Not your father's cattle market

What are cattle crush spreads telling us?By Domenic Varricchio

Ideas on beef production and the supply of cattle for 2024 have changed a lot over the last three months. The October “Cattle on Feed” report surprised the entire market with a very large placements number. That trend was seen again in December. So, we saw higher than expected placements in three-out-of five feedlot inventory reports from May 2023 onward.

Marketings of cattle have been slow from September onward. This has allowed cattle to “back up” in feedlots. The evidence for this is seen in the heavy carcass weights and the days on feed in closeouts.

Sluggish cattle marketings and lower than expected fed slaughter rates into the fourth quarter of this year has retailers suddenly comfy with beef supply. This is evidenced by the fact that retailers are content with going hand to mouth on beef purchases.

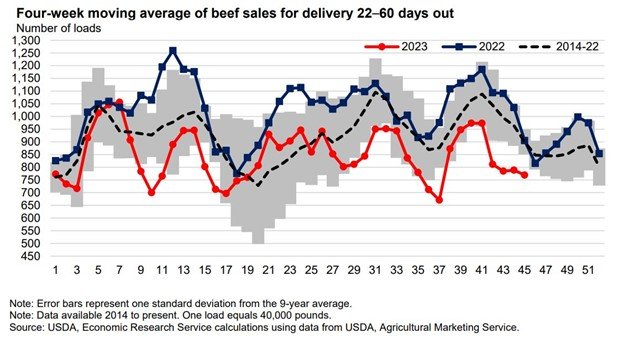

The lack of forward bookings of beef by retailers was pointed out by the USDA in their November 2023 “Livestock, Dairy, and Poultry” outlook. Volumes of beef purchased for +22 days ran over standard deviation below the eight-year average for the holiday season. Some of this lack of buying is attributable to beef production in 2023 being less than 2022. However, this purchasing behavior emphasizes the fact that retailers are using a just-in-time purchasing strategy in beef. Spot market beef volume, meaning beef bought for delivery within 20 days, is one standard deviation above the average for the same Oct/Nov time period.

With all this being said, it is this writer’s opinion that the retailers aren’t holding a lot of beef inventory. They seem to be operating under the assumption that larger-than-expected feedlot numbers will provide them with plenty of beef through at least the first quarter of 2024.

I think cattle traders need to be diligent in looking at the forward bookings of beef heading into Q1 and Q2 of 2024. If there is any change to the above-mentioned assumption by retailers, they should show their hand and begin purchasing beef in the forward market again.

What impact has this had on the cattle market? Full feedlots, higher-than-expected placements last fall and slower-than-expected marketings caused feeder cattle prices to fall faster than fat cattle prices into December. This is evidenced in the cattle crush spreads.

