Market Outlook

Herd liquidation is coming and so are higher feeder cattle prices With high input costs does this mean more profit for producers?

By Elliott Dennis

There is little doubt that the beef cow herd will be smaller in 2023 and 2024 compared to 2022. Liquidation of the beef cow herd consists of two parts: decreasing the number of beef cows and heifers that will eventually be bred.

The accelerated beef cow slaughter implies a lower calf crop in 2023. This could be offset by more bred heifers but the large percentage of cattle that are on feed that are heifers indicate that cow-calf producers are not seeking to re-build herds – at least not yet. This translates to fewer feeder cattle in 2024.

Combined, fewer feeder cattle available for feedlots, assuming a stable domestic and export beef demand environment, leads to higher prices for cow-calf producers. But higher prices do not necessarily mean that producers are making more profit. Higher feed and other cow costs are limiting profits.

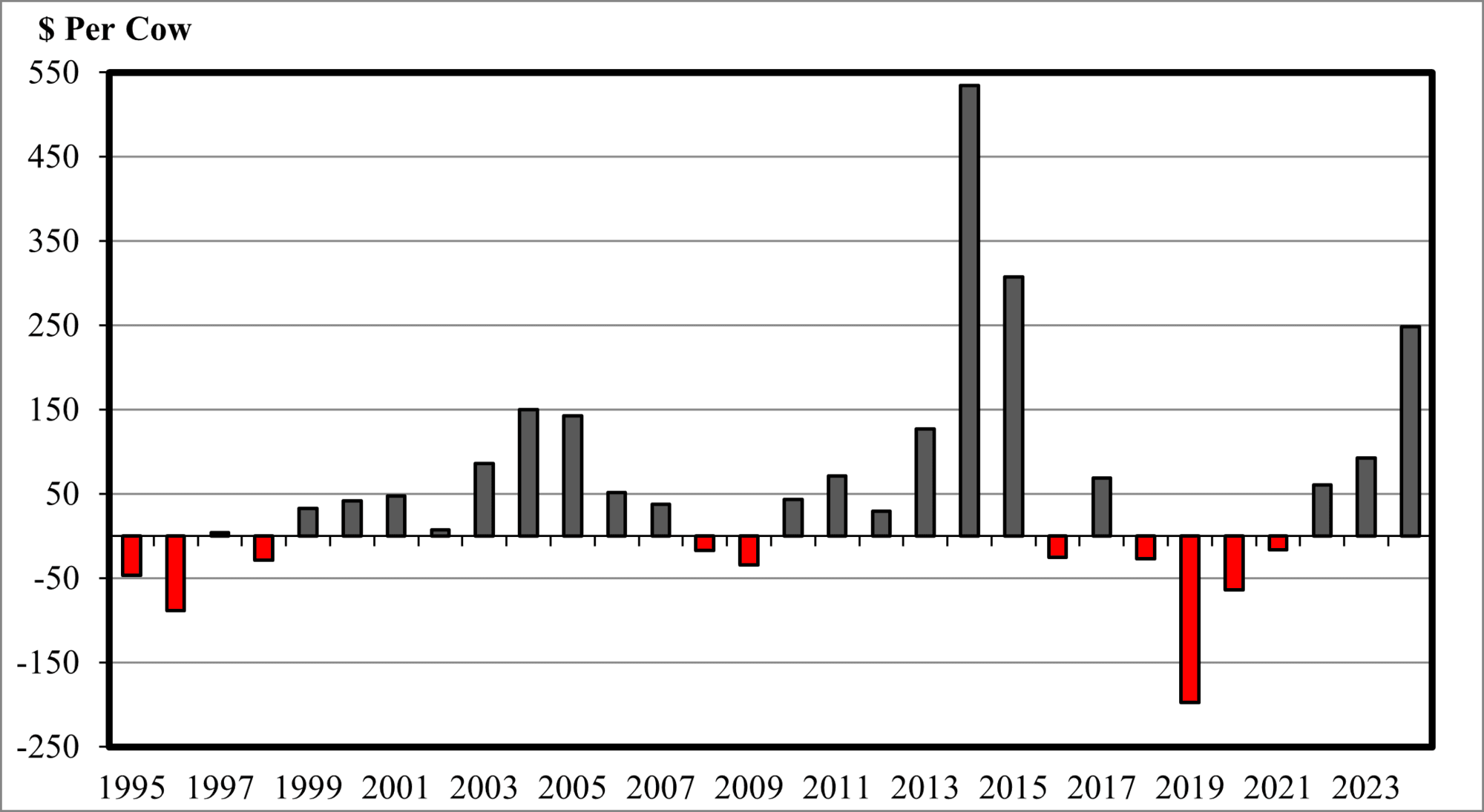

Estimates are that cow-calf producers will net approximately $60 per cow in 2022, $93 per cow in 2023 and $248 per cow in 2024 – the largest profit margin since 2014 (see Figure 1). In what follows, I explain the details of how I came to these conclusions and what indicators producer should for if the US beef industry is beginning to rebuild the herd and how this will ultimately affect prices received for cattle.

Figure 1. Estimated average cow calf returns over cash cost, annual. Note: Includes pasture rent. Source: LMIC (2022).

Heifers on feed The number of heifers on feed is an early indicator of the feeder cattle supplies in one to two years. As the number of heifers on feed increases, there are fewer heifers to be bred and thus a lower calf crop in future years. USDA-NASS releases the number of heifers and steers on feed each quarter in addition to the monthly cattle on feed report for approximately 13 states.

