Market outlook

Expect a slower herd rebuildBy Lance Zimmerman

The beginning of the next cattle cycle is near, and cow-calf producers will be tasked with building a more economically viable herd as outside demands on production agriculture intensify. But it is important to realize the cow inventory lows are still a year or two away from being realized, and the next rebuild faces significant headwinds.

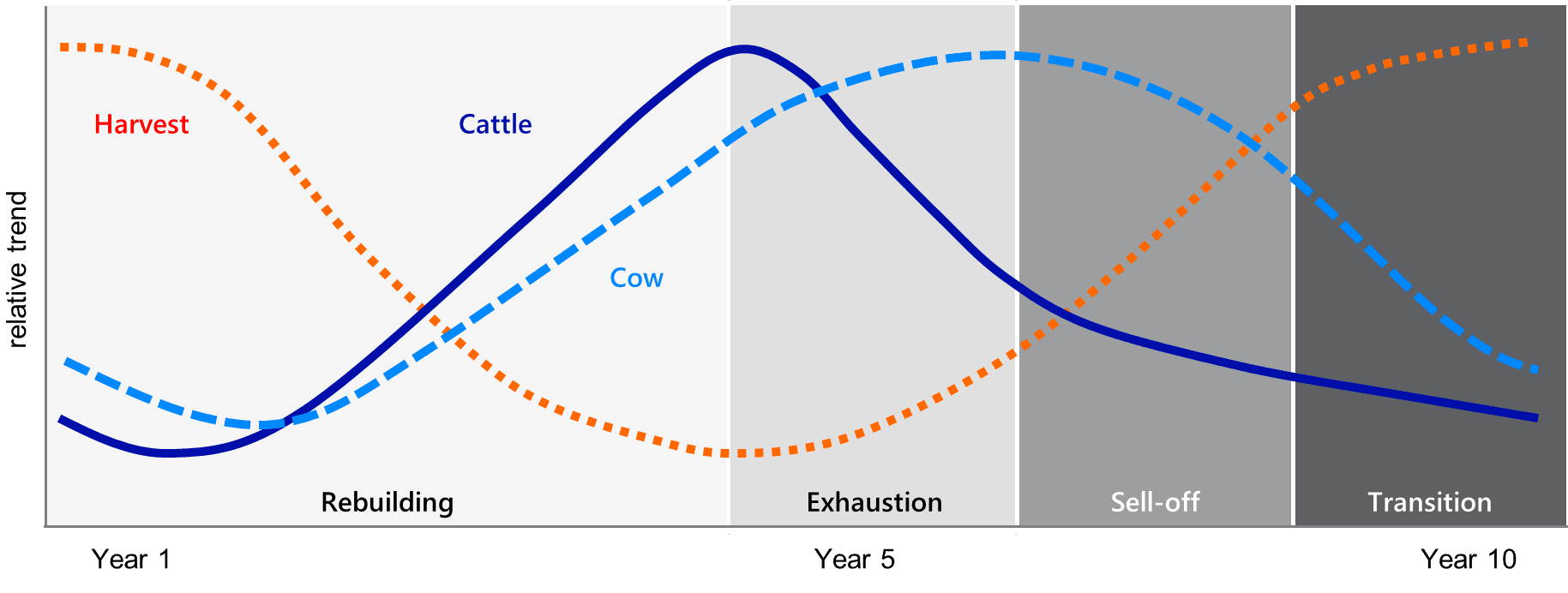

The cattle cycle is a unique fundamental dynamic compared to other agricultural markets – both within the United States and around the world. It can reference beef cow numbers, cattle prices or beef production. Each of these variables operates in concert with the others and exhibits defined long-run peaks and valleys with approximately 10 years between each historical high or low.

The timing of when each market indicator reaches its relative highs or lows can vary considerably (see Figure 1), and that lead and lag between the various factors can often make market participants impatient. It is important to recognize cattle cycles have long tails, and simply seeing the end is near does not mean it has arrived.

Slow transition from liquidation to expansionA declining culling rate does not mean herd rebuilding is here. It may be inevitable, but the extreme rate of beef cow culling and heifer dispersal in 2022 most likely means the beef industry is still two years away from meaningful herd rebuilding. Cattle producers culled a record-large 13.4% of the beef cow herd in 2022. The culling rate is expected to decline to 12.0 to 12.5% in 2023 and should reach a rate closer to 10% by 2025 which suggests herd stabilization. However, that trend depends on improving forage resources and cow-calf operation cash flow.

