Ben Goldstein, Lori Ranson The terrorist attacks of Sept. 11, 2001, changed the airline industry forever. The pandemic will, too.

Ben Goldstein, Lori Ranson

Airline and airport employees held a candlelight vigil at Dulles International Airport on Sept. 14, 2001, the first night of operations after the terrorist attacks three days earlier. Credit: George Hamlin.

The tragic events of Sept. 11, 2001, quickly accelerated a brewing recession in the U.S. and ushered in what Southwest Airlines CEO Gary Kelly regularly refers to as “the lost decade” for the country’s airlines. That 10-year period was peppered with one crisis after another—the severe acute respiratory syndrome (SARS) and H1N1 viruses, volcanic ash clouds and the global financial crisis.

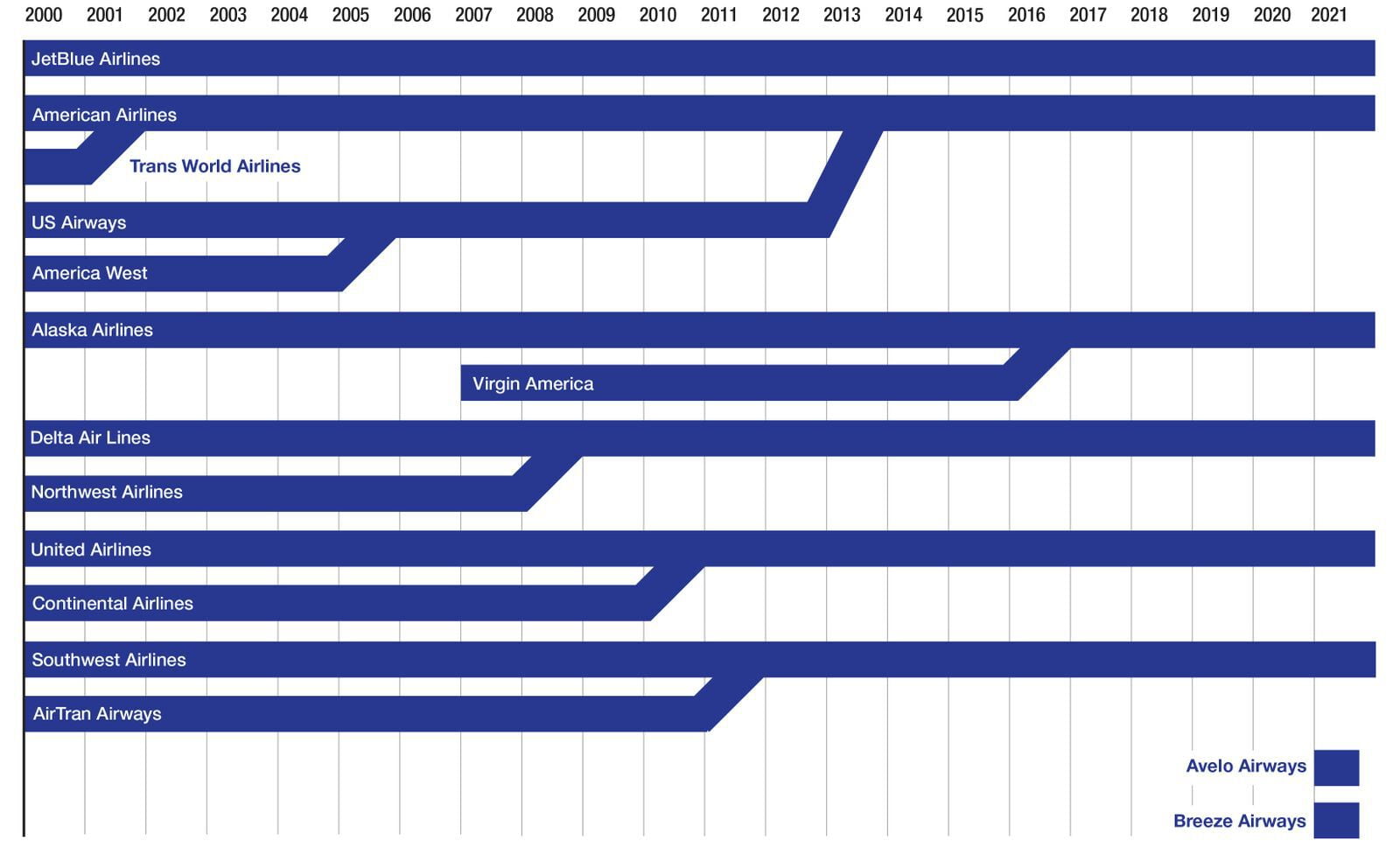

As a result, from 2000 to 2013, brands such as AirTran Airways, Aloha Airlines, America West Airlines, ATA Airlines, Continental Airlines, Northwest Airlines and US Airways either ceased operating or were swept up in the ensuing wave of consolidation that followed numerous bankruptcy filings in the U.S. airline industry (see graphic below). At the same time, Southwest Airlines and other low-cost carriers (LCC) took advantage of major airline bankruptcies and consolidation to build strength and inject new levels of competition into the marketplace.

Now, 20 years after 9/11, the global industry is battling the COVID-19 pandemic, which has shaped up to be the worst crisis in the history of commercial aviation. But the difference between then and now is that U.S. airlines are poised to recover more rapidly due to better financial footing.

Data from Airlines for America (A4A) shows the U.S. airline industry’s pretax margin from 2010 to 2019 was 7.1%. While still below that of other industries, airline pretax margins improved to 9.6% in 2017-19, reflecting growing momentum before the pandemic upended the global aviation sector.

A4A also calculates that U.S. airlines retired $91 billion in debt and returned $56 billion to shareholders between 2010 and 2019. Cowen & Co. analyst Helane Becker concludes that airlines entered 2020 “in arguably the best financial position they’d been in, because they spent the prior decade repairing their balance sheets.”

Both after 9/11 and in the early days of the COVID-19 pandemic, the U.S. government moved quickly to create financial support for the airline sector. But the major difference in the pandemic aid is the Payroll Support Program (PSP), the airline jobs initiative that has been deemed a major success by executives and unions alike.