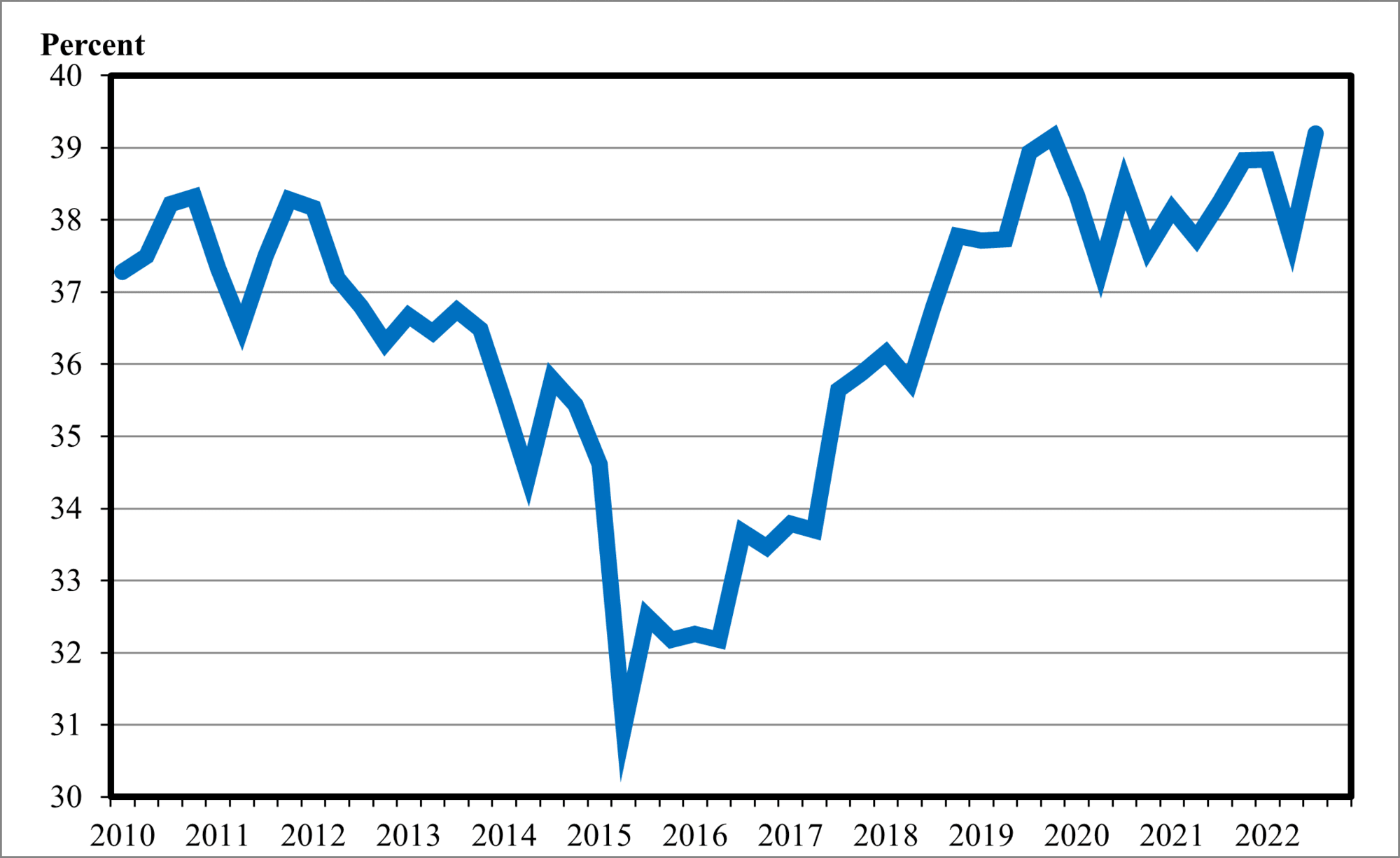

Heifer placements into feedlots, as a percentage of total cattle on feed, have been increasing (see Figure 2). Currently, approximately 40% of all cattle on feed are heifers. During periods of contraction, heifer placement into feedlots is high and during periods of herd rebuilding, it is low. The fewest number of heifers on feed occurred in 2016 at the peak of the last cattle cycle at approximately 32%.

Figure 2. Heifers on feed as a percent of total cattle on feed in the U.S. Note: Beginning of quarter. Source: USDA-AMS (2022), LMIC (2022).

As prices begin to rebound in 2023, look for more heifers to be retained which will increase the calf crop in 2024. This adjustment tends to happen rapidly. Usually, within about 18 months of the turn of the trend, we have retained enough heifers to rebuild the herd. Output price risk management is essential if producers are going to be selling as prices can erode quickly after retention has occurred.

