Richard Aboulafia Enabled by cash from parent defense prime General Dynamics, the market leader is poised to maintain its dominance for many years to come.

Richard Aboulafia

Credit: Gulfstream

Gulfstream’s announcement of the G400 large-cabin and G800 very-long-range business jets in October represents an interesting development in the market. Funded by parent defense prime General Dynamics, the market leader is poised to cement its dominance for many years to come, with only modest risk to profitability.

The G400 is particularly intriguing because of the opportunity it presents and because of the competitive factors in that segment. It will compete with Bombardier’s Challenger 650 and Dassault’s Falcon 2000LXS. The 650 is the latest iteration of the Challenger 600, which first flew in 1978, making it easily the oldest business jet design still in production. The 2000LXS is the latest iteration of the Falcon 2000, which first flew in 1993. The latter jet might be able to last a few more years with discounting; the Challenger 650 will simply be forced out of the market.

Given the age of the Challenger 600/650, Bombardier needs a clean-sheet design to respond to the G400. Dassault may create a new derivative of its existing models, or it might need something all-new, too. But neither company is in a position to respond. Bombardier’s debt is nearly $6 billion, and it narrowly averted a debt-covenant breach this year. Dassault is just finishing development of its ambitious Falcon 6X and has also committed to its largest ever Falcon, the 10X, which will absorb all of its development resources for the next five years (AW&ST May 17-30, p. 10).

Other than the 650 and 2000, the G400 is aimed at a big, empty space in the market—there is nothing else offered, by anyone, between Gulfstream’s $25 million G280 and its $45 million G500. That $20 million gap has been defended by two of the oldest designs in production.

Economists say you should not be able to find a $100 dollar bill lying on the sidewalk, but at least for the G400 and its market segment, that is what Gulf-stream has done. And in terms of development costs, offering these models is an inexpensive way to leverage investments made for the G500 and G700, from which they are derived.

But recurring costs are the flip side of that coin. As derivatives of larger jets, they share the same engines, avionics, wings, fuselage cross sections and other systems. They are just shorter. But they sell for considerably less than their larger brethren—the $34.5 million G400 is more than $10 million cheaper than the G500. It is not possible to take $10 million out of a business jet’s production costs by removing a few feet of fuselage length. The other costs remain the same.

This reality may replicate what happened with Gulfstream’s G300/G350, which were G450 derivatives with reduced capabilities and prices. Gulfstream built just 24 of these in the 2000s, and company executives said they were much less profitable than the G450. Hawker had the same experience with its 750, a less capable Hawker 800.

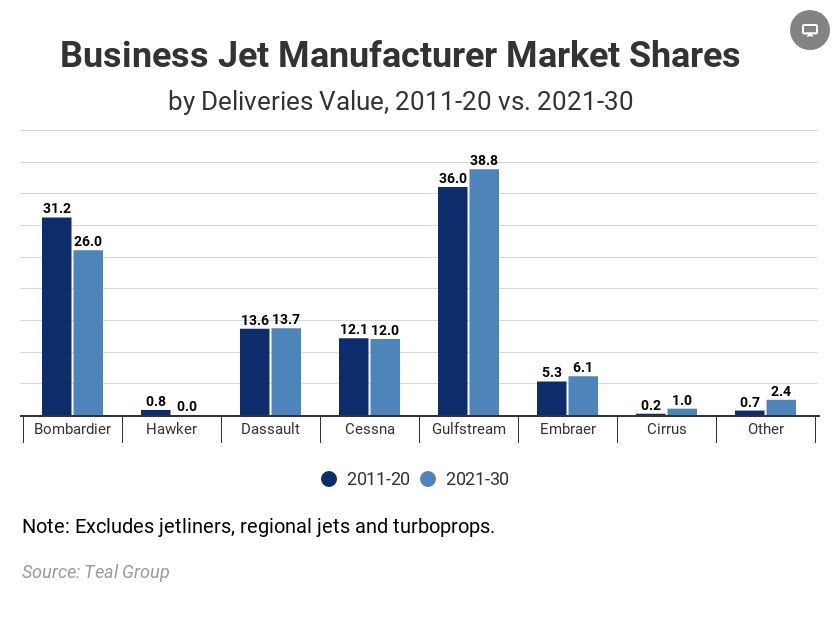

Even though the new jets may dilute Gulf-stream’s profit margins, the G400 and G800 are the right move for an industry leader, one that is well positioned to stay on top in terms of resources, product portfolio and overall brand. As the chart indicates, Gulfstream’s market share will grow to nearly 39% in value of deliveries in the next 10 years. In an industry with five major and three minor players, that is an impressive achievement.

The Teal Group forecast also anticipates that sometime later in the decade, Bombardier will find the cash to launch a new jet in the Challenger 650/Gulfstream G400 class. Given the company’s balance sheet, that might be a generous assumption. If it does not happen, Gulfstream’s market share will easily exceed 40%.

Finally, if Bombardier were to merge with Textron’s Cessna unit, the combined entity would have about the same market share as Gulfstream. The combination has been mooted before. As Bombardier contemplates its future as the only publicly traded pure-play business jet prime competing with deeper-pocketed and more diversified players, it may revisit this merger idea as perhaps the best path forward.