U.S. carriers have received nearly $54 billion in PSP grants during the pandemic. The total aid from the government related to COVID-19 is in the ballpark of $80 billion, including tax relief, grants and loans. After 9/11, by contrast, government support consisted of $5 billion in direct grants and $10 billion in loans.

“The PSP has been a lifeline to the industry,” A4A CEO Nicholas Calio said in testimony to Congress earlier this year. He described the PSP as the “single most successful part of the CARES [Coronavirus Aid, Relief, and Economic Security] Act.”

Joe DePete, president of the Air Line Pilots Association, joined Calio in lamenting how the Airline Transportation Safety and System Stabilization Act passed by Congress after 9/11 contained no employee protections. DePete said carriers that were able to access assistance “paid off their shareholders while essentially no money flowed through frontline employees.”

DePete said the government-run entity overseeing that financial assistance, the Air Transportation Stabilization Board, “used its credit instruments to wrest disproportionate wage and benefit concessions from workers, effectively entering the government into private sector collective bargaining to change labor contracts.”

The PSP, by contrast, “is without a doubt, the most historic worker-forward, critical bridge to recovery,” he added.

Becker notes that when traffic declined 20 years ago because of terrorism fears, “the government picked the winners and losers.” For example, America West received aid while United Airlines did not, forcing United to file for bankruptcy in 2002.

“This time around, everyone got money and survived,” Becker says.

Carlos Ozores, vice president and managing director of aviation at consultancy ICF, says the biggest winners from government aid during the pandemic have been airlines, organized labor and shareholders.

“U.S. airline stocks have largely recovered from the sharp fall in March 2020,” Ozores says. “Without government bailouts, it’s possible that certain U.S. majors would have eventually filed for bankruptcy, which would have wiped out equity.”

He also cautions that it is far too soon to issue a verdict on the success of the government support—given that international travel continues to be highly restricted and concerns remain over the COVID-19 delta variant and other further mutations that could dampen domestic recovery.

U.S. airlines' cost per available seat mile remained largely flat after the terrorist attacks, while revenue per available seat mile fell by 15% in 2002, compared with 2000, and remained down 10% in 2003-04, Ozores says. A recovery did not occur until 2006.

Ozores says a revenue shortfall also helped contribute to the wave of U.S. airline bankruptcies during the period after 9/11.

