Market Outlook

Summer showdown awaits cattle marketBy Domenic Varricchio

The 2025 Annual Meat Conference recently concluded in Orlando, Florida, and at the conference, one of the topics discussed was consumer beef demand. A poll was conducted on 1,600 consumers and it showed that grinding meat is where the beef demand growth happened in 2024. According to Circana data, ground beef was the No. 1 food category of the year, among 85,000 other foods!

In terms of dollar growth, ground beef was No. 1 with 2024 sales up 9.6% to $15.3 billion. Unit sales of ground beef were up 6.8% to 1.6 billion.

What’s more is the demographics of who is buying ground beef. Millennials now account for 28.6% of all ground beef sales and were responsible for 42% of 2024’s growth. The survey showed that millennials love ground beef so much, they’d prefer a dedicated section in the grocery store for ground beef as opposed to positioning it next to the muscle cuts. That’s remarkable to me.

Millennial spending on ground beef accounted for 62% of total unit sales growth in 2024 and 52% of the dollar sales growth. Anne-Marie Roerink conducted the survey and says that this is a sign of the “changing of the guard.” Millennials are taking the place of the baby boomer generation at the meat counter. For this writer, I think this is a sign that ground beef demand should continue to grow in 2025.

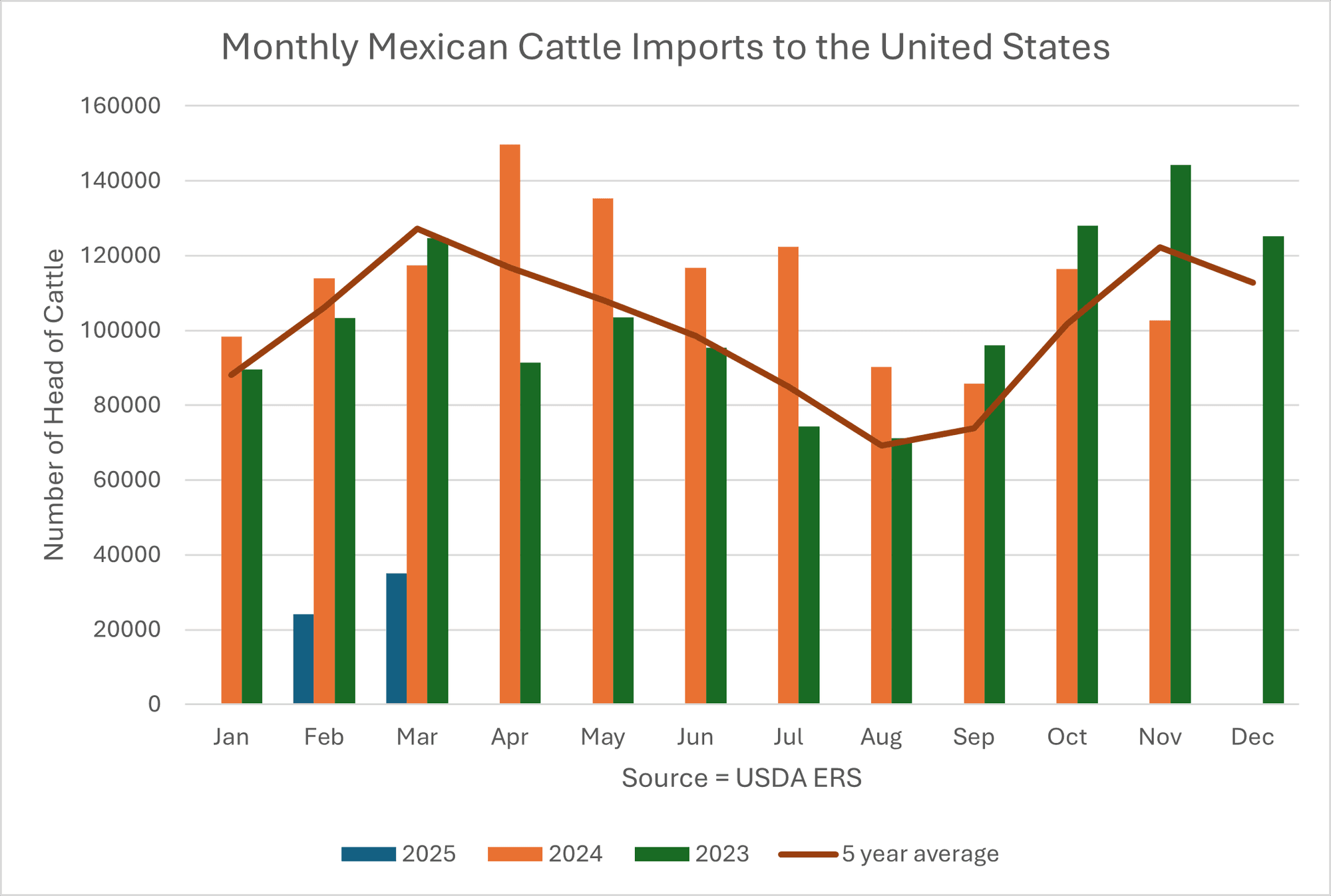

