Michael Bruno A wave of newly minted publicly traded space companies is hitting the marketplace and sustaining investment confidence, hinting at more to come.

Michael Bruno

Credit: Virgin Orbit

Like a slew of cubesats slinging out of a ride-share rocket, a wave of newly minted publicly traded space companies is hitting the marketplace and sustaining investment confidence, hinting at more to come.

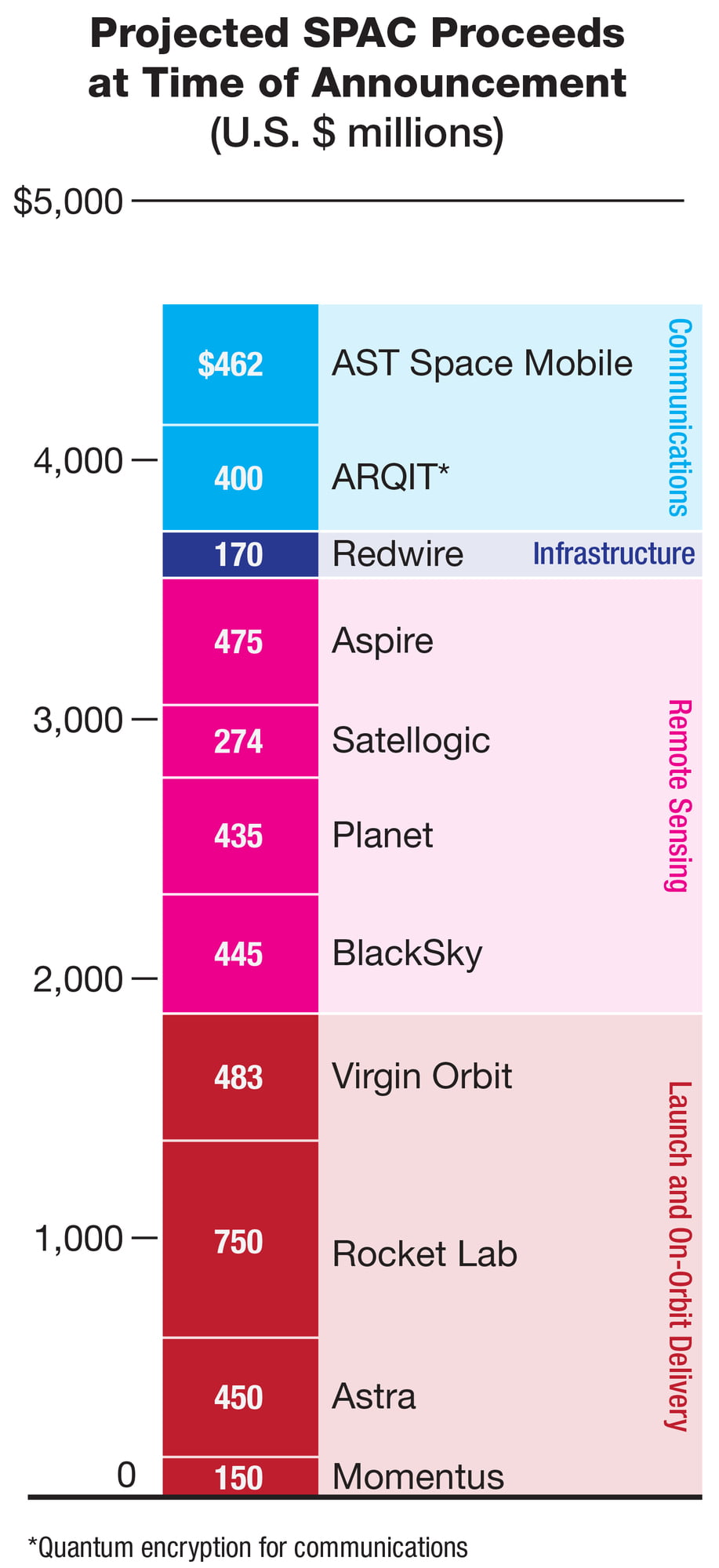

Low-Earth-orbit launch upstart Rocket Lab is the latest. It will become a publicly traded company Aug. 25 now that shareholders have approved a reverse merger with Vector Acquisition, a special-purpose acquisition company (SPAC), grossing more than $750 million dollars for the 15-year-old rocket company.

Vector shareholders approved the deal Aug. 20. Less than 3% of Vector shareholders redeemed their shares (i.e., demanded payback), so the gross amount of cash that the combined company will receive from Vector’s trust account and concurrent private investments upon closing will be around $777 million before transaction expenses.

Following close behind, Redwire, a private-equity-created new-space rollup company, will become publicly traded on Sept. 1 in a reverse merger with a SPAC called Genesis Park. The going-public event is supposed to net Redwire about $170 million, assuming no or low redemptions, and it will represent an early SPAC success for aerospace private equity firm AE Industrial Partners (AEI), which quickly put together Redwire starting last summer.

Theoretically, the transaction places Redwire at a $615 million pro forma enterprise value, representing about 9.6 times its estimated 2023 adjusted pretax earnings of around $64 million. Redwire has projected such earnings to reach $250 million by 2025.

