Bizav playing supply chain ‘Whack-A-Mole’

OUTLOOK

Honda Aircraft’s head of sales compares challenges in the business aviation supply chain to a game of Whack-a-Mole.

In the game, players score points by whacking plastic moles that pop up randomly as they appear. The faster the reaction, the higher the points.

“There’s always one or two components that are on the top priority list,” Peter Kriegler, Honda Aircraft director of sales, said of supply chain challenges. That can vary from week-to-week, month-to-month and from supplier to supplier for various reasons.

“This week it’s this one; that week it’s that one,” Kriegler says of shortages that pop up.

The good news is the situation is improving.

“Everybody’s doing the best that they can,” he told BCA. “Everybody’s working well together. We’re seeing a lot of things catch up on the production side. So, that’s been good.”

It’s a common issue in the industry, and one that has mitigated manufacturers’ ability to boost production in response to near-record demand since the pandemic.

In the past two years, flight activity and pre-owned transactions have been at all-time highs, while inventory has seen all-time lows. First-time business aircraft users have flowed into the market, whether through jet cards, charter, fractional ownership or full ownership.

Today, the inability to ramp production to match demand means the industry is well positioned for an uncertain economic future, experts say.

Business aircraft manufacturers and used aircraft dealers say that the market remains busy in 2023, but it is returning to more normal conditions.

Leading industry indicators have been easing over the past six months, although “admittedly against tough comparisons,” Robert Stallard with Vertical Research Partners wrote in a recent report to investors.

Business jet activity in 2023 is down 6% compared to a year ago, with a particular weakening in leisure demand, Stallard says.

At the same time, inventory of used aircraft for sale is increasing and pricing has eased. Book-to-bill, or the ratio of new orders compared to deliveries, has declined from 2-to-1 in 2022 to about 1-to-1 in the first quarter of 2023.

“It is tough to fight the tide of a declining book-to-bill ratio,” Stallard says.

The number of used business jets for sale in May 2023 totaled 969, according to Jefferies, down from 922 in April and 590 in May 2022. Medium and heavy jet inventories rose 85% in May, compared to a year ago, while light jet inventories rose 42%.

In the first quarter of 2023, dealers closed 239 transactions of used aircraft, down from 288 a year ago but up from 213 in the first quarter of 2021. Of the transactions, 52 experienced lower pricing, compared to six a year ago. Dealers ended the quarter with 197 aircraft under contract, down from 259 a year ago, according to the International Aircraft Dealers Association (IADA).

“There is evidence that demand and supply forces are rebalancing, with less frenetic activity, more realistic pricing and a slow but steady buildup of available inventory,” says Zipporah Marmmor, IADA chair and president of transactions for ACASS in Montreal. “Although specific low-time aircraft with attractive pedigrees continue to attract top-dollar, the overall market has begun to downshift from a peak characterized by accelerating prices and strong residual values.”

Analysts agree that the industry is in much better shape than it was at the peak of the last upcycle of 2008 and through the subsequent “lost decade.” No one is predicting widespread aircraft devaluation or swelling inventories found during the 2008-09 recession.

For one, total production is down. Stallard, for example, projects deliveries of about 650 business jets in 2023, compared to a peak of about 1,100 in 2008 and 680 before the pandemic.

“Unlike in the past, the OEMS have not chased the 2020-22 surge in demand, and have instead built backlog, lead times and pricing,” Stallard says. “While no one is immune to a slowing in demand, the bizjet OEMs have much more backlog buffer than they ever had in the past, and so we should not expect significant if any changes to production plans.”

During the first quarter, the market for business jets was hurt by news of bank failures, Phebe Novakovic, chairman and CEO of General Dynamics, Gulfstream Aerospace’s parent company, told analysts on a call about the company’s first quarter financial results.

“The quarter was looking quite good until the two regional bank failures in early March,” Novakovic says. “This created a pause in the market for about three weeks. I am pleased to report that normal activity has resumed.”

Despite some headwinds in 2023, the business jet market remains resilient, Global Jet Capital officials say. It forecasts steady growth over the next five years.

In 2023, Global Jet Capital projects new deliveries to increase 6.3%, with deliveries over the next five years are expected to grow at a compound annual growth rate of 4.6% with annual dollar volume growth of 6.4%.

