The airline industry anticipated a strong rebound in 2022, but more border closures and restrictions will make that harder to achieve.

Jens Flottau

When the Biden administration lifted restrictions on transatlantic air travel in November, many in the airline industry saw it as the beginning of the end of the novel coronavirus crisis. After all, with one of the biggest air transport markets back online, wouldn’t other governments likely end their own travel bans, finally giving airlines everywhere the opportunity for a comeback?

Some travel bans will be eased, certainly. But as the industry heads into 2022, more signs are emerging that it will be a long and winding road back to full recovery, with unpredictable speed bumps that could slow trends temporarily and regionally at least. Parts of Europe have seen an unprecedented surge in new coronavirus cases over the past few weeks, leading to some new lockdowns. The U.S. government warned against travel to Austria, Belgium, Denmark, Germany and Hungary as a result—an alert typically reserved for countries fighting civil wars. Restrictions remain in place in large parts of the Asia-Pacific region, even though China is expected to open up conditionally for the 2022 Winter Olympic Games.

And globally, discovery of the new COVID-19 omicron variant has led to a wave of restrictions and border closures, renewing concerns that the recovery of the air transport industry may stall or even be reversed.

Where travel is possible, numerous rules about testing and vaccinations are in place, and they typically differ for every country.

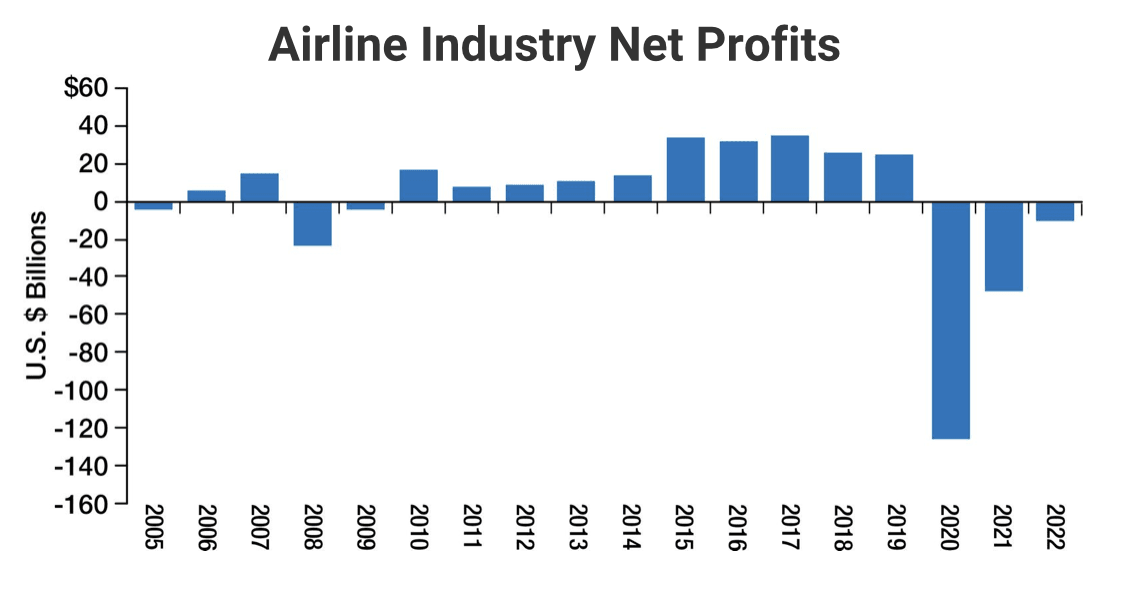