The beef supply chain is expecting a ramp up for the next herd expansion with a few new entrants already established in the packing segment and four larger regional processing plants in some phase of fundraising or construction. But the payoff for those investments is still likely years away. Significant reductions in cattle slaughter and beef production are expected as the industry waits for the shift.

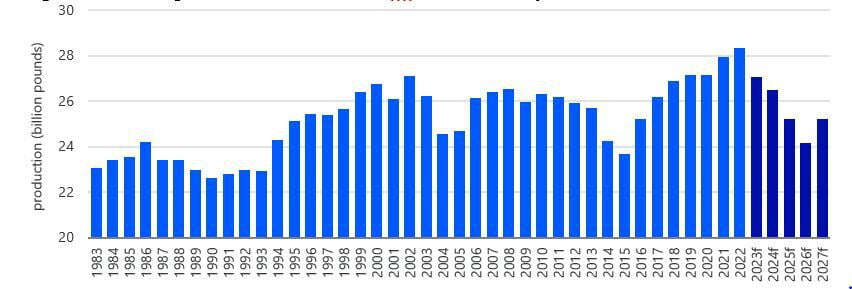

The latest USDA Cattle Inventory report shows the Jan. 1, 2023, U.S. beef cow inventory at 28.9 million head. That is a 2.8 mil. head decline from the 2019 highs. However, 2022 beef production set new record highs 28.3 billion pounds. Pandemic-related processing disruptions followed by extreme drought conditions in major cattle-producing regions created a four-year gap between the start of cow herd liquidation and the declining beef production that will become more prevalent this year.

Continued herd contraction – and the eventual transition to heifer retention – mean it is plausible that U.S. cattle slaughter will decline between 1.0 mil. and 1.5 mil. head per year for the next four to five years before increasing again. Annual beef production could decline 4 bil. lbs. over that time before moving higher once again (see Figure 2).

Herd liquidation and expansion phases generally take years to develop within each cattle cycle – well beyond the initial onset of the environmental and/or economic conditions that spur those transitions. Turning toward an expansion mindset and away from recent cow liquidation trends is at least two years away for most U.S. cattle producers.

Need for wetter weatherLong-term weather forecasts from the National Oceanic and Atmospheric Administration in the United States call for La Niña conditions are likely to persist through the winter before transitioning to a more neutral pattern by spring and a wetter El Niño pattern by summer. Weather patterns shift over months, and it seems a much-needed transition will occur in 2023. A considerable shift in precipitation patterns will be necessary to break the recent liquidation trend. And wetter weather patterns will need consistency and strength to rebuild depleted water and forage resources across most major U.S. calf-producing regions before the segment will invest in the next herd replacements.

