Brian Kough, Senior Director, Forecasts & Aerospace Insights, Intelligence & Data Services

The commercial aviation market finally turned a corner. The segment is seeing a flurry of activity along with turbulence adjusting to the new normal. The uneven regional recovery saw the North American domestic market recover the quickest followed by much of Europe, most recently redoubling their schedules, and Asia-Pacific now accelerating to keep pace with demand with strong ASKs scheduled.

These recent experiences of pent-up air travel demand underscore the optimistic forecast for the commercial transport aircraft segment. Continued improvements are still to come as several regions experience passenger demand improvements while others are practically recovered. Nearly 21,800 new commercial aircraft are anticipated with more than 10,800 aircraft retiring during the 10-year forecast period. At risk are knock on effects from labor shortages, nagging supply chain issues, and MRO aftermarket performance as well as underlying positive economic conditions continuing to support our industry.

Examples of regional, utilization rates quickly recovering, as well as business aviation utilization rates peaking above historic means, demonstrates the undercurrent ready to fuel the next phase. With twin-aisle aircraft market demand likely stunted for some time, narrowbodies lead the recovery. Boeing’s recent manufacturing troubles however sets the stage for Airbus to maintain a dominant market share in the all-important narrowbody segment for the foreseeable future. Boeing’s legacy and new generation aircraft MRO aftermarket requirements on the other hand will surpass all others at $500 billion out of a total +$1 trillion 10-year market.

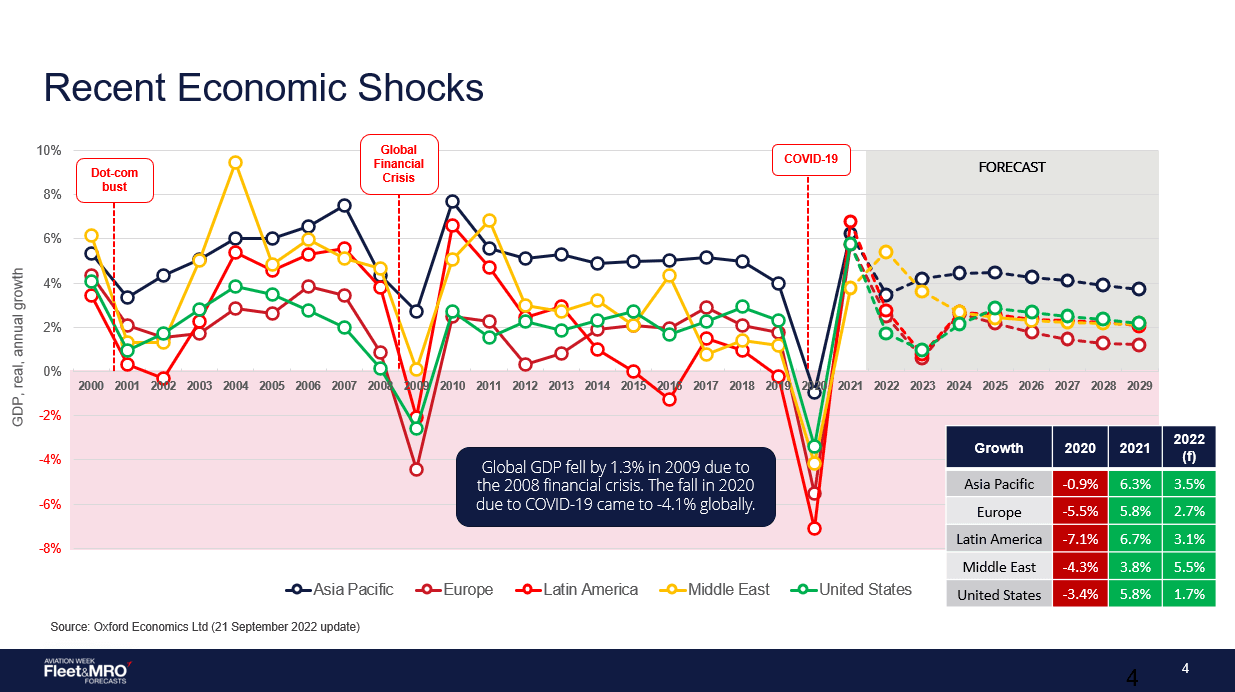

Concerning factors increase this year, however. Long-term aircraft retirement expectations could signal trouble for legacy engine parts suppliers as green time and USM materials likely flood the engine market in the second half of the decade. Low interest rates seem to be a thing of the past and fuel prices have been vulnerable to shocks as the world’s supply chain sorts itself out. Recent aggressive GDP recovery predictions around the world seem unachievable at the time of this report. The needs and wants of commercial passengers though cannot be mistaken.