Michael Bruno A flurry of headlines makes it seem the middle of the A&D industry is going to dwindle to just a few companies.

Michael Bruno

Will the last midsize aerospace and defense manufacturing company please turn off the lights?

A flurry of recent headlines has made it sound as if the middle of the aerospace and defense (A&D) supply chain soon is going to dwindle to just a few companies:

Indeed, as perennial fears of an evaporating A&D industrial base flare anew, dealmakers on both sides of the Atlantic Ocean are watching closely to see what happens in the many ongoing deals. Proverbial water-cooler talk among consultants and executives centers on whether U.S. and UK officials will countermand the latest consolidation wave.

“Another one bites the dust,” is how seasoned analysts at Vertical Research Partners responded when the Parker bid for Meggitt was unveiled Aug. 2. “Goodrich, B/E Aerospace, Precision Castparts, Rockwell Collins, Cobham . . . and now Meggitt. The list of small/mid cap public A&D companies continues to shrink, even though the actual industry continues to grow.”

Yet therein lies the rub. New middle-market players actually are emerging, albeit most of them privately held and without brand-name cachet to match more venerable names that are merging or being taken private. The common thread in the latest wave of mergers and acquisitions (M&A) to roll over A&D has been long-term growth prospects for companies and dealmaking opportunities triggered by the fallout of COVID-19.

“Pre-COVID, it was all about value creation, high [deal] multiples [and whether] the supercycle [was] still going,” says Alex Krutz, managing director of Patriot Industrial Partners. “Now I see it as more opportunistic and necessity-based.”

“Everybody’s been affected—the Tiers 2, 3 and 4 particularly,” echoes Michel Merluzeau, director for market analysis at AirInsight Group.

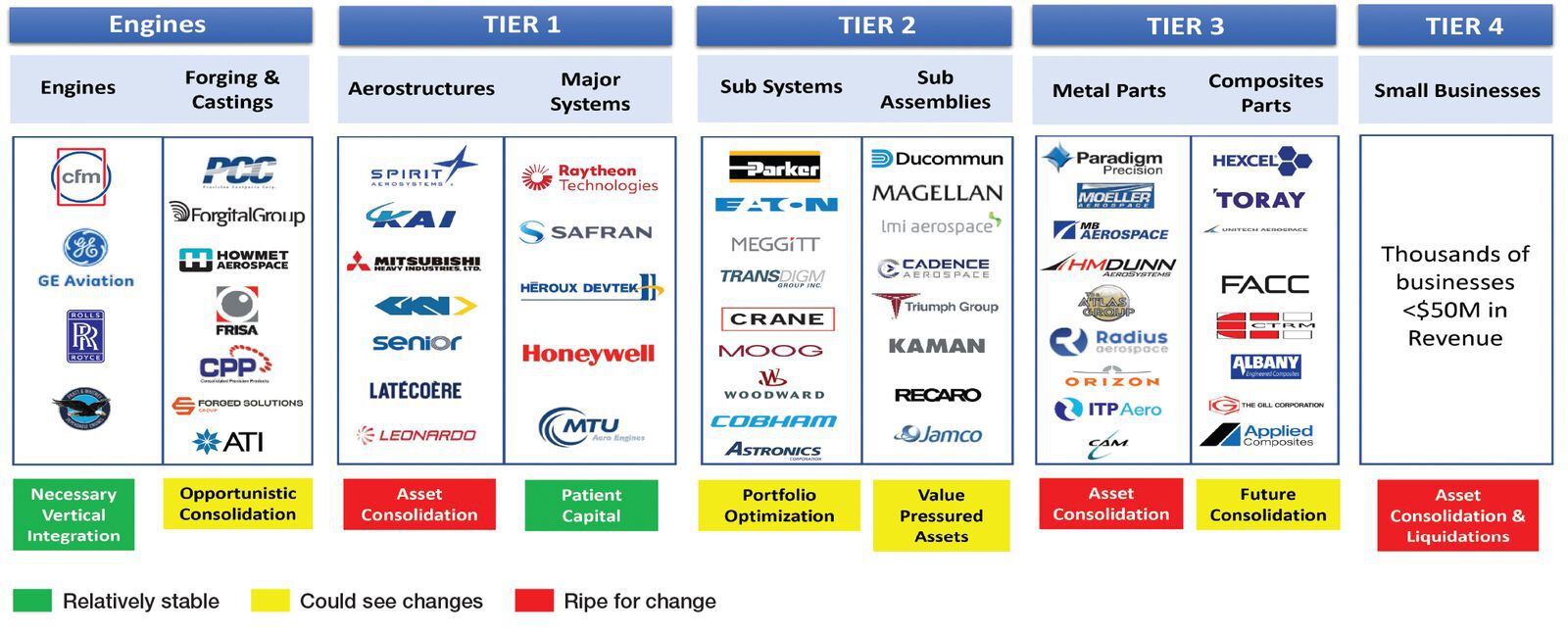

According to the industry consultants, M&A at the Tier 1 level will be driven by research, development and production of new programs. Those will drive Tier 2 suppliers into deals as well, but so will financial requirements. But Tiers 3 and 4 will be driven more by financial reasons and, part and parcel to that, governance and resource availability.

“There’s some level of consolidation likely between some of the Tier 2s into the Tier 1s,” says Merluzeau, declining to be more explicit because his firm is privy to dealmaking. “There’s definitely one or two European candidates there that are likely targets.”