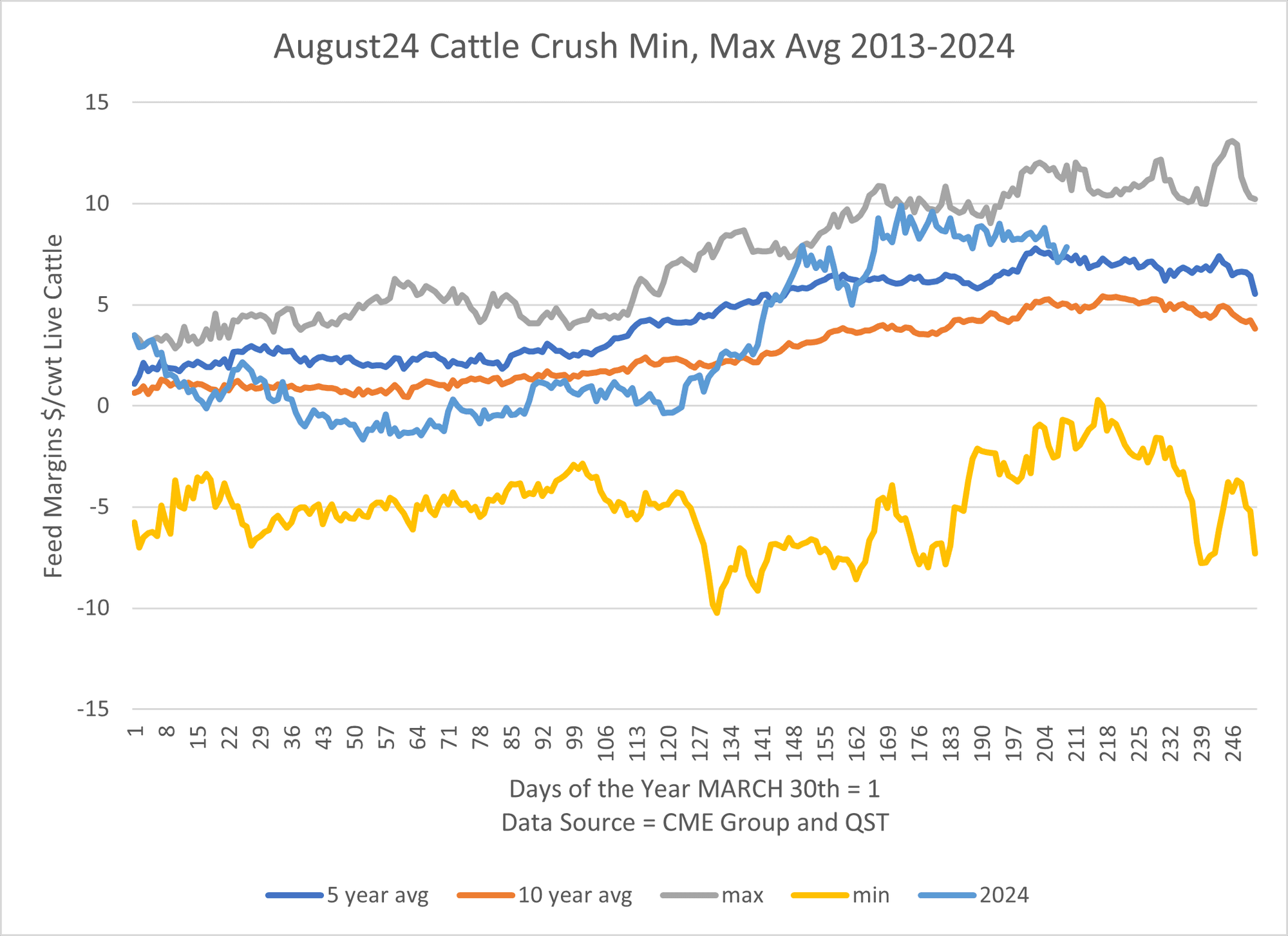

At Pluto Commodities, we track these spreads to gain an idea of what the board is paying operators to feed cattle. Citing the CME’s own “Cattle Feeding Spreads” whitepaper, we like to look at the 4-3-8 cattle crush spread- meaning owning four feeders, three corn contracts and selling eight live cattle contracts. We feel this ratio best reflects feeding margins in the current marketplace.

When looking at the August Cattle Crush Charts, know that March 30 is equal to Day 1 in the year for those charts. A new crush spread is born when the next March feeder contract comes into existence. We are looking at the August crush spread in terms of a March-to-March calendar year.

So, what is this spread telling us? Looking at the Aug. 24 crush, which involves owning four March 24 feeders, three May 24 corn and selling eight Aug. 24 live cattle contracts, it is at +$8.60/cwt. at the time of this writing on Dec. 26, 2023. That means, live cattle prices are high enough above the feeder and corn input cost where one could turn a profit feeding cattle on paper. This method doesn’t account for basis or death loss.

The August crush spread has made a $7.00/cwt. rally since early October. Feeding cattle became more profitable on the board as feeder cattle prices broke from late September onward. When crush spreads are positive, it encourages operators to retain ownership on cattle.

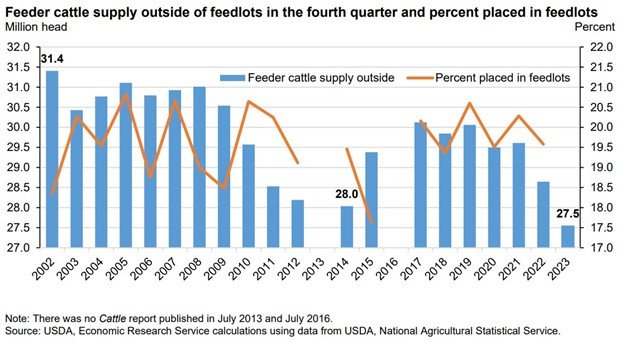

If we start to see this happen, smaller feedlots may start to fill up, with cattle operators deciding to retain. This could further cut into what is already predicted to be a record-low number of feeders available in 2024. See the chart labeled “Feeder Cattle Outside of Feedlots in the Fourth Quarter and Percent Placed in Feedlots.”