That’s the big question for the cattle market heading into summer. Will there be enough cattle to meet demand in the May, June and early July timeframe? The border closure from Nov. 25 through early February set us back on feeder cattle inventories that normally are placed against the June timeframe. Mexican cattle imports typically peak in March and help provide extra cattle numbers for the summer beef demand period. Through March 14, cumulative total cattle imports from Mexico are at 59,135 head. That’s down 82% from year-ago levels, which were about 330,000 head at this time.

Cattle placements since November of 2024 have run about 4% below year ago levels, with February placements the lowest monthly figure seen since February of 2015. The consecutive years of smaller calf crops are starting to show up in the on-feed data, and at present, points to tight cattle numbers for the May, June and early July timeframe.

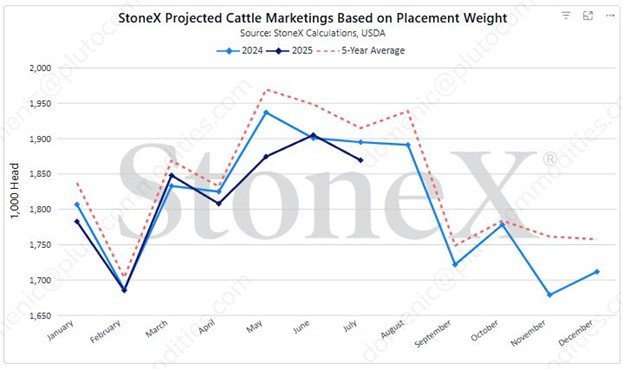

Using StoneX Financial Inc - FCM Division’s projected cattle marketings based on placement weights we can define the shortfall in numbers a little better. See the chart labeled “StoneX Projected Cattle Marketings Based on Placement Weight.” For the months, April, May, June and July, it looks like there are 100,630 head less to market this year versus 2024. May’s deficit is the largest monthly deficit with 62,530 less cattle placed against that timeframe.

