Will there be enough cage-free laying hens by 2026?

By the Egg Industry Center Many grocery retailers, restaurant chains and food manufacturers pledged to reach 100% cage-free egg purchases by 2026. These commitments require the conversion of living space for approximately 224 million U.S. laying hens. The question is, can it be done in time?

While the question seems to be simple enough, Maro Ibarburu, Business Analyst for the Egg Industry Center, outlined challenges facing the industry’s transition status at the Midwest Poultry Federation Convention.

Unknown challenges Ibarburu highlighted two major unknowns that make it hard to estimate the industry’s cage-free conversion status.

The first issue is that to date nine states have legislated cage-free egg production. This has created a cage-free demand “overlap” with the cage-free purchasing pledges that were already in place. Ibarburu explained that each state enacting legislation had organizations that were already committed to 100% cage-free egg purchases. Therefore, this creates a potential double-counted demand for cage-free eggs. The overlap makes it difficult to calculate the status of the transition by merely looking at the size of the U.S. laying flock in cage-free systems. Ibarburu estimates a difference of 48 million laying hens needed to supply the state legislation and customer pledges based on different overlapping assumptions.

The second unknown is the volume of cage-free eggs needed by organizations that did not commit to 100% cage-free egg purchases. Many retail outlets were already selling cage-free eggs before the cage-free pledge movement or adoption of state legislation. Many of those organizations plan to continue providing consumers cage-free egg choices, even if they are not committing to 100% cage-free. This stream of cage-free eggs that are needed, but not part of the pledges, also makes it hard to calculate transition status.

Known challenges There are also known challenges making the industry’s transition to cage-free egg production difficult. Available capital continues to be a concern. Given the number of cage-free laying hens placed as of January 2022, the industry needs an additional estimated $6.6 billion to finalize the conversion. Typically, for an investment to make economic sense, it would result in either reducing the cost of operation or securing a product premium. The Coalition for a Sustainable Egg Supply study showed that the cage-free operating cost are higher. Therefore, the only alternative is a price premium, which finally depends on consumers’ willingness to pay. So far, consumers overwhelmingly prefer to buy the less expensive conventionally produced eggs.

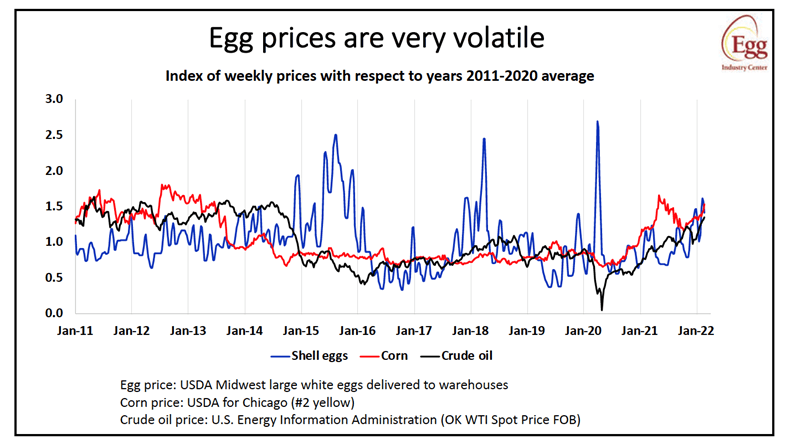

Add to the capital outlay the volatility of the egg market. The relative price volatility of eggs was apparent when Ibarburu illustrated this volatility by graphing the warehouse price for eggs against corn and crude oil markets (Figure 1). This volatility makes it hard for egg farmers to create repayment plans with their lenders. Ibarburu explained that there may be prolonged periods when farmers are unable to make payments, and then other times when farmers can pay more than a normal payment.

Additionally, the higher capital costs needed to enter the cage-free egg market creates a barrier to enter the market for new farmers. Oddly enough, there is also a barrier to exiting the market once a farmer has made the cage-free investment because they have a more expensive facility, which makes it hard to compete with the more affordable conventionally produced eggs.

Ibarburu estimates a difference of 48 million laying hens needed to supply the state legislation and customer pledges based on different overlapping assumptions.

Finally, when looking across the entire country, 2021 retailer purchase data from Nielsen reveals that for certain regions of the country, consumers are rapidly converting to cage-free egg purchases, but not in others. The Northeast and Northwest regions show non-conventional purchases add up to 29-31% of total egg sales. In contrast, the South and Midwest show 11-13% non-conventional purchases. This will be an interesting trend to watch as legislation and pledge deadlines approach.

The future In looking at the current consumer purchasing habits and the cage-free egg markets, there are lessons to be learned regarding the new cage-free egg market of the future. USDA reports that in the last five years the average retail price difference between conventional and cage-free eggs has been $0.83/dozen.

