Market Outlook

Prices are boomingBy David Anderson

Six weeks into 2025 and cattle prices continue to boom. It’s not just cattle prices but cutout values and meat prices keep moving higher. Within the broader cattle and beef market some sources of volatility remain that will likely mean some ups and downs as we head into spring.

PricesThe drive to new record high prices really started last fall and continued into 2025. The price increases have been broad-based across everything from cull cows to calves to feeders to beef. Each of these types of animals and beef have their own seasonal price patterns due to relative supplies and demands that will affect their trajectory in coming months.

Cull cow prices have jumped more than 10% so far this year. They tend to increase until about May-June benefitting from burger grilling demand in spring and reduced total cow culling that time of the year. This year they continue to be boosted by historically low cow numbers that is contributing to sharply lower beef cow slaughter. Dairy cow culling rebounded in January to actually exceed that of the prior year for the first time in almost a year and a half but has since declined.

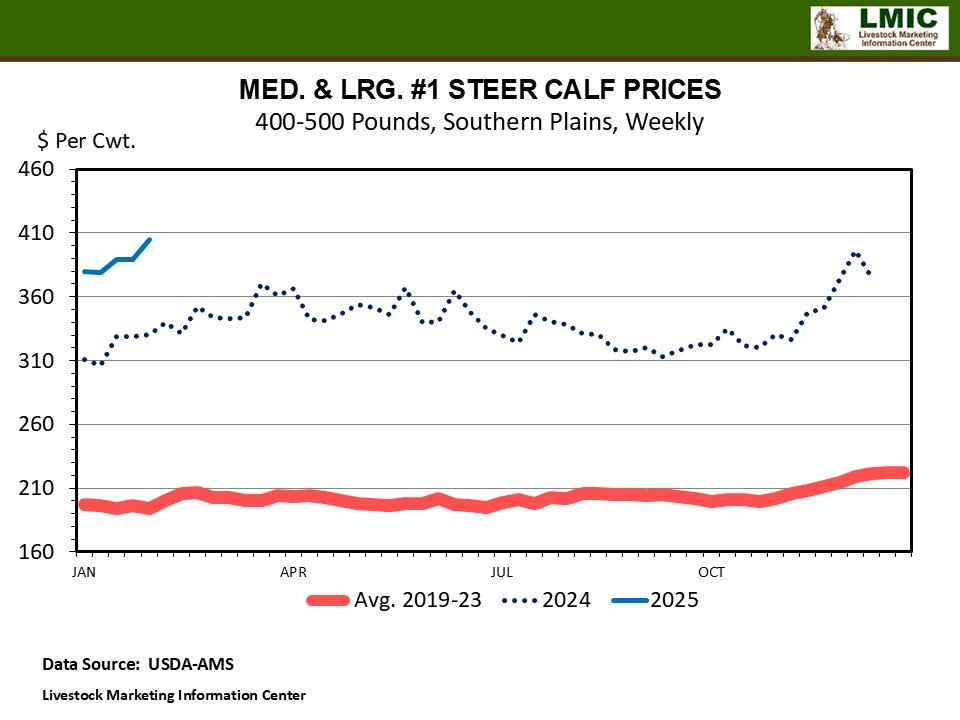

Steers weighing 400-500 pounds hit over $4 per pound in Southern Plains auction markets. Prices tend to increase for this weight class in spring often due to a relative lack of supplies. No doubt these lightweight calves are being boosted by the closing of the border to Mexican calves bound for U.S. grass and feedlots due to the finding of a cow with screwworms in Southern Mexico, bordering Guatemala. While procedures for importation have been finalized and signed, as of this writing no cattle have crossed the border yet. Last year over the 10-week period from late November through Feb. 1, 282,666 feeder cattle were imported from Mexico. That’s a fairly significant cut in available supplies of calves.

Feeder cattle in the Southern Plains climbed to almost $290 per cwt. Heavier feeder prices tend to be pressured from March-May as wheat pasture cattle hit the market. But, tighter supplies, in general, and fewer calves from Mexico that would have gained weight to be sold later this spring may keep boosting prices.