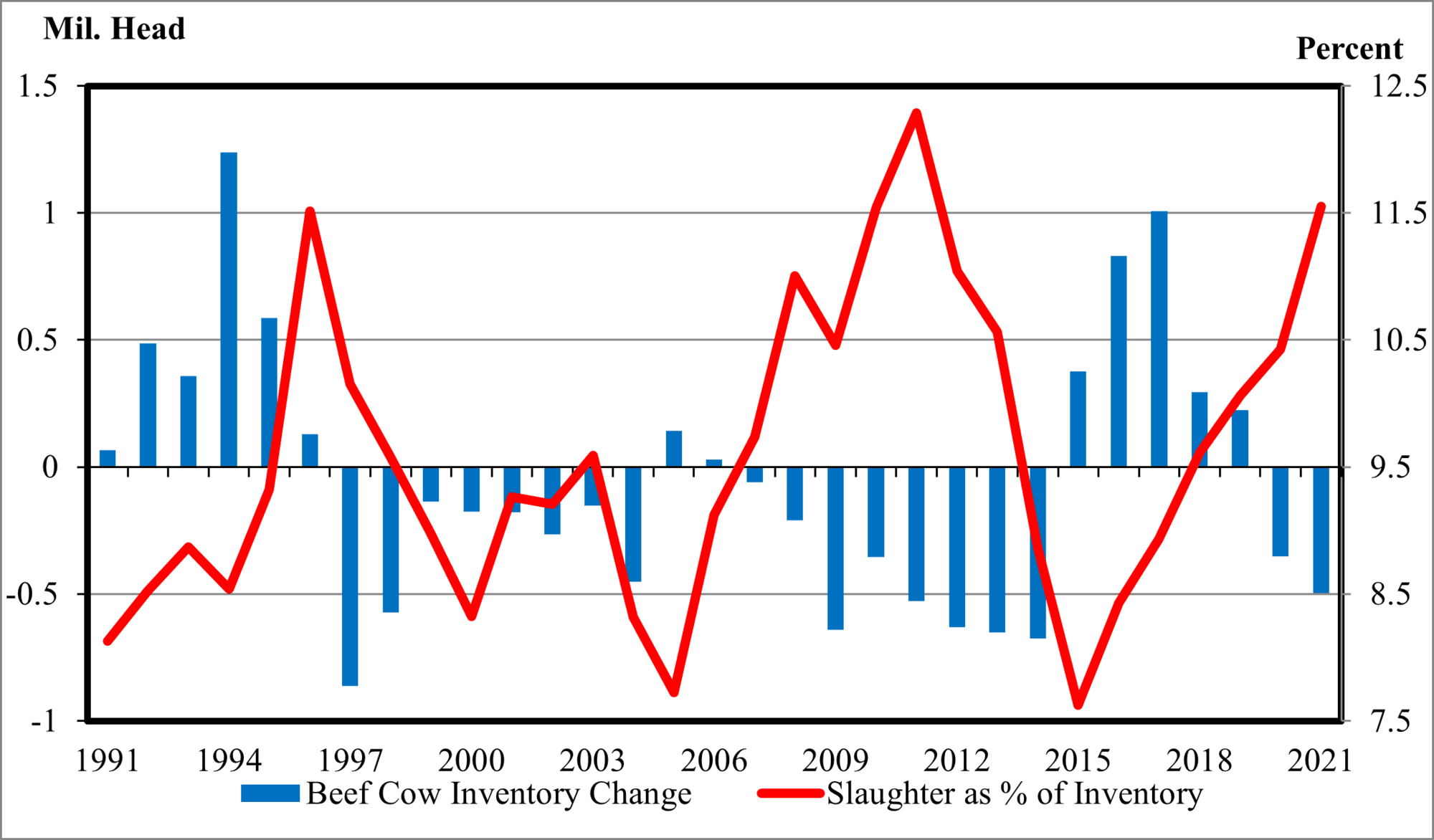

Beef cow sell-off Beef cow supplies are the most immediate indicator of a smaller calf crop within the next year. In 2022, there has been a strong pace of cow slaughter. Current beef cow slaughter is at 2.6 million head year to date. In 2021, the U.S. harvested about 3.5 million head.

Beef cow slaughter is very flexible, it can change very quickly given market conditions as the decision is very simple and readily available – cows are ready and can be sold off in any given week (see Figure 3). Abnormally high cull cow prices due to low ground beef imports and worsening drought conditions have incentivized more cows to be sold off.

Figure 3. Beef cow inventory change & federally inspected beef cow slaughter in the U.S., annual. Note: Federally inspected slaughter is on a percent of total cow inventory. Source: USDA-AMS (2022), LMIC (2022).

A lot of cows are being pulled forward to slaughter quicker than they historically have been, as evidenced by the dramatically lower cow dressed weights. Cow dressed weights in May are historically 645 pounds but in 2022 cow dressed weights were about 630 pounds. The deviation in weights began in May 2022 and have anywhere from 5-15 pounds less than the historical five-year average since then.

