This is a supply driven market, which means it will peak when least expected and the move to the downside will be rapid.

By Richard Brock

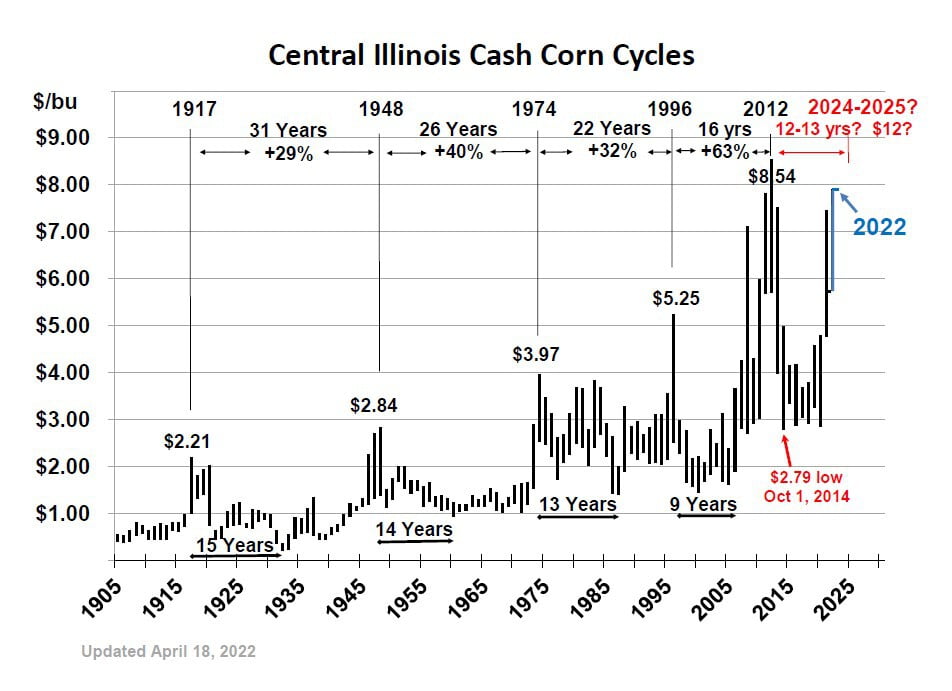

None of us have ever gone through a period of time like recent history. First the COVID-19 pandemic upended just about everything, and now the war in Ukraine is causing another global shock. As the world struggles to replace lost ag exports from Ukraine and Russia, U.S. weather conditions are off to a poor start for getting this year’s corn crop planted. The result is that we are seeing incredibly wild and high prices. For the last few years, we have published the long-term price cycle for corn, using Central Illinois cash prices as our benchmark. With the current strength in the corn market, we’ve received several calls and emails over recent weeks wanting to know if the cycle high might possibly be coming earlier than we previously thought. Maybe. Let’s review what the cash corn cycles really show. To begin with, there is a very dominant long-term cycle in cash corn prices. The first peak shown in the chart was in 1917 at $2.21 per bushel, with the next peak occurring 31 years later at $2.84. After that, the following peak was 26 years later in 1974 at $3.97, then 22 years after that at $5.25 and 16 years following that at $8.54 in 2012.

Source: Brock Associates

As the chart clearly indicates, the cycles keep getting shorter; from peak to peak and also from peak to trough. And each cycle peak is, on average, 41% higher than the previous peak. If the pattern continues, one could expect a new high 12 to 13 years following the 2012 peak which would put the next cycle peak at about 2024 or 2025 in the $12 per bushel area. With all of the current events, it is certainly a legitimate question to ask, “Is it possible to that the next cycle high will come ‘early’, as in 2022?” The most obvious two factors that might cause that to occur would be a continuation of the war in Ukraine which would then very likely result in a significant portion of their corn crop not getting planted. The normal planting season in Ukraine is similar to Minnesota, so there is still ample time left for their crop to be put in the ground. But as of now, the war seems is from being over and even if the crop gets planted, Russia is controlling the Black Sea and no corn can be exported out of Odessa. That poses a major problem. To offset that argument somewhat is the fact that because the port has been closed and exports are down sharply, this years’ corn ending stocks in Ukraine are going to be record high. A lot of that corn normally goes to Middle Eastern and Asian countries. With the tight corn supplies, other feed products are being substituted in livestock rations. Consequently, corn demand is actually being slowed in that area of the world. Of more immediate short-term concern is the weather in the U.S. Midwest. While corn planting progress as of April 17 was not materially behind, current field conditions are not favorable for a rapid advance in planting progress. Soil temperatures are very cold and even if the crop was in the ground, conditions are currently not conducive for rapid emergence. Thus, as of this writing it’s very possible that the Midwestern corn crop could end up being planted on average two weeks late, which is not necessarily a game changer. But if the crop is planted late, then the market would likely be even more fearful of the potential for a short crop. As in every bull market, bullish news keeps getting more bullish. The Bottom Line All bull markets need to be identified as either supply or demand driven. This one is supply driven which means it will peak when least expected and the move to the downside will be rapid. Because of this, our opinion is that $12 corn is not likely for this move. The news is almost always the most bullish at the top and combining planting weather in the U.S. along with the war in Ukraine, this is about as bullish as it can get. If the livestock industry and ethanol industry were both expanding and increasing demand, then the anticipated results would likely be different. But this is not a rapidly expanding demand market. Be very careful about getting too bullish this late in a bull market.