Kevin Michaels Jetliner manufacturing is bedeviled by shortages of skilled labor and microchips as well as reduced parts-manufacturing capacity.

Kevin Michaels

It is heartening that aircraft OEMs are busy planning for significantly higher production rates after so much bad news. Airbus is urging suppliers to be ready for 75 A320s per month by 2025. Boeing expects to deliver more than 600 aircraft in 2022—nearly double that in 2021. While the aerospace ecosystem craves the upturn, there are two factors that will govern the pace of recovery: a shortage of skilled labor and supply chain bottlenecks.

Skilled labor has emerged as the main supply chain challenge. After major layoffs in 2020, aerospace suppliers are having difficulty bringing back employees and expanding capacity. At this stage evidence is mostly anecdotal, but my conversations with aerospace executives indicate they are operating with a workforce that is 10-20% smaller than desired.

The major mystery is why? There are a variety of hypotheses. Younger workers can earn competitive wages elsewhere and are showing less interest in aerospace. Recent evidence suggests that labor participation decreases are concentrated among married couples when one of the spouses leaves the workforce. Older workers may be enticed into early retirement by record stock market prices and home values. No industry is immune from what some economists call “The Great Resignation.”

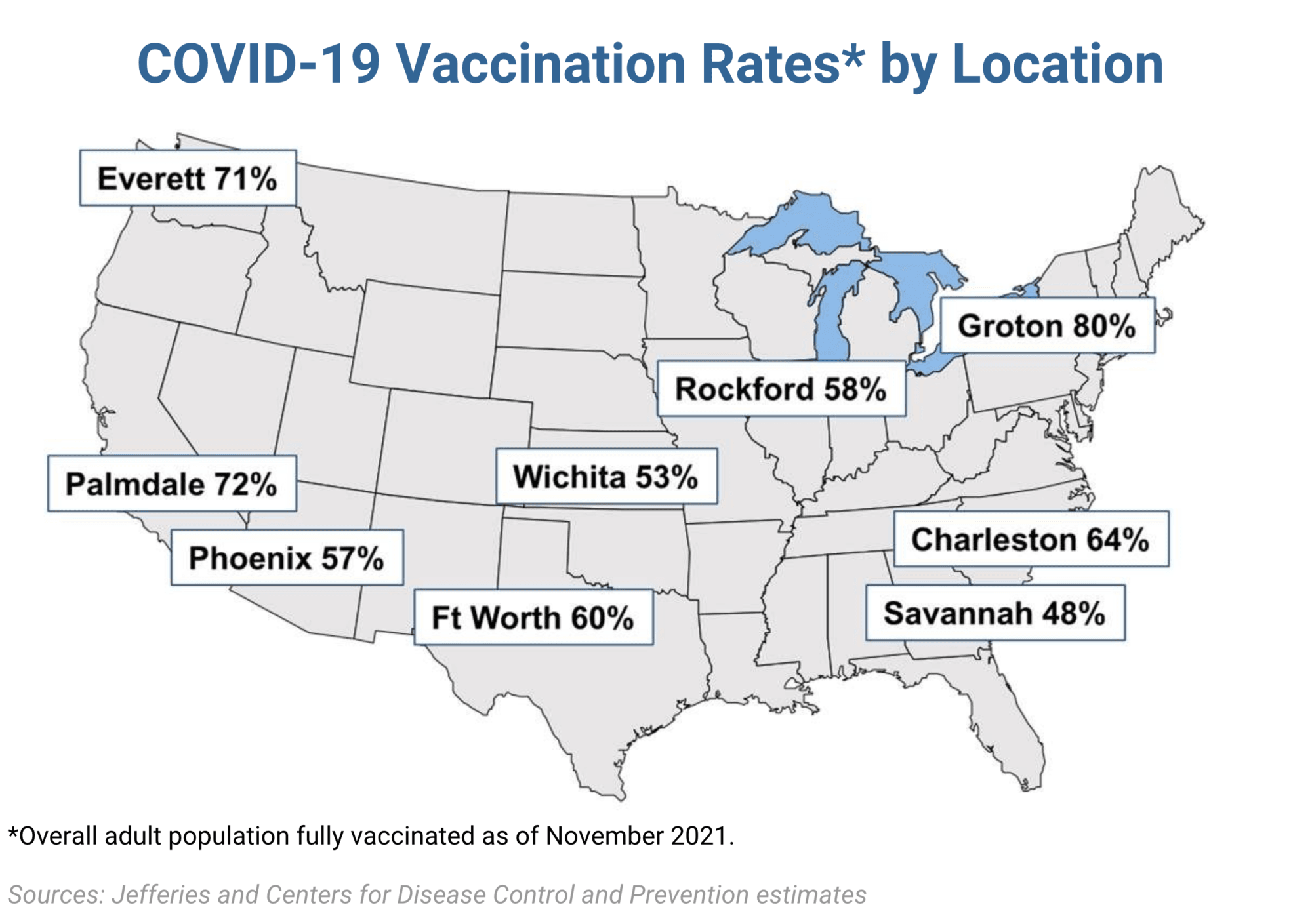

The Biden administration’s Jan. 18, 2022, deadline for federal contractors to be vaccinated against COVID-19 introduced a wrinkle into this tenuous supply-demand challenge. Consider Wichita, where just 53% of adults are vaccinated. The machinists union there, which includes more than 12,000 employees for Textron Aviation and Spirit AeroSystems, is pushing back against the mandate. Other manufacturing hubs also have low vaccination rates, including Phoenix (57%); Fort Worth, Texas (60%); Savannah, Georgia (49%); and Charleston, South Carolina (64%). Mass mandate-related resignations could be devastating for an already struggling supply chain.