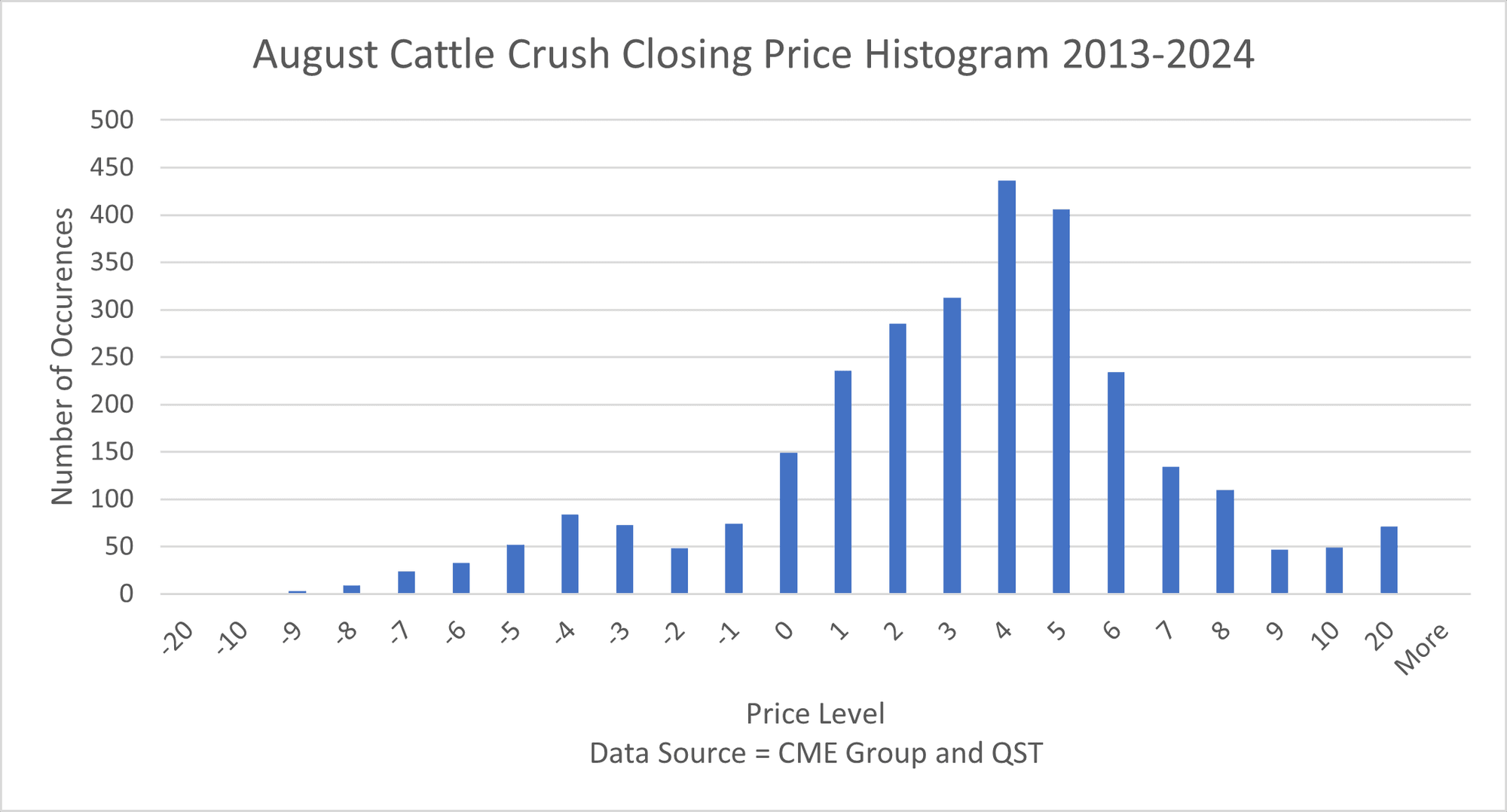

Looking back over the last 10 years, the Aug. 24 crush spread is at the second-highest level for this time of year. 2023 was the only year where the August crush was higher. When considering the value of this spread, we like to look at a price histogram and observe how many times a price level was hit over the last 10 years.

Looking at the price histogram chart labeled “August Cattle Crush Price Histogram,” we can see that +4 and +5 are the most common price levels for this spread to trade at over the last ten years. At the current price of +$8.60/cwt., we can see that the spread is near the upper end of value when looking back over the past 10 years.

