Market Outlook

And the cattle show keeps on rockingBy Elliott Dennis

As we head into the fourth quarter of 2025 markets have continued to show out in some remarkable ways. Consider just a few of these that have happened over the past 9 months:

U.S. beef demand reached record highs in Q2-2025 (up 34% from 2000) with consumers sustaining strong purchases even at higher prices.

The Choice cutout has stayed elevated longer than usual as packers found new value in chuck and round primals amid tight cull cow supplies.

Tariff friction with China reduced beef exports, but export market diversification has limited some of these effects

Heavy carcass weights persist as cheap corn and low grid discounts make feeding cattle longer more profitable than marketing lighter animals.

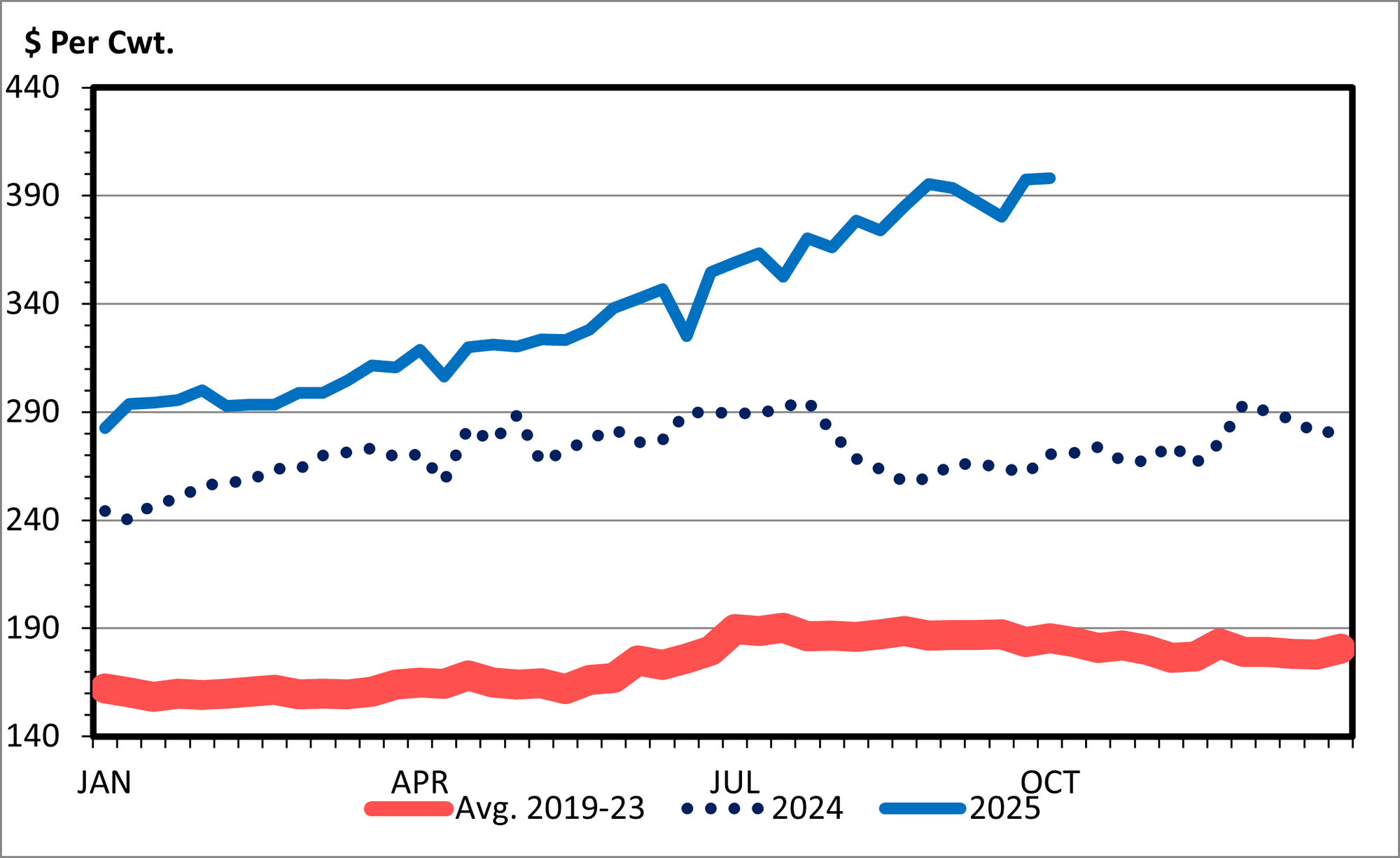

Feeder prices have hit record highs across weights while heifer retention remains limited despite strong fundamentals and high cull cow values.