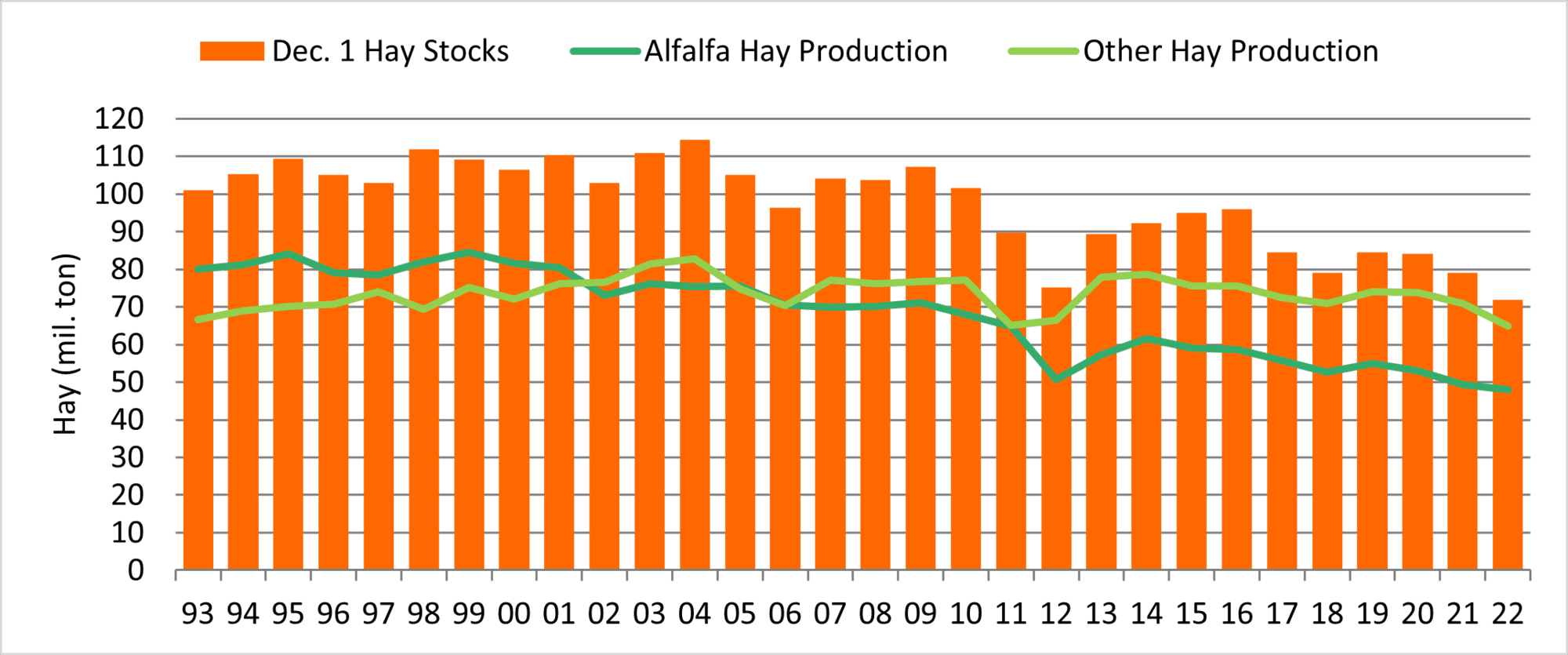

Hay stocks on U.S. farms and ranches on Dec. 1 were at the lowest level since 1990 at less than 72 mil. tons (see Figure 3), and the percentage of pastures in moderate or worse drought were at the highest level since 2012 (51%).

The precipitation needed to rebuild the feed and forage base of U.S. ranches and facilitate a cow herd expansion takes multiple years of average to above-average pasture conditions. That is the next ingredient needed for a cow herd rebuild. With cow-calf producers sitting on the smallest winter hay inventory on record, a relatively dry start to the next grazing season in major cattle-producing regions would do little to improve sentiment in the segment but recent winter moisture is helping.