Feeder prices have certainly been boosted by higher fed cattle prices. The five-market average hit $210 before backing off in the second week of February. It’s not unusual to have fed cattle prices back off before running to their spring highs. A little less beef supplies are helping to boost prices but it appears that beef demand is helping too.

Beef productionOver the first six weeks of 2025 beef production is 2.4% great than last year. The big contributor to production continues to be steer and heifer dressed weights. While the big winter storm in January may have taken a toll on weights, average steer dressed weights, at 948 pounds, were almost 30 pounds more than the year before.

That the Choice beef cutout is 11% higher than a year ago with more total beef production does suggest continued positive beef demand. More total beef production has been coupled with a small decline in the percent of beef grading Choice. While Choice was down a little, Prime grading beef was up more than a full percentage point to 11.1% in early February. When combined with more beef production than last year, so far in 2025, there are ample supplies of high quality grade beef for consumers.

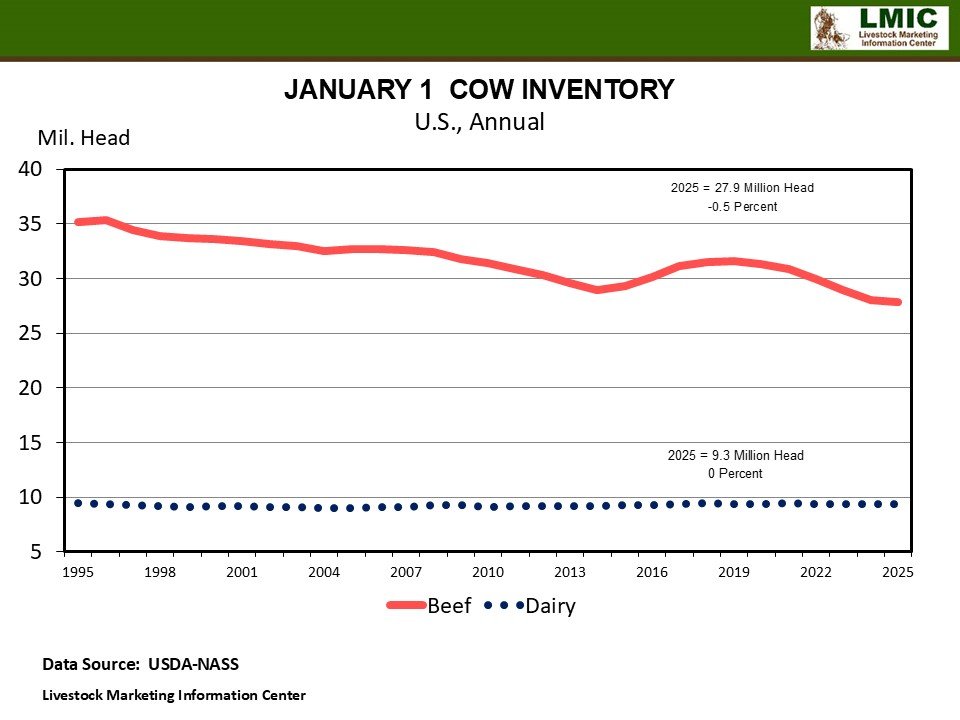

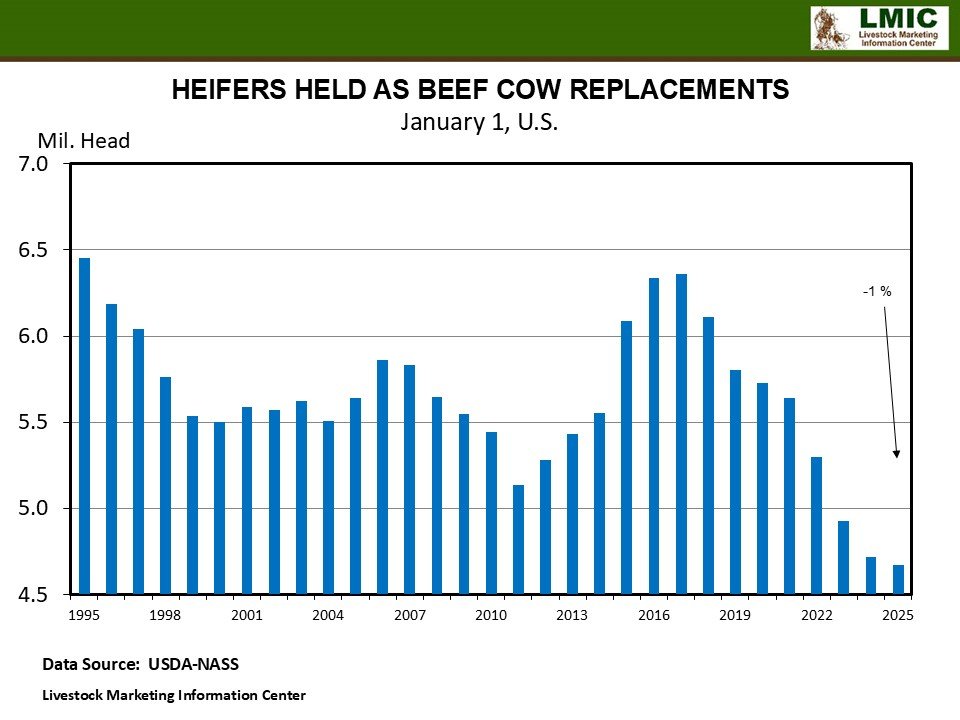

Longer termThinking ahead, there are some interesting longer term things to watch for in the market. USDA’s cattle inventory report certainly confirmed a smaller cow herd in 2025 than 2024. The rate of decline in cow numbers in this cycle has slowed. But, a number of beef cattle heifers reported held for replacement continued to decline. Even higher calf prices are yet to come when heifers begin to be held back for herd expansion. Expansion will start when calf prices get high enough to make it worth holding new heifers.

On the feedlot side, almost 1% fewer cattle were on feed Jan. 1. Some decline was likely due to the lack of Mexican feeder cattle some was due to fewer calves available. As on-feed supplies decline more later in the year beef supplies will tighten up, supporting prices even more. Fewer cattle on feed will have an interesting impact on weights. Heavier weights have supported beef production.