Parker, Meggitt and others fall within the Tier 2 subsystems category that Krutz says is ripe for portfolio optimization. In a July 29 webinar with Merluzeau—before any of the news regarding a tie-up between Meggitt and either Parker or TransDigm emerged—Krutz highlighted the potential for “mergers of equal” within the group (see chart).

“There are a lot of good companies in that group and there are some that are maybe a bit challenged that have synergies that could align well with others in there,” he said. Parker especially seemed poised to create a new “super Tier 1,” coming off acquisitions of Exotic Metals Forming Co. and Lord in 2019 for a combined $5.4 billion, he added.

Ironically, there may be relatively fewer transactions like those as the post-pandemic recovery continues. To be sure, practically all A&D industry observers expect M&A activity to gain steam, and many say that should start now as coronavirus-related government aid runs out. But a slew of reasons suggest strategic M&A deals may trail activity by buyers outside legacy industry for a while.

Ultra Electronics may be a small/midsize publicly traded company, but it is a recognized defense electronics provider to allied nations, making it an obvious M&A player, analysts say. Credit: Ultra Electronics

For one thing, publicly traded A&D providers simply have less financial ability in the wake of the pandemic, according to a recently released report from Canaccord Genuity dealmakers. From the first quarter of 2019 to the same quarter of 2021, so-called “dry powder” in A&D plummeted about 88% as COVID-19 “greatly” deteriorated the financial health of many companies—particularly those with commercial aviation exposure, which was the favored end market in recent decades.

Along those lines, A&D public company dry powder (a metric calculated as three times pretax earnings minus total debt plus cash and short-term investments) was just above $16 billion at the end of the first quarter this year.

By comparison, total private equity dry powder surpassed $1.6 trillion at the end of 2020, the Canaccord Genuity report from John Stack, Dan Coyne and David Istock notes, as the number of private equity funds exceeds 4,000 worldwide. Driving that in part is strong, easy fund raising due to low interest rates and government stimulus.

Specifically in A&D, private equity investment has doubled over the past five years, according to the Canaccord report. Of the 233 A&D portfolio companies owned by private equity as of June 30, 53 have been owned at least five years, with 14 held for longer than 10 years—a milestone representing likely sale candidates.

Another trend remaking A&D ownership is the advent of special-purpose acquisition companies (SPAC) and the quick-to-market opportunities they offer for A&D startups or privately held established players to become publicly traded.

“SPAC deals have started to permeate the landscape and will likely continue their presence for the near term,” states the latest regular Mesirow report from dealmakers Andrew Carolus and Adam Oakley. Four out of the top 10 A&D deals in the first half of 2021 were SPAC transactions, they note.

Perhaps another reason why there may be relatively less strategic M&A action is that there are fewer players to pair. Industry consolidation has been running rampant over the last decade, with numerous names disappearing from the marketplace. In turn, each successive strategic deal is that much harder to justify and close.

Punctuating that last point is new skepticism voiced by the Biden administration. In July, President Joe Biden issued an executive order that aims to promote business competition, in part by setting a higher bar for allowing further consolidation. Most immediately, it could affect Lockheed’s proposed $4.4 billion acquisition of Aerojet, one of Lockheed’s leading suppliers for air and space propulsion programs. Observers took note in August when new Federal Trade Commission (FTC) Chair Lina Khan sent a letter of response to Sen. Elizabeth Warren (D-Mass.), a vocal opponent of big-business mergers.

Khan’s response indicated exasperation with a longstanding practice of requiring merged behemoths to allow competitive access to products, as well as suggesting that size matters.

“I am skeptical that behavioral remedies alone are sufficient to prevent a vertical merger from causing harm,” Khan said. “This is especially true for vertical mergers involving large firms with substantial market power at one or more levels of the supply chain. The larger the market share, the higher the risk that a vertical merger will result in a reduction of competition post-merger. For that reason, I prefer structural remedies that prevent the harmful integration of assets or would support the commission moving to block the merger altogether.”

In turn, analysts said they thought Lockheed’s successful takeover of Aerojet was now in jeopardy. Capital Alpha Partners expert Byron Callan recast the deal’s prospects at just 25% after the Khan letter, down from 55% before. Still, it does not necessarily dampen vertical integration across A&D, he further said.

“If new civilian leadership in the Defense Department does not support the deal and [the] FTC blocks it, we don’t see it as a game changer for the defense sector,” Callan said Aug. 12. “Aerojet Rocketdyne is somewhat unique because of its position as a key supplier to Lockheed Martin and Raytheon Technologies on missile and space programs. We can’t think of another independent company the size of Aerojet Rocketdyne, or larger, that plays the same role as a critical supplier to multiple primes that would trigger vertical integration concerns.”

What is more, many industry observers say, strategic deals will continue for many of the same underlying reasons that spur private investors, SPACs and other alternative financing in A&D. Various macroeconomic reasons make dealmaking attractive, such as low interest rates, high stock prices, accumulated cash hordes thanks in part to government stimulus, and the continuing business effects of the pandemic. Above all, there remains a deep-seated belief in the A&D industry’s prospects. So what better time than now or in the near term for sweeping up valuable assets?

“It is notable that some names we have analyzed for many years (35 years for Meggitt and Cobham, over 20 years for Ultra Electronics) are being subject to genuine bids for the first time and all at the same time,” says Nick Cunningham of Agency Partners. “This is mainly about the very low cost of capital in our view, especially given the £35 [($48) per share] bid for Ultra, which compares to an all-time high of £25. In other words, it’s not because they are suddenly cheap.”