“We are at the beginning of a second golden age of space, with substantial growth being driven by new business models that are economically and commercially feasible in the near term because of innovative technology and infrastructure like ours,” says Peter Cannito, chairman and CEO of Redwire. He is also an operating partner at AEI.

Meanwhile, Rocket Lab competitor Virgin Orbit announced Aug. 23 that it will go public in a deal with a SPAC called NextGen Acquisition Corp. II. If successful, the deal should leave Long Beach, California-based Virgin Orbit with a pro forma enterprise value of around $3.2 billion. That includes $383 million from NextGen, assuming no significant redemptions, as well a combined $100 million from a private-investment-in--public-entity round from Boeing and AEI.

Virgin Orbit, a small-satellite-launch startup in aerospace entrepreneur Richard Branson’s portfolio, began operations this year (AW&ST, Jan. 25-Feb. 7, p. 24). The current SPAC phenomenon is thought to have started with Branson’s other space company, Virgin Galactic, in November 2019 when it went public via a blank-check company. “I’m very excited we are taking Virgin Orbit public, with the support of our partners at NextGen and our other wonderful investors,” Branson said in the latest deal announcement. “It’s another milestone for empowering all of those working today to build space technology that will positively change the world.”

According to investor materials, Virgin Orbit has $300 million in active contracts and expects another $1.3 billion worth of active proposals, along with $2.3 billion worth of “identified opportunities.” Virgin Orbit forecast it will produce almost $2.1 billion in annual revenue by 2026, up from $15 million in expected revenue this year, a 166% compound annual growth rate.

Of that total, $436 million would come from so-called space solutions, $789 million from commercial and civil launch business and $838 million from national security and defense business. By the end of 2026, the materials forecast pretax earnings of $854 million. But the company forecasts annual operating losses through 2023 until earnings reach the black in 2024.

Of note, buried in the SPAC transaction was news that Virgin Orbit apparently will build and offer a fleet of its own Earth-observation and Internet of Things satellites starting in 2023. Virgin Orbit’s “satellite as a service” offering will focus on connectivity for ocean ship management, aircraft, pipeline monitoring and intelligent agriculture.

The startup expects to devote a quarter of its proceeds from business operations and investments to develop the satellite system in 2021-23. The goal is for full fleet build-out to be completed after 2023. The Virgin Orbit approach also entails investments in complementary constellations. Partner agreements for the space-enabled data and analytical services have been made with Arqit, BigBear.ai, Redwire, HyperSat and SAS. The system will offer electro--optical, synthetic aperture radar and infrared-hyperspectral imagery.

To differentiate its service, Virgin Orbit will lean on its air-launch system’s seemingly easier and locale-friendly approach to lofting satellites off the ground via aircraft, rather than Rocket Lab’s, Astra’s or other fixed-base rocket systems. That method could allow allies and approved nation states to have full local, legal control over the fleets—and resulting data—launched from their own runways.

While the current space SPAC surge is less than two years old, the trend first emerged with Iridium in 2008 when it raised $324 million through a merger with a SPAC called GHL Acquisition. Then came Virgin Galactic, and this year already has seen the debut of AST Spacemobile, Astra Space and Spire Global. Several more, including those mentioned above, are slated to occur over the next four months.

Industry observers say the trend is gathering steam as candidate companies once thought to be more late-stage venture-capital-bound now are jumping to publicly traded marketplaces. For startups in capital-intensive industries such as those operating in space, tapping public capital—including a pandemic-led generation of do-it-yourself investors—is attractive as a way of suddenly infusing long-term plans with enough funding to make them real, instead of wallowing through the traditional “valley of death” between proposal and production.

“SPACs are particularly suited to markets with long-term investment plans,” consulting firm Avascent states in an Aug. 23 report. “Investor pitches can focus on projected future revenues and build hype around companies with limited current revenues that would typically not be able to go through the traditional initial public offering (IPO) route. Low interest rates have made longer-duration investments even more tenable, and the New Space industry checks all the boxes.”

Still, one notable side effect from the space SPAC surge is that while all the startups fall within the new-space sector, they are targeting very different marketplaces with widely dissimilar offerings. For investors, it means new opportunities to value significantly different market niches and companies almost overnight. That is both exciting and perilous for those making investments.

“As publicly traded pure-play space companies proliferate and successfully de-SPAC, they begin to establish public market values for subsectors where none existed before (e.g. small-launch, proliferated constellations, infrastructure and payloads),” the Avascent group says. “For many, this will look like the old ‘if you build it they will come’ adage. But to answer one adage with another, ‘not all SPACs are created equal.’”

Experts continue to urge potential investors to do their due diligence before investing in SPAC deals. Good questions to ask include: Does the startup have revenue and contracted customers or just product offerings? Is the addressable market large enough to entail growth? Is a specific startup differentiated enough from competitors? Do they have an experienced management team in the sector? Last but not least, is the marketplace really new, or can it be addressed by other more established industries.

One thing is certain: Investors will have plenty of opportunity to ponder and act on these and other questions in the coming months.