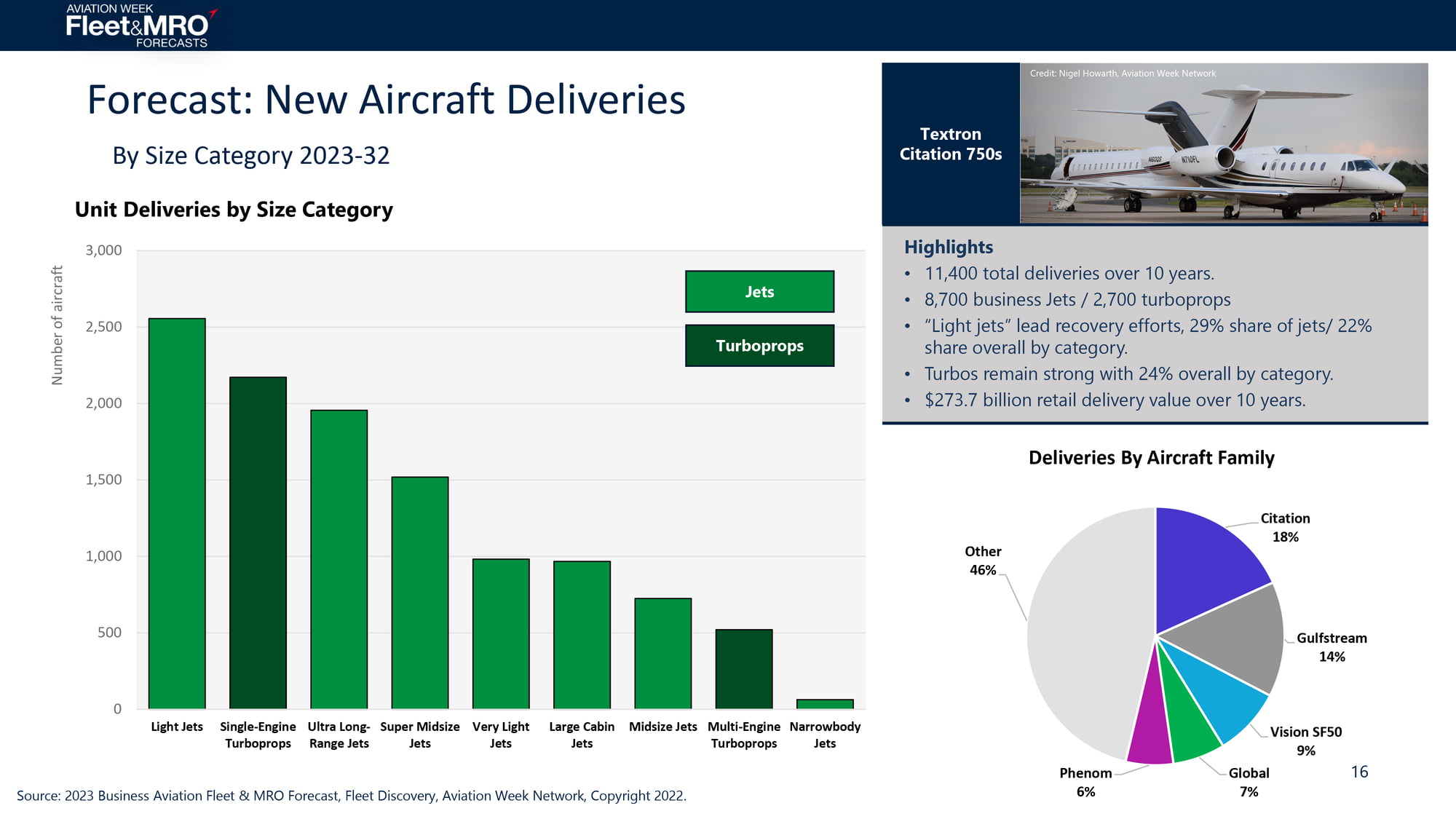

The Aviation Week Network forecasts delivery of 8,700 business jets and 2,700 turboprops over the 10 years from 2023 to 2032. It projects the business aircraft in-service fleet to expand 12% to 38,848 aircraft over the period with a compound annual growth rate of 1.3% over the period.

A forecast by Jetcraft projects steady growth to continue in the years ahead, setting new volume and value benchmarks, despite “an inevitable market correction in 2023.”

Textron Aviation had a “very nice” first quarter, Ron Draper, president and CEO, told reporters in May. “We delivered 35 jets, 34 turboprops and 46 pistons. We grew backlog in the quarter. So, contrary to a few of the naysayers out there that said the market was going to slow precipitously, that wasn’t the case. We grew backlog another $136 million, so we’re up to $6.5 billion in backlog. That was a book-to-bill by our calculation of about 1.2 in the quarter.”

Despite an uncertain economy, Draper says he sleeps better at night knowing the company has that strong backlog.

“Whether it slows down a bit more or continues where it’s at, I think either way, we’re in a good position,” he says. The company’s investment back into its products and the business mean it is in a good position. “We have a nice backlog, so we’re ready to see what comes next.”

—Molly McMillin, a 25-year aviation journalist, is managing editor of business aviation for the Aviation Week Network and editor-in-chief of The Weekly of Business Aviation, an Aviation Week market intelligence report.