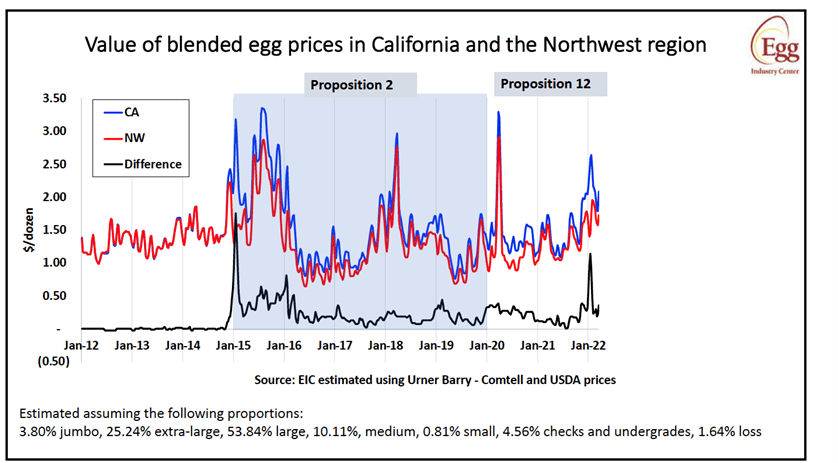

The Egg Industry Center has been paying specific attention to California, as it is the only U.S. market currently fully cage-free. For years California mirrored the northwest states of Washington and Oregon with its prices. After the inception of Proposition 2 that required 73% more space per bird than the industry standard and the cage-free egg sales mandate required by Proposition 12 legislation, California markets initially spiked but then leveled out, although at a higher price than the northwest states (Figure 2). This indicates that we can expect to see an increase in overall prices in a transition to cage-free production, but the amount of that increase is hard to estimate now and will likely continue to change as more cage-free state legislation and retail pledges come online.

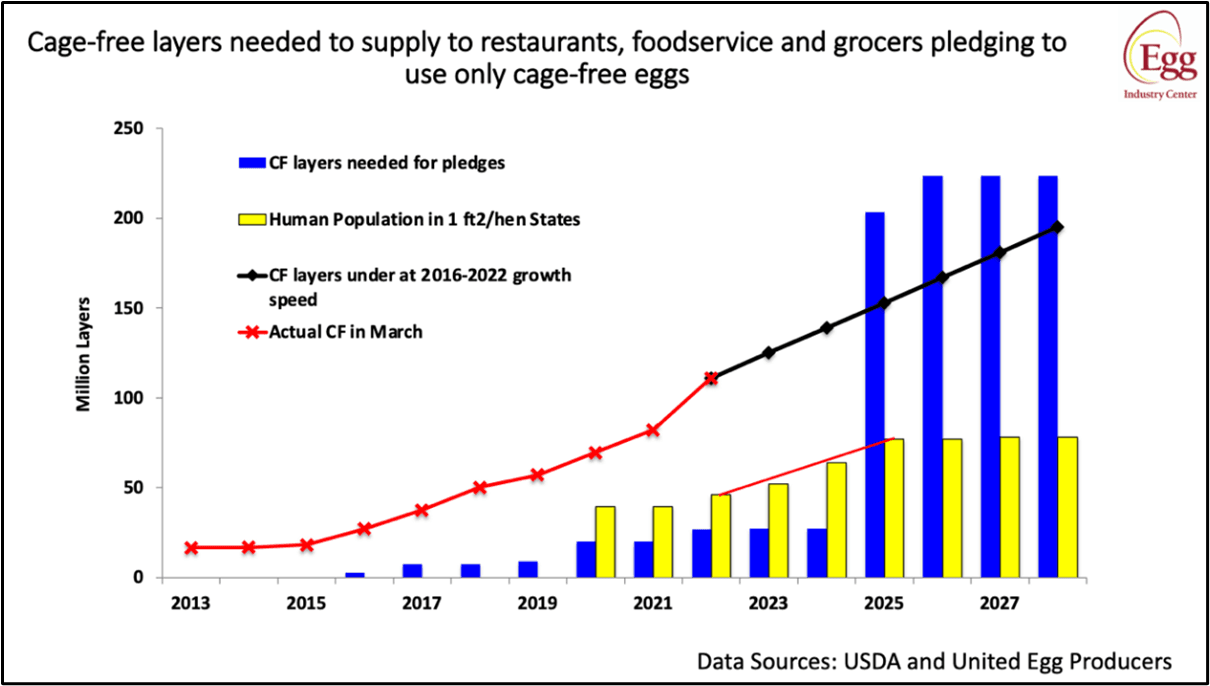

Understanding all the challenges still leaves one over-arching question: Will there be enough cage-free laying hens by 2026? As of March 2022, the industry already has enough cage-free laying hens to meet the needs of all nine states that have committed to regulating cage-free housing. If the industry continues to convert at its current speed, the flock will reach 168 million cage-free layers by 2026, roughly 75% of purchase commitments and nearly 50% of the current U.S. flock (Figure 3). What will be the overall effect of the overlaps in pledges and legislation? Only time will tell.