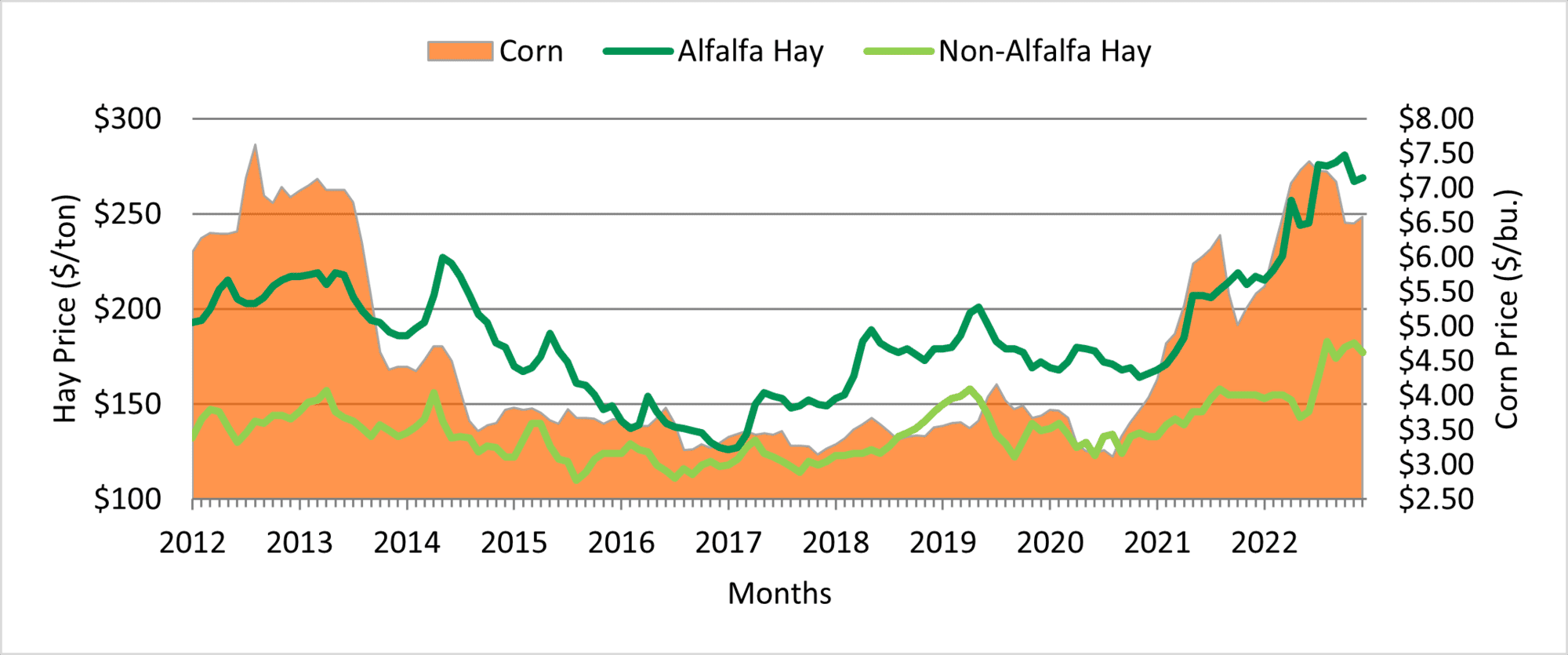

Feedstuff competitionIncreased competition for feed grains and oilseeds is also changing the cost structure for livestock and poultry operators as the beef industry transitions into the next cattle cycle. Feed grain and forage prices have adjusted to all-time highs over the last two years (see Figure 4), with drought, global conflict, logistics disruptions, energy price increases, renewable energy market growth, higher farm input costs, and a lack of feed alternatives all playing a role.

These factors will remain market considerations for the next several years, but none may have a more long-lasting effect than the development of renewable diesel. With farmland acreage holding relatively steady, the corn market may find itself increasingly tied to energy markets as it fights to preserve acres and production.

During the 2022/23 marketing year, corn was planted on 88.6 mil. acres, while soybean acreage was 87.5 mil. Announcements for new soybean crush facilities and renewable diesel plants have been consistent for the past several years. Rabobank estimates suggest the US will need several million more soybean acres or considerably smaller soybean exports to adequately supply the recently proposed crush capacity.

This increases the likelihood that the higher trading range for soybean and corn prices will continue for the next several years – similar to when the corn market moved to a higher demand level after Congress increased funding for the Renewable Fuel Standard program in December 2007.

Higher corn costs will be a constant consideration in cattle feeding profitability as the next cattle cycle approaches. In the second half 2022, higher fed cattle prices cushioned the blow from elevated costs of grain. That higher price trend will need to continue into 2023 and beyond to offer more price upside for all classes of cattle.

The risk is that eventually, the higher feed costs will need to be passed along to the consumer in the form of higher beef prices. But US beef, pork, and broiler production reached a new all-time high of 101.5 bil. lbs. in 2022, marking the eighth consecutive year these sectors established a new production record.

Even as beef production pulls back, total animal protein production will remain historically large – and demand will remain a threat to cow herd expansion if product struggles to find a home with US consumers or in the global marketplace. Ample pork and poultry supplies offer cheaper alternatives. Consumer pushback could limit beef and cattle market upside and stifle upstream demand for feeder cattle and calves if higher feed prices persist.

Planning for the next herd expansionThe book has not closed on the recent cattle cycle just yet. Until that changes, the entire U.S. beef sector needs to prepare for a relatively fluid supply situation that will take years to work through the system. Procurement strategies and market expectations will need fine-tuning throughout the sector as one phase of the cattle cycle transitions to the next. Beef supplies are most likely going to fall by more than 10 percent over the next four years.

Processors will face a situation that has been relatively foreign to them over the last seven years. All classes of cattle supplies will shrink, and the financial viability of packing plants, value-added processors, and distributors will be stressed as each participant fights to maintain capacity utilization. Declining cattle and beef production should not lead to additional facility closures. However, battles for market share will intensify and the recent additions in this sector will face additional margin compression, while construction and fundraising for new facilities will face more scrutiny and skepticism.

Cattle feeders need to continue to operate with intense discipline on production and risk management, but cash positions will be increasingly stressed in an environment where cattle supplies tighten and corn prices remain historically high. As a new cycle begins, those who control the cattle supply generally find more profit opportunities, and that is what leads to herd expansion. However, the pressures being faced by all cattle producers run the risk of limiting opportunity more than in the most recent cattle cycle.

This topic is explored in greater detail in a recent RaboResearch Food & Agribusiness report titled Not So Fast: Rebuilding the Herd Will Take Time. The full report is accessible to Rabobank clients here and outlines additional market forces that are likely to create a slower, more calculated transition into the next cowherd rebuild.

A bullish cattle inventory report, consumer meat demand weaker than a year ago, and increased input prices on top of lingering drought conditions, what’s the long-term market outlook for the beef industry? Joining us today to discuss these topics and more from the Cattlemen Industry Convention in New Orleans is Lance Zimmerman of Rabo AgriFinance.

Zimmerman is a senior beef and cattle market research analyst with Rabo AgriFinance.