The number of commercial turbofan and turboprop engines in service globally is forecast to increase by 35%, from 66,333 in 2023 to 89,549 by 2032.

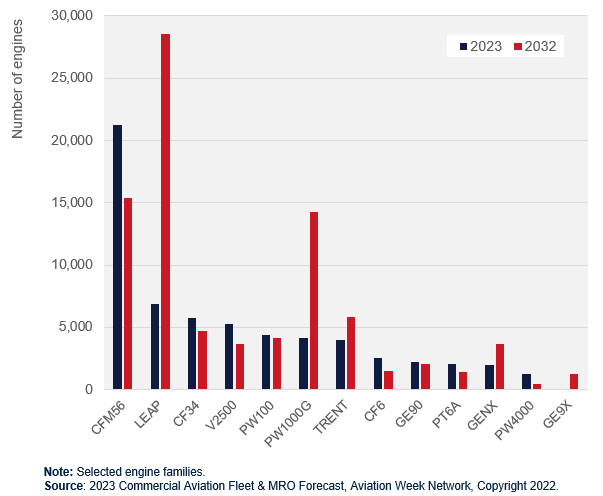

At present, the in-service fleet of engines is dominated by the CFM56 family. As of 2023 a total of 20,662 of these engines are in service worldwide, representing almost a third of engines in service on commercial aircraft. While the number of these engines in service will gradually decline through the forecast period as narrowbody fleets transition to aircraft with new generation engines, 5,000 of CFM56s will remain in service in 2032, accounting for 17% of the in-service fleet at that time.

The main beneficiary of the gradual withdrawal of the CFM56 is expected to be the LEAP family of engines. The in-service number of the LEAP is projected to increase by more than 300% over the forecast period, from 6,876 engines in 2023 to 28,538 in 2032. The PW1000G will similarly see numbers of in-service engines increase by 237%, the GENX by 84% and the TRENT family by 47%.

While mature engines such as the CFM56, CF34 and V2500 will continue to account for the majority of the in-service fleet of engines throughout the 2020s, new generation engines will progressively increase their market share over the period. Between 2023 and 2032, new generation engines such as the LEAP and PW1000G combined will increase from 16% of the in-service engine fleet to 47% as commercial aircraft fleets are gradually recapitalized.

Simultaneously in-service numbers of RB211 engines are expected to fall by 83%, CF6-80s by 42%, V2500s by 30%, CFM56s by 27% and CF34s by 18% over the forecast period.