A big question for the industry now, he notes, is how revenues will recover. “Our view is that the traffic recovery will be a multiyear affair, marginally faster than the recovery from 9/11,” Ozores says. “But the jury is still out on the revenue recovery, and there is a strong case to be made that a slow recovery in business travel—some of which will not come back—and international travel will generate revenue headwinds.”

Even though airlines were able to maintain a solid portion of their employment rosters, overall employee counts have declined as carriers negotiated voluntary furloughs and early retirements during the pandemic. Calio said that 50,000 employees have opted for early retirement or other forms of voluntary separation since the start of the pandemic, while more than 100,000 opted for voluntary unpaid leaves of absence or voluntary compensation adjustments, “which has brought much needed flexibility,” he noted.

Airlines are also working to pay off massive amounts of debt they accumulated to fortify their balance sheets to withstand the pandemic crisis. The latest data from A4A projects that collective year-end debt totals for Alaska Airlines, Allegiant Air, American Airlines, Delta Air Lines, Hawaiian Airlines, JetBlue Airways, Southwest, Spirit Airlines and United grew to $163 billion in 2020 from $105 billion in 2019. The forecast for 2021 is $171 billion, and projected net interest expense for the year is $5.6 billion.

As carriers return to profitability, their top priority is to pay down that debt. But at the same time, they face the task of ensuring that their balance sheets are fortified for the next crisis.

Calio explained that in March 2020, airlines were prepared for an economic effect similar to what was seen following 9/11. “But the time has come again for airlines to rethink how they manage balance sheets broadly—and cash specifically—to withstand a future crisis of the unprecedented magnitude of COVID-19,” he said.

Prior to 9/11, Calio said the rule of thumb was to keep 10-15% of trailing 12-month revenue in the form of cash. After 9/11, those levels increased to 20-25%. “It has yet to be determined what the right metric is, let alone the right amount, but it is certainly something that will be seriously evaluated,” he said.

With the delta variant beginning to cast some clouds over the U.S. domestic airline recovery, operators may choose to keep their cash balances higher as 2021 remains a transition year for the U.S. airline industry.

But given where airlines were 20 years ago and where they are today, there is some reason to be hopeful. “Going forward, we think airlines will be better prepared for recessions than they were in the past,” Cowen & Co.’s Becker said during an industry presentation earlier this year. “So the next time an unforeseen event occurs, they’ll be able to quickly implement the learnings of the last year.”

The years following 9/11 were also characterized by the gradual transfer of market share from network carriers to LCCs, and no carrier illustrated this trend better than Southwest.

Along with LCC upstart JetBlue, Southwest expanded deep into legacy airline strongholds on the East Coast during the first decade of the 2000s, exploiting a sizable unit-cost advantage to attract customers away from large hub airports. By January 2002, the Dallas-based carrier’s market capitalization was greater than that of all the country’s network airlines combined, as investors wagered that the 21st century would increasingly favor the LCC business model.

While 9/11 helped accelerate the shift toward LCCs, in reality that trend was already well underway and being driven by several converging factors before the terrorist attacks. On the technology front, the internet disrupted airline pricing models by making ticket prices transparent to the consumer. Meanwhile, network carriers also finished negotiating a new round of expensive labor contracts by the first half of 2001, which further expanded the unit-cost gap between them and the LCCs.

From 1995 to 2009, the size of the gap in unit costs between Southwest and the network carriers grew to 30.4%, according to a report from the Swelbar-Zhong Consultancy. Bankruptcy court assistance helped legacy airlines narrow that gap substantially. Between 2010 and 2014, the unit-cost differential shrunk to 9.2% before widening slightly to 12.6% from 2015 to 2019.

“One could say that 9/11 was the coming out party for the LCCs, even Southwest,” Bill Swelbar, co-founder of Swelbar-Zhong Consultancy, tells Aviation Week. “The LCCs took full advantage of the labor-cost differentials and used the competitive advantage to price their product aggressively. The opportunity resulted in a meaningful market share grab by the lower-cost sector.”

Since around 2015, however, Southwest has found itself increasingly on the defensive, threatened by the rise of a newer generation of ultra-LCCs (ULCC), including Allegiant Air, Frontier Airlines and Spirit Airlines. While Southwest’s unit-cost gap has narrowed in comparison to the legacy airlines, it has grown compared with the ULCCs. The Swelbar-Zhong report shows that from 2015 to 2019, the gap between Southwest and the ULCCs reached 34.8%, compared with a 42.1% gap between the network airlines and ULCCs.