Small subtier suppliers, already reeling from the 737 MAX production shutdown and the COVID crisis, are especially vulnerable. Many already lack the working capital to support a production ramp-up, and when coupled with a skilled labor shortage, they may be pushed to insolvency. Paradoxically, more failures are likely in the next 18 months than in the prior 18 months during the peak of the pandemic.

The labor situation is attracting interest from the Pentagon and Congress. Sen. Tommy Tuberville (R-Ala.) recently sent a letter to President Joe Biden and Defense Secretary Lloyd Austin seeking to reverse the executive order, opining that “the American war-fighter is ultimately harmed when skilled workers leave the defense contractor workforce, a foreseeable consequence of your order.”

Beyond skilled labor, aerospace executives are concerned about several specific inputs. The same microchip shortages that idled automobile factories are now affecting aerospace suppliers of electronics components. Compounding the issue is the fact that many aerospace applications feature older-generation chips, which are out of favor at foundries. The situation is “awful,” one supply chain executive says.

Investment castings and forgings—major pre-COVID bottlenecks—have reemerged as issues in the aeroengine supply chain. Reduced capacity is the culprit. Precision Castparts (PCC), a major supplier of both, eliminated 10,000 employees last year, one-third of its workforce, as it took a $9.8 billion write-down of assets. Some 4,300 employees were laid off at PCC rival Howmet Aerospace in 2020, nearly 20% of its workforce. This underpins what one executive described as a nightmare scenario: strong aeroengine production rate increases in 2022-23 coupled with surging aftermarket demand overwhelm forging and casting suppliers, which are unable to add and train skilled labor fast enough.

Chemicals and adhesives are another concern. The deep freeze that triggered mass blackouts in Texas last February led to chemical plant shutdowns, which continue to disrupt aerospace supply chains. Stycast, a thermally conductive epoxy, is an example.

With these considerable bottlenecks having an outsized impact on aeroengine suppliers, it is not surprising that Snecma is publicly pushing back against Airbus’ push to take single-aisle production to uncharted levels. It looks like the weakened supply chain—not air travel demand—will determine the timing and magnitude of the jetliner ramp-up.