soon. The marketing year for the 2021/22 crop has been a roller coaster ride. One year ago, nearby corn futures were at $5.38/bu. and then peaked in April at $8.27 only to fall all the way back to $5.62 in July. Soybeans had a similar ride rallying from below $12.00 in September of 2021 to $17.84 in June and before July was over, prices had dropped back to nearly $14.00. Plenty of excitement for everyone. On the surface, the next 12 months do not appear to be nearly as volatile. Corn harvest in the south is well under way. Clients of ours in the northern Delta are reporting corn yields down about 10% from a year ago as a result of heat and dry weather. Some states have been hurt considerably, specifically Kentucky, Tennessee, and Arkansas. However, none of those states fall into the top 12 corn-producing states. Nationally, this will not be a record corn crop. As the Table from the USDA indicates shows, the state-by-state breakdown is a mixed bag. Iowa is in good shape but will still only match last year’s corn yield. Illinois is in a similar spot whereas Nebraska has been hurt by both drought and hail.

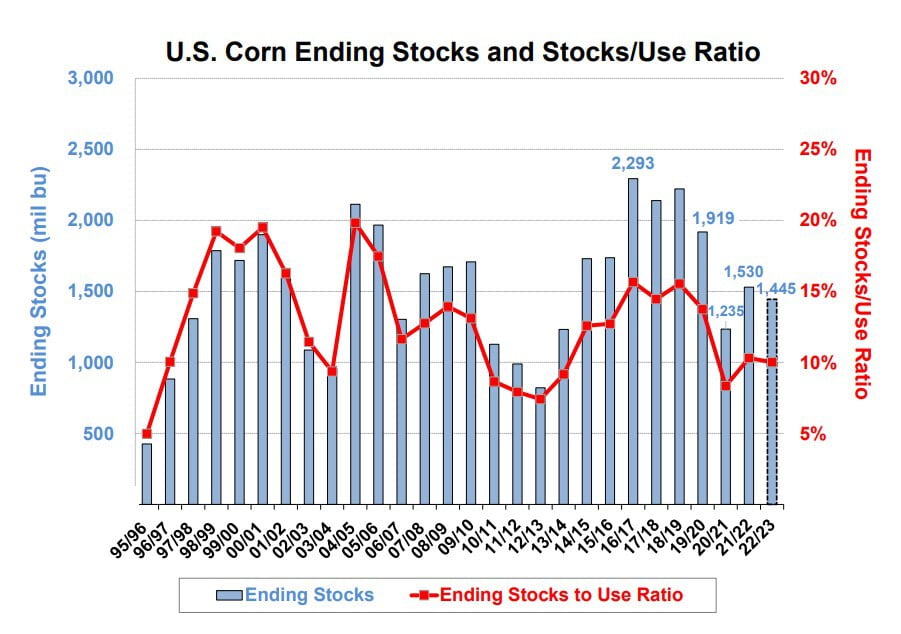

The U.S. Department of Agriculture’s estimated yield of 175.4 bu. per acre will likely be close. As the Figure shows, U.S. corn ending stocks and the end of the 2022/23 marketing year will be more than adequate. Slightly less than 2021/22, but well above the carryover in 2020/21.

War in Ukraine The history books will likely indicate that Putin made a significant mistake invading Ukraine. Estimated Russian casualties are over 60,000 and for what? To pick up a small sliver of land that with the bridges torn down, now Russian supplies cannot even get there. Nevertheless, geographically, because of the ports, the move has strategic benefits for Russia, but at a big cost. But even the impact on the corn and wheat market has been far less than what the press would like people to believe. Currently USDA is estimating this year’s Ukrainian corn production at 30 MMT versus 42.1 in 2021/22. Ukrainian's exports will also be down but will have negligible impact on the market.

With a projected ending stocks-to-use ratio in the U.S. of 10%, the expected average price should be approximately $6.00/bu. give or take 30 cents basis central Illinois. There will of course be some surprises along the way. It always happens. But overall, this would appear to be a much calmer year ahead in grain prices than what we suffered through these past 12 months. We could all use a more normal market. The world is a much different place than it was three years ago. The word “normal” has taken on a new meaning. The good news is that people will continue to eat and that is certainly good for our industry.

Commodity trading involves substantial risk of losses as well as profits when trading futures and options and past results are not indicative of future results. This brief statement does not disclose all risk aspects of derivative trading therefore careful study of Brock Associates Disclosure Document as well as carrying FCM’s Risk Disclosures is strongly encouraged. Redistribution or reproduction of this content is strictly forbidden.