Many have discussed the economic reasons that a feedlot would want to have cattle on feed longer and sell heavier animals. It’s worth remembering that there is a packer side to weights also. Heavier weights have allowed packers to keep production high with fewer animals to process. Yet, at some point, packers may need the animals to maintain an efficient number going through the plant. Demand for the animals could result in pulling animals in sooner resulting in lighter weights and reducing weights. That will be a really interesting dynamic later in 2025.

Many of the longer-term questions will introduce more uncertainty into cattle and beef prices. A lot of these sources of uncertainty deal with policies like tariffs and immigration and might be more controversial. We might consider beef demand a source of uncertainty as consumers deal with higher beef prices.

The threat of tariffs and retaliation are an important source of uncertainty. We import more beef today because much of what we import are lean beef trimmings for ground beef. We don’t have enough cull cows to get as much very lean beef as we want. Import tariffs would raise those prices. Yet we also export beef. Retaliatory tariffs on beef exports would reduce prices. The net effect on cattle and calf prices is harder to figure out.

Resuming imports of Mexican feeder cattle would likely pressure calf prices lower. When imports resume and the speed of imports coming adds some uncertainty to calf prices. While closing the border to imports has boosted calf prices longer-term it will reduce beef production and add some pressure for higher retail beef prices to consumers. Higher prices to consumers will have some negative ramifications for beef demand.

On balance, there are a lot of moving parts, short and long term, in the cattle market. Longer term supplies will keep supporting cattle prices even though it might not be smooth sailing every week.

Anderson is a professor and Extension economist in livestock and food product marketing in the Department of Agricultural Economics at Texas A&M University.