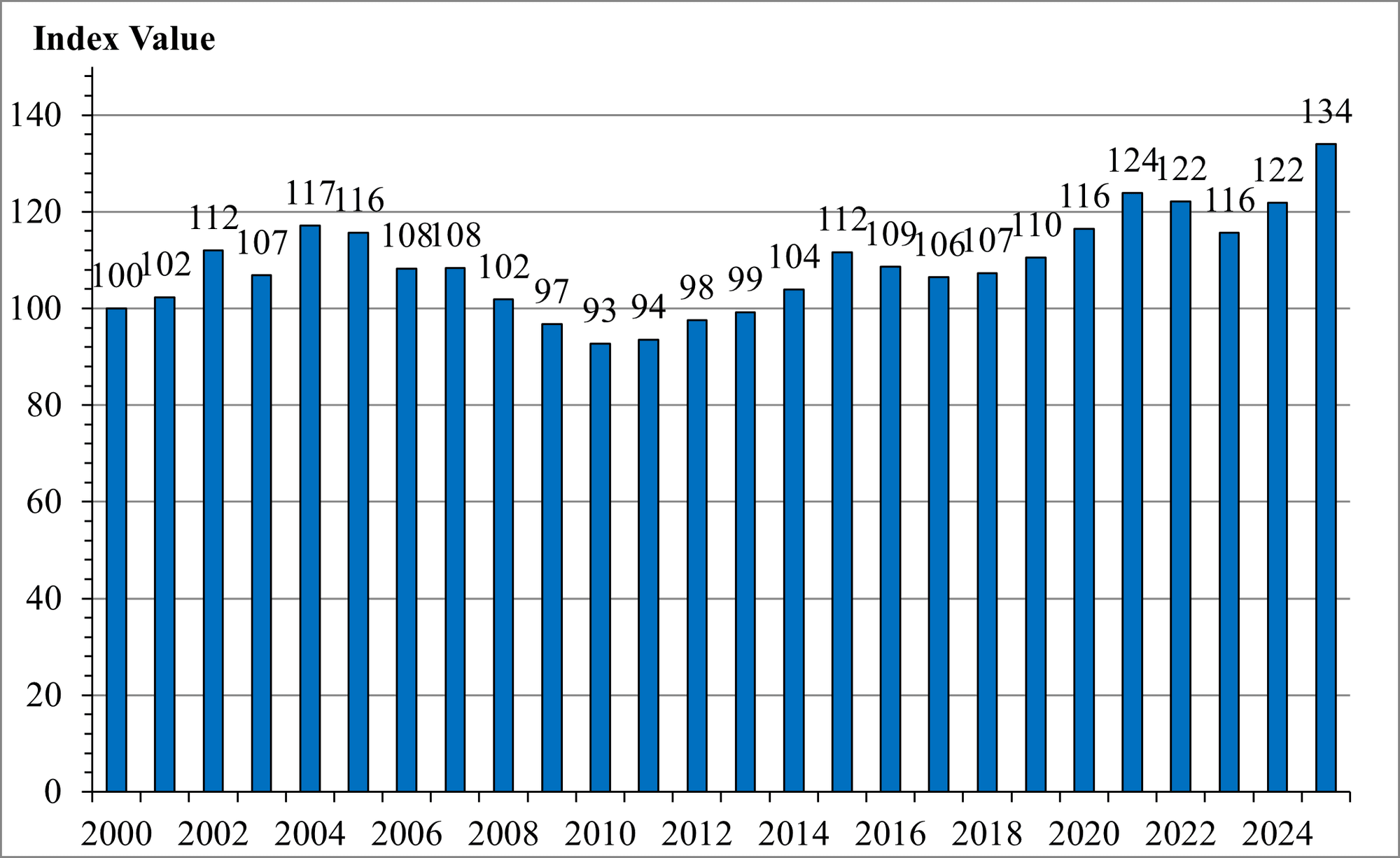

Consumer demandBeef demand is a function of the quantity consumers are willing to purchase at given prices. Whether the beef demand increases or decreases is a function of both these factors. Economists can put demand into an index that compares current demand levels to a historical base year, generally the year 2000. In all quarters this year beef demand has been at record highs.