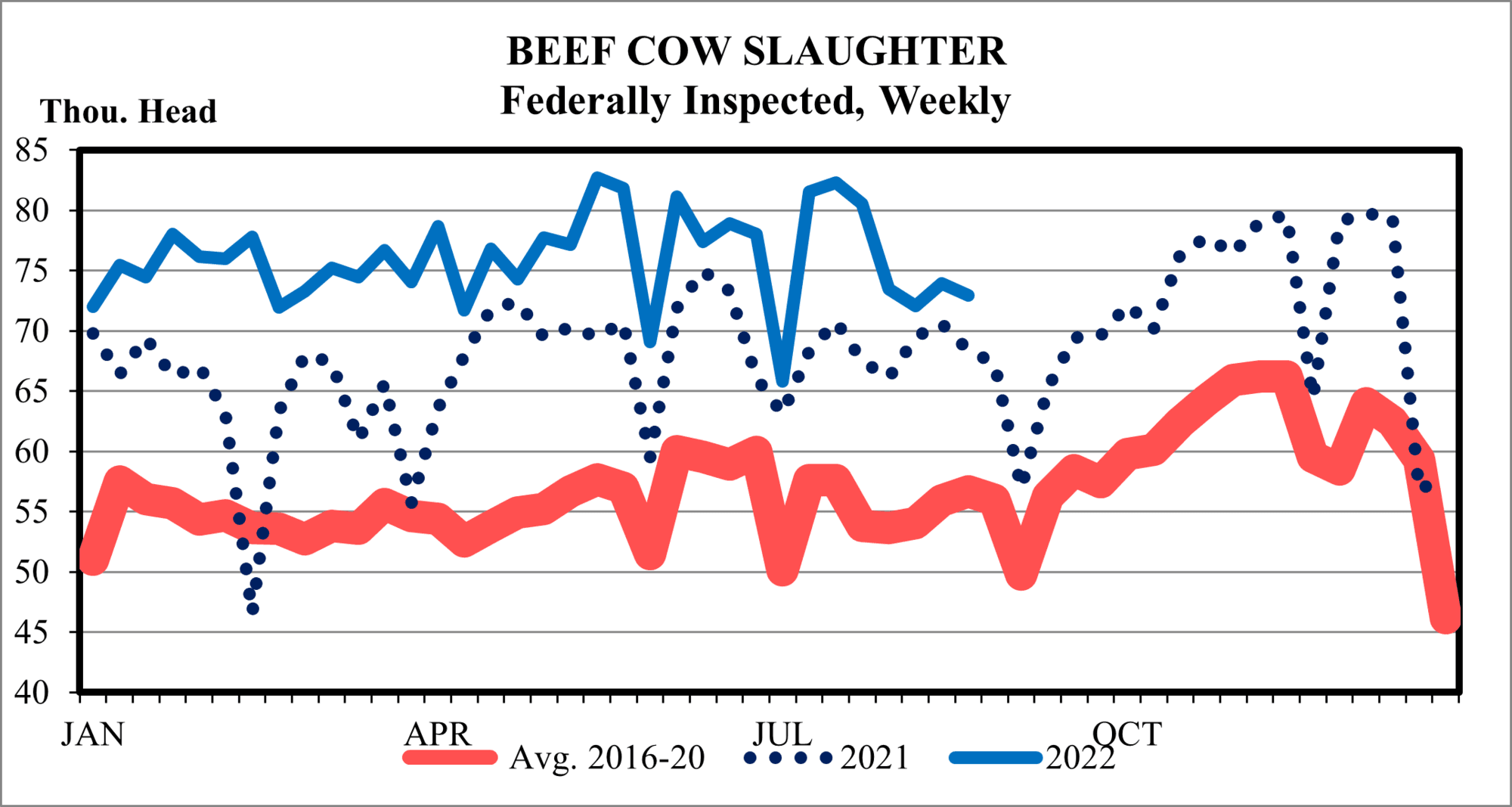

For the United States to break even with last year’s annual cow slaughter numbers it would need to reduce the total weekly harvest to about 50,000 head per week nationally. That would be a significant deviation from the historical averages of beef cow slaughter during the fourth quarter.

On average, the United States harvests about 67,000 head per week during those months and it has only had a few months where it has been under 55,000 head nationally (see Figure 4). So the beef cow herd is going to contract, the question is by how much? My estimates using historical data suggest that the beef cow herd will likely be reduced by 4-4.5%. This is slightly higher than the July cattle inventory report which estimates a reduction of about 3-3.5%.

Figure 4. Beef cow slaughter, weekly. Note: Only from Federally Inspected plants. Source: USDA-AMS (2022), LMIC (2022).

The justification for a slightly higher percentage decrease is that hay production is down significantly and unless there are a few good rains to allow recharge in the pastures then winter grazing could be limited.

Add to that reduced corn stalks biomass due to lower corn yields and we will likely be in a situation where feed resources are very thin and producers will sell some cows off rather than buy higher feed prices.

In other words, I believe the market will continue at an elevated slaughter pace into the 4th quarter of 2022.

Regional retention and liquidation All the commentary thus far has focused on national numbers but there are always regional differences. These differences in production decisions ultimately translate to differences in prices received for cattle.