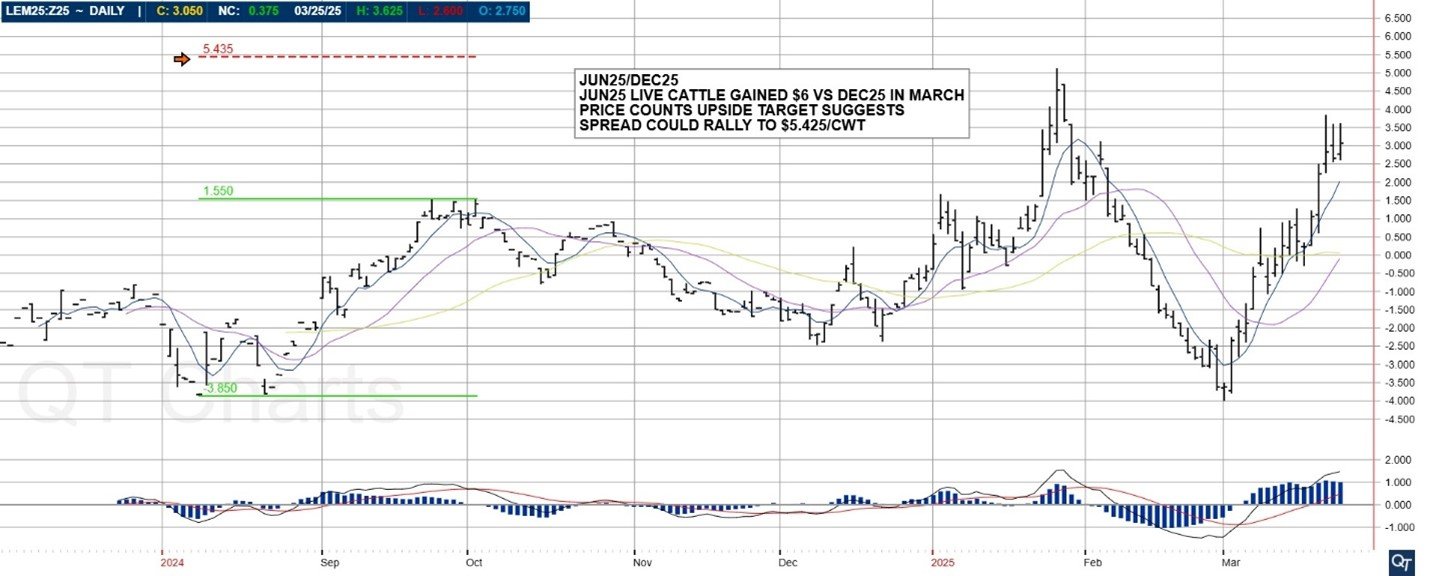

What’s all of this mean for cattle prices? Two things to consider. First, look at the June/Dec live cattle spread chart. Note that June live cattle hold a $3/cwt premium to the Dec 25 contract. That’s the futures market admitting there’s a supply hole in that June timeframe. That spread traded as high as $5.125/cwt back in January.

This spread suggests that the market may need/want the cattle in June, not later. That’s the scenario I believe this market is heading for. It will try and demand we pull cattle numbers forward in June in order to satisfy early summer beef demand.

Our current price counts targets for June 25 live cattle suggest that the outright June 25 contract could see a move up to $216.65/cwt. June 24 live cattle futures expired at 193.50 last year, which was a new all-time spot live cattle contract expiration high. A move to 216.65 would be 12% above June 24 expiration. Is that an unreasonable expectation?

Consider that Jan 25 feeders expired at 281.90/cwt, which was 21.5% above Jan 24’s expiration at 232.025. Aren’t January feeders just June live cattle before they’re placed? If feeders were 21% more expensive this year in January, is it unreasonable to think that June 25 live cattle could be 12% above year ago levels? I think not!

Cited source for first paragraph of this article:

Ricci, Peter Thomas. “Power of Meat Presents 2024’s Biggest Meat Trend” www.meatingplace.com, Publish Date: 03/25/2025, https://www.meatingplace.com/Industry/News/Details/118433, Accessed on 03/25/2025.

This material should be considered as the solicitation of trading strategies and/or services provided by the Andrew McCarty Inc. DBA Pluto Commodities noted in this presentation. These materials have been created for a select group of individuals and are intended to be presented with the proper context and guidance. Information contained herein was obtained from sources believed to be reliable but is not guaranteed its accuracy. These materials represent the opinions and viewpoints of the author and do not necessarily reflect the viewpoints and trading strategies employed by Andrew McCarty Inc. DBA Pluto Commodities. Commodity trading involves risks and past financial results are not necessarily indicative of future performance. Any hypothetical examples given are exactly that and no representation is being made that any person will or is likely to achieve profits or losses based on those examples. Andrew McCarty Inc. DBA Pluto Commodities is not responsible for any redistribution of this material by third parties, or any trading decisions taken by persons not intended to view this material. This material does not constitute an individualized recommendation, or take into account the particular trading objectives, financial situations, or needs of individual customers. Contact designated personnel from Andrew McCarty Inc. DBA Pluto Commodities for specific trading advice to meet your trading preferences or goals. Reproduction without authorization is forbidden. All rights reserved.

Varricchio is co-founder and vice president of Pluto Commodities.