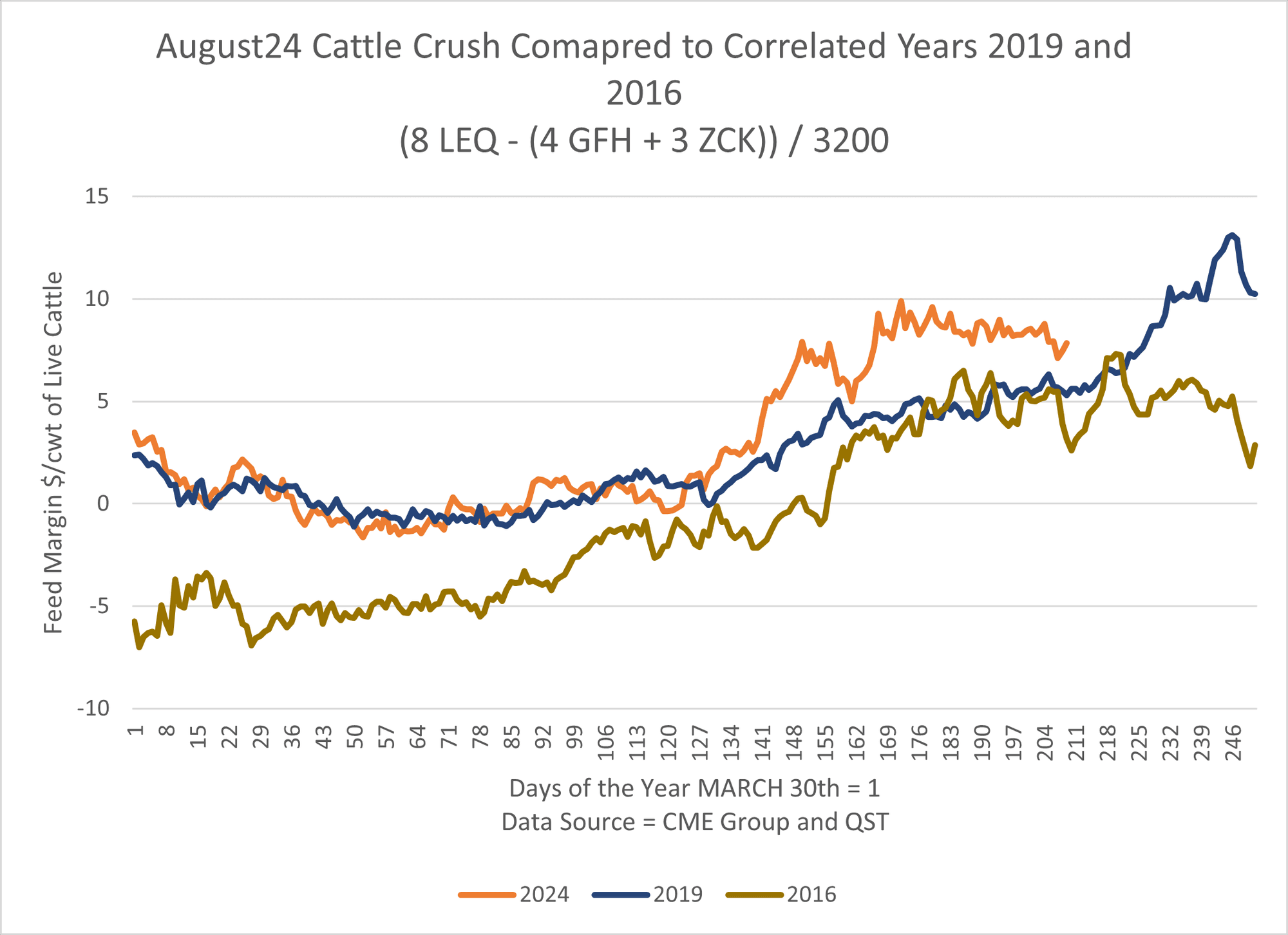

Another thing to look at for this Aug. 24 cattle crush spread is correlation between years. I looked back over the last 10 years of price history for the August cattle crush and found that this year’s price action is significantly correlated (greater than +.80) with the years 2016 and 2019. In 2019,the August crush spread ran up to new highs heading into expiration and peaked out around $13.00/cwt. before March feeders expired. In 2016, the crush spread chopped sideways around the +$5.00/cwt. level and finished at +$2.875/cwt.

Note that the Aug. 24 crush spread is higher than both 2019 and 2016 for the December timeframe. This means more margin to feed cattle, which I think encourages more ownership retention of cattle into next year.

That’s the bottom line here. A profitable board crush spread for the Aug. 24 crush is telling cattle operators to retain ownership and keep feeders on feed instead of running them through the sale barn. I believe this could lead to less feeders being available in the second quarter of 2024. This just happens to line up with the turn of cattle after February.

If the October “Cattle on Feed” report told us that there were going to be plenty of cattle available to market in February, what happens when feedlots empty out in February and can’t find feeders to refill the pens in March? My guess is that feeder cattle prices will have to ration larger demand chasing the smaller supply in that timeframe.

Sources:U.S. Department of Agriculture, Economic Research Service. (2023). Livestock, dairy, and poultry outlook: November 2023 (Report No. LDP-M-353). USDA ERS - Livestock, Dairy, and Poultry Outlook, November 2023

CME Group. “An Introduction to Cattle Feeding Spreads” January 2014. An Introduction to Cattle Feeding Spreads (cmegroup.com)

Varricchio is co-founder of Pluto Commodities, an advisory and brokerage firm focused on agricultural, energy and metal markets.