So are there differences in the percentage of heifers on feed in each of the five major cattle feeding areas? The short answer is yes.

Iowa/Minnesota has a significantly lower number of heifers on feed relative to Kansas and Colorado – 22% vs 48%. Nebraska and the Texas-Oklahoma-New Mexico region are fairly similar with about 41% of cattle on feed that are heifers.

This translates to slaughter weights and quality grades coming out of these regions – heifers tend to grade slightly lower and are brought to lower dressed weights. Thus, regions with a higher number of heifers on feed are likely to see lower quality grades and slightly lower beef production.

Are there differences in the number of beef cows being sold off by region? Definitively yes. USDA does not report beef cow slaughter by state but by region.

The most significant change has been the decrease in slaughter from Region 5 and the significant increase in slaughter from Region 6 (AR, LA, NM, OK, and TX). The steady rise in beef cow slaughter in Region 6 is a direct result of the drought. Over the last two months, they have been averaging about 2,000 more head per week than in the earlier part of the year and well above last year's slaughter.

Higher cow slaughter indicates that fewer feeder cattle will be available in 2023 and these regions could see slightly higher prices relative to other regions assuming other factors are similar across regions.

Elliott is an assistant professor in livestock marketing in the Department of Agricultural Economics at the University of Nebraska-Lincoln.