For example, in Q2 beef demand was 134 meaning that beef demand was 34% higher in 2025 than in 2000. Comparing this high over other years and Q2-2025 was the highest demand ever recorded by nearly 10%. This has largely been a function of constant consumption but at higher prices. This change has some questioning whether we are entering a new phase of U.S. consumer demand where own prices matter more than cross competing commodity prices such as those for pork and chicken. Consumers have been the shining star thus far in 2025.

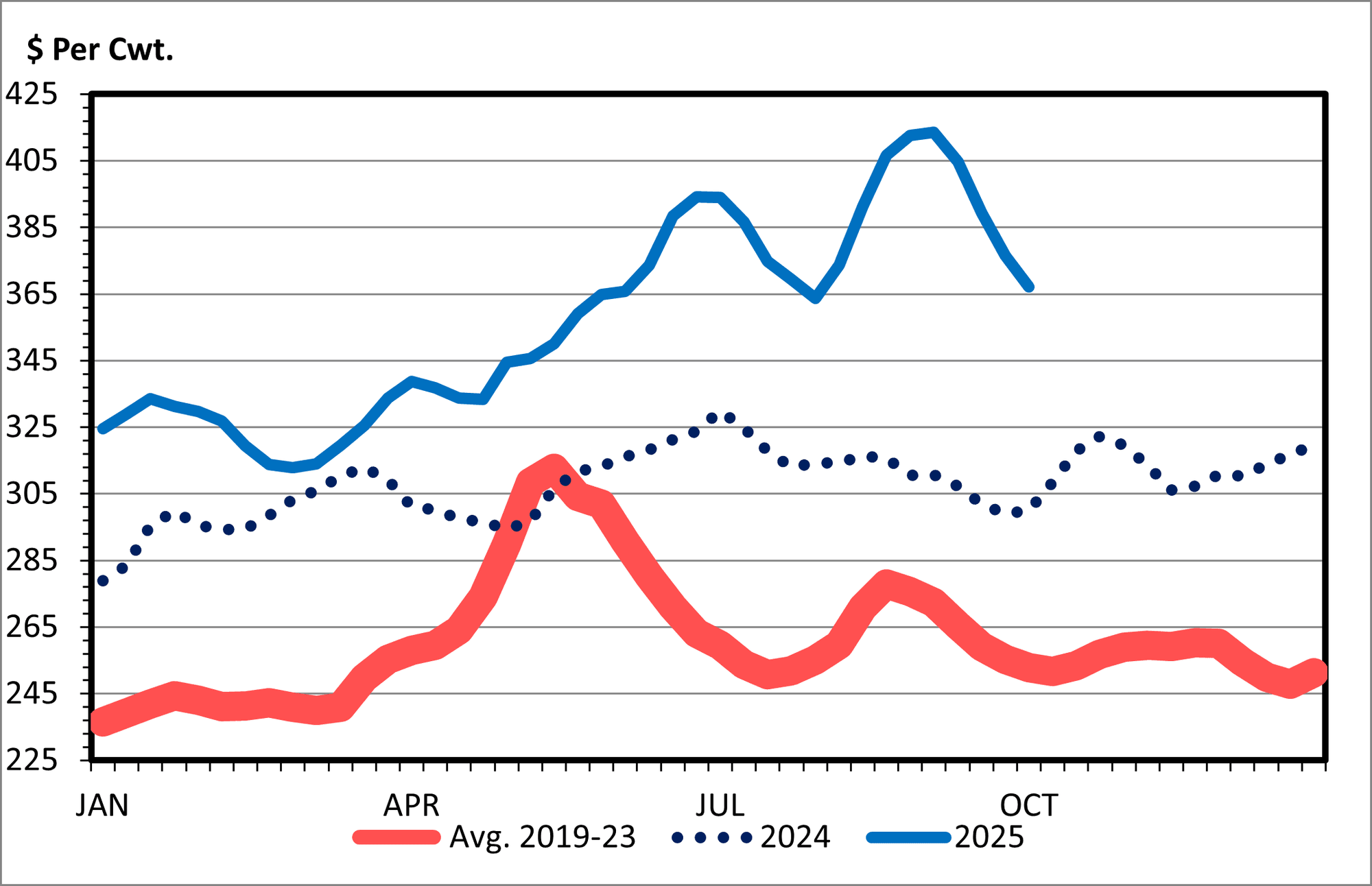

Beef cutout and cull cowsThe Choice Beef cutout remained strong during the summer months which normally is carried by the rib and loin but was supported by strong prices for round and chuck primals. This caused the cutout to remain at higher prices for longer beyond the seasonal peaks. Higher values for the chuck and round came partially from their higher value in the form of grind rather than roasts. Some of these meat primals have been ground and then mixed with 50’s from the fed cattle kill to get 80/20 or 90/10 ground beef.

Consumers continue to love ground beef and the shortage of cull cows to get 90s has put pressure on packers to find more profitable means for the chuck and round. As long as cull cow prices remain high, which I anticipate will occur to some degree in Q4, the cutout will continue to stay elevated. This combined with drop credit for byproducts for tallow, hides, and offal meats has supported packers.

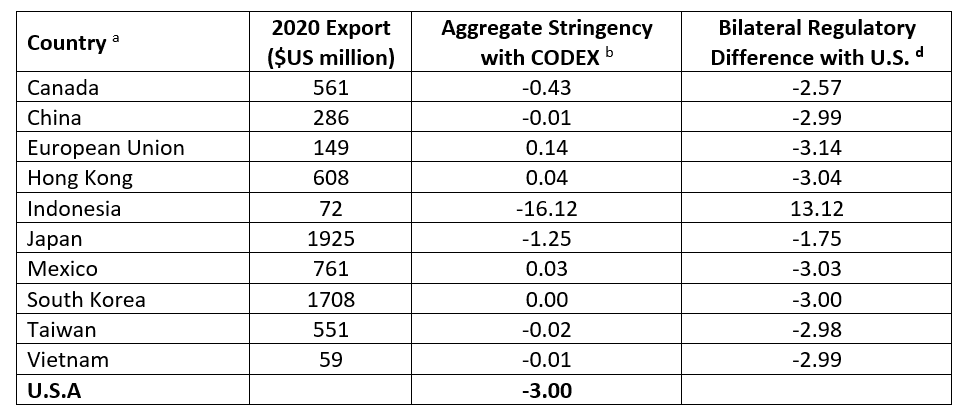

International tradeTrade flows are shaped in part by tariffs and non-tariff barriers as many countries protect their agricultural sectors to maintain food security and rural employment. Under the Trump administration in 2025 tariffs have played an important role in the beef trade. Current volumes of beef exports to China are now back to pre-Phase 1 and Phase 2 levels, shifting China from a major buyer to a minor market. Fortunately, new export markets continue to emerge supported by the beef checkoff program.

Non-tariff measures such as sanitary and phytosanitary regulations (SPS) are also a key figure in the Trump trade negotiations. The United States maintains some of the most lenient import standards among major trading nations, forcing domestic producers to meet stricter health requirements abroad than foreign suppliers face when exporting here. These issues will remain central to the ongoing trade negotiations.