Swelbar expects that ULCCs will exploit their rock-bottom cost structures to take on both Southwest and the network carriers in the post-COVID-era, aided by the strong recovery of leisure demand relative to corporate and long-haul international traffic.

“Just as Southwest took full advantage of its unit-cost benefit versus the network carriers after 9/11, the ULCCs will use their cost advantages to grow at the expense of both the network carriers and Southwest in a post-COVID world,” Swelbar says. “Southwest is no longer the low-cost provider it was during the 1990s and 2000s. It still can be a price disciplinarian, given the scope and scale of its domestic network, but it has less room on the pricing side than it did, as its unit-cost advantage has eroded over time.”

One of the key differences between the 9/11 and COVID-19 demand shocks, however, is the effect on business travel. While 9/11 disrupted demand for leisure travel, business travel demand remained mostly intact, and the global economy continued to chug along. This time the opposite is true: Leisure demand has fully recovered in the U.S., but corporate volumes are down around 60% from 2019 levels.

While business travel is expected to continue to rebound in the months ahead, there is a broad consensus that at least some types of corporate travel—namely intracompany travel—will be permanently replaced by video-conferencing technology.

“COVID is having a far greater impact on business travel [than 9/11], at least in the short run,” George Hamlin, president of Hamlin Transportation Consulting, tells Aviation Week. “After 9/11, business travel was chomping at the bit to get going again. If anything, it was the leisure travelers who were most worried about their safety. This time, the opposite is true.”

The reduced pool of corporate travelers will cause legacy airlines to have to adapt to a weaker revenue environment in the coming years, with lower fares leading to structurally lower yields compared with pre-pandemic levels. That could, in turn, lead to a greater emphasis on capacity discipline across the industry, as full-service carriers look to boost yields by keeping a tight lid on supply.

“Average yields, over the short run, are going to be noticeably lower than what we’re used to,” Hamlin says. “This is going to make it very tough on the legacies, and I think they’re going to need to adjust capacity downward.”

The years following 9/11 caused airlines to curb nearly 50% of their short-haul flying, classified as trips under 500 mi., according to the Swelbar-Zhong report. Now, with carriers chasing a smaller pool of travelers, small-community air service could once again be at risk. Exacerbating the trend is a shift in the market away from 50-seat regional jets used to serve many smaller cities over the past two decades.

During the pandemic, air service levels to small communities have been artificially supported by the terms of the CARES Act, which requires carriers to continue serving most points in their pre-pandemic networks. Once that requirement lapses on Oct. 1, Swelbar predicts that small-community air service will reemerge as a key political issue in Washington.

“There are 455 commercial air service airports that have fewer seats today than they had in 2019,” Swelbar says. “If the U.S. domestic industry will be smaller, as the network carriers have suggested, then it is hard to imagine every dot on the 2019 map being on the 2023 map after the dust settles and the CARES Act money is no longer artificially protecting all airports served.”

Hamlin agrees that the move away from small regional jets could mean that some smaller cities will lose commercial air service in coming years.

“Smaller cities served by regional aircraft are going to have less service [and] less competition,” Hamlin says. “And some of them may fall off the map.”

Somewhat paradoxically, while COVID-19 has had a much greater impact on airline finances than 9/11 did, the U.S. market likely will not see anything approaching the spate of bankruptcies and mergers that the terrorist attacks ushered in. This can be largely attributed to the industry’s much better financial condition and a hugely successful government aid program.

Additionally, the waves of mergers ushered in by 9/11 and the global financial crisis mean that there are simply fewer available targets for consolidation this time around. Virtually all the network carriers have already consolidated to some degree, and ULCCs with very different business models can be difficult to combine, either with each other or with network carriers.

Still, airlines will have to contend with an operating environment characterized by intense competition from ULCCs, weaker business travel, depressed yields and lower levels of service to small communities.

All indications point to competition being fierce as the story plays out over the next decade.

Editor's note: This article was updated to clarify the comparison of the impact on airline finances of the COVID-19 crisis and 9/11.