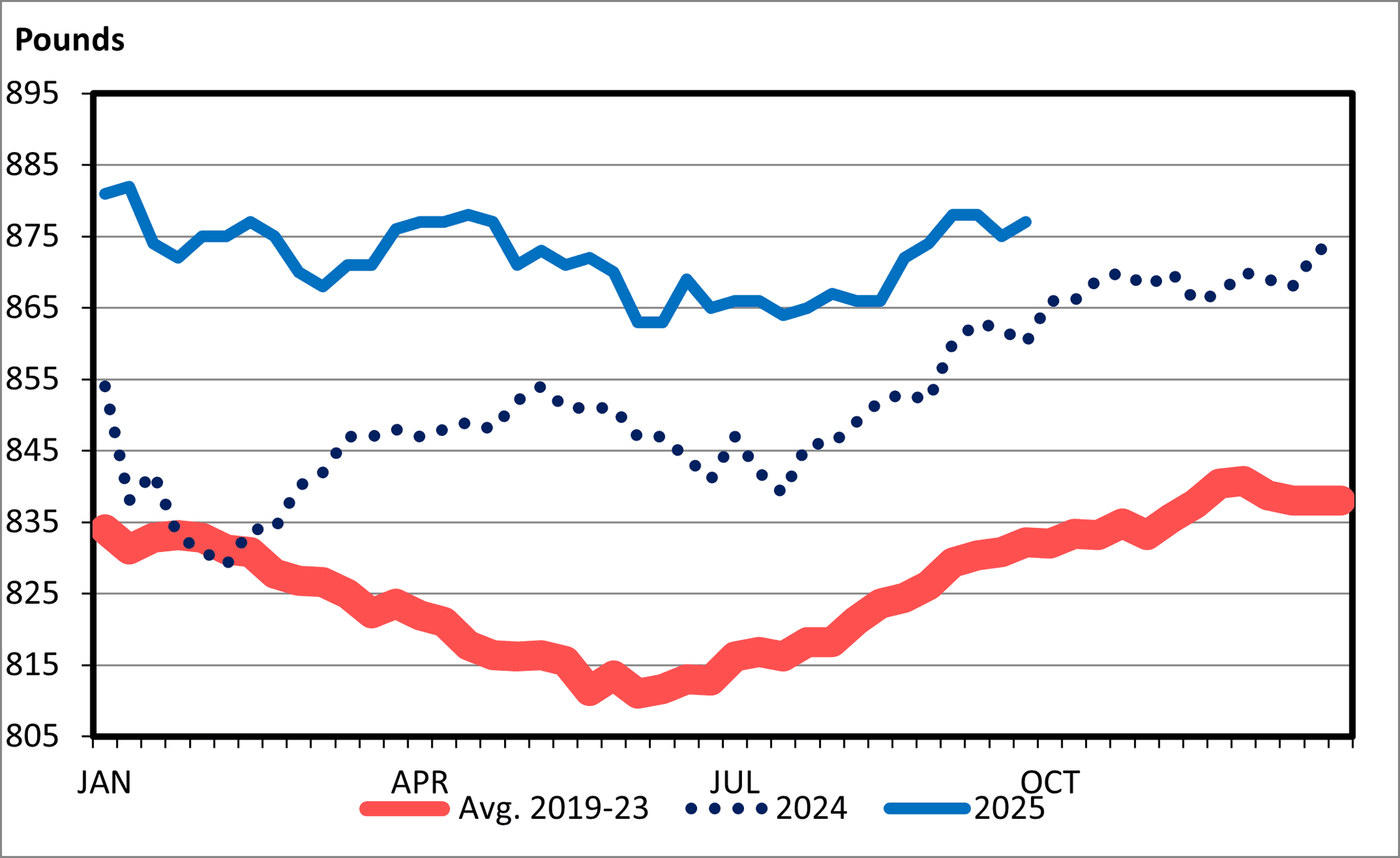

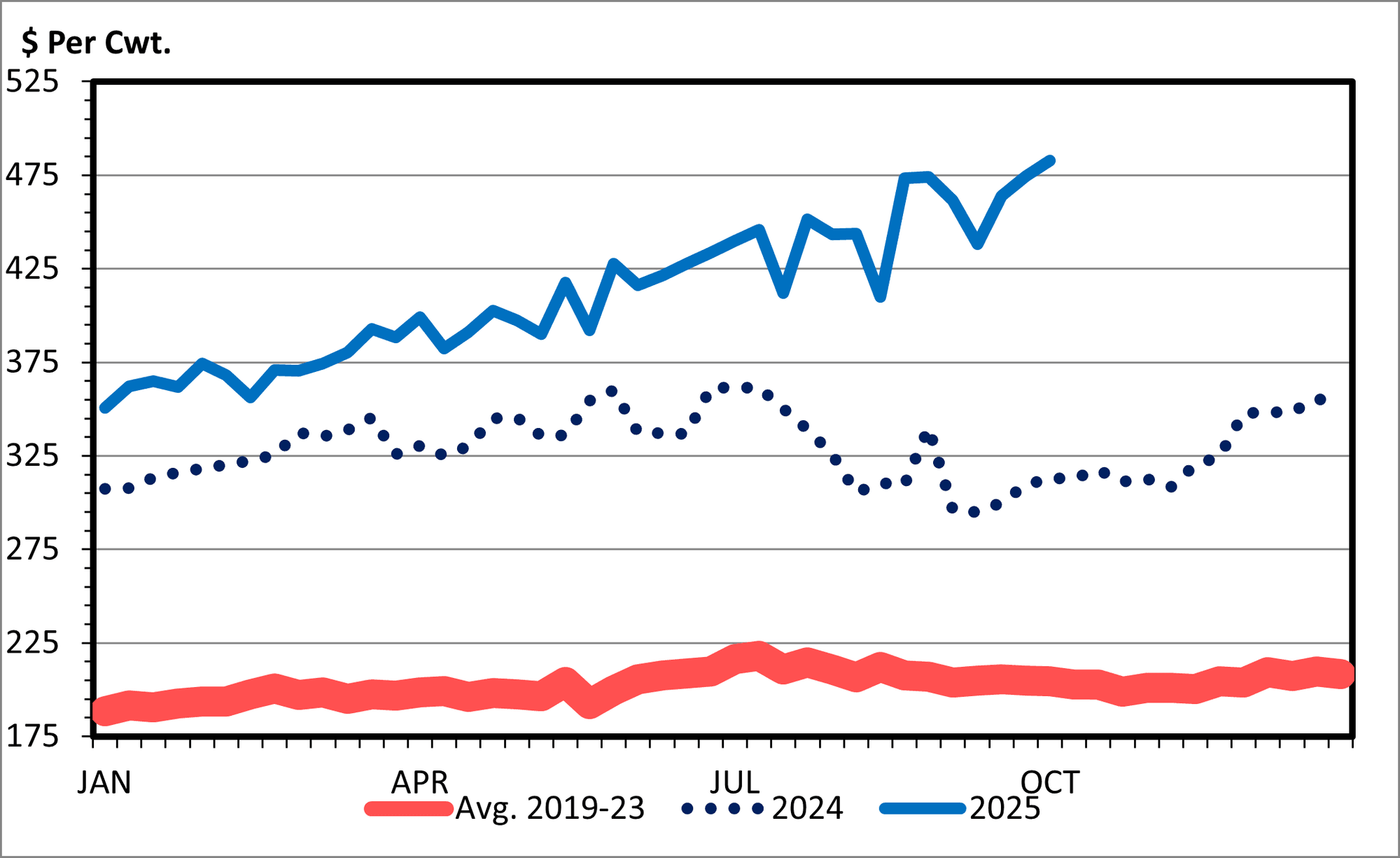

Fed cattleCarcass weights have continued to be elevated driven by low corn prices, higher feeder cattle prices, and low discounts for heavy carcasses. All these indicate that feedlot profits are maximized by putting on additional pounds on an existing carcass rather than putting the weight on a new animal. Higher days on feed leads to more cattle grading Choice+ but at lower yield grades (4s and 5s) and thus more residual fat to be utilized.

Low discounts on heavy carcasses by packers has allowed this continue with packers willing to harvest fewer cattle at higher weights which has caused total beef production to remain similar to 2024 YTD. Cattle weighing 900-1000 lbs., 1000-1050 lbs., and over 1050 lbs. are currently being discounted approximately $1 , $4, and $15 per cwt, respectively. These discounts have remained constant within the last 4 years. For carcass weights to change, grid discounts would need to increase, and corn would have to remain cheap as feeder cattle prices will certainly be higher into the future.

Feeder cattleFeeder cattle prices have kept the ball rolling this year. Over the past few months, sale barns have been posting record level prices for feeder cattle across all weights. The value of gain for cattle in Nebraska and most states in the Northern Plains indicates that lighter cattle are the premium product with no huge incentives to put on additional weight. Spurring this has been the reality of a strong cull cow harvest which many analysts thought would have cooled by now.

But strong consumer demand and with many producers fearful of the sharp drop experienced in 2014/15, many have seemingly chosen to get the cash up front and let the market ride out. Private treaty cattle, which tend to be program cattle, have been at even higher prices.

Even so, heifer retention appears to still be lagging. Heifer retention first shows up through a reduction in the share of auction barn receipts for heifers both over and under 600 lbs. Regionally some markets have started to slip but nationally it will take through the end of November to see the full picture before heading into the USDA January Cattle Inventory Report.

Takeaways2025 has certainly been an unexpected year in terms of the price highs and for how long they have persisted. Everyone is keeping their pulse on heifer retention observed first through auction barn receipts, then through quarterly cattle on feed, and final through head slaughtered. Heifer retention has been complicated by higher cow harvest from record level cull cow values.

Finally, prices along the supply chain are continuing to be supported by record level consumer demand for beef products. If consumer demand falters we could see prices self-adjust downward quickly.

Dennis is an associate professor and livestock and marketing economist with the University of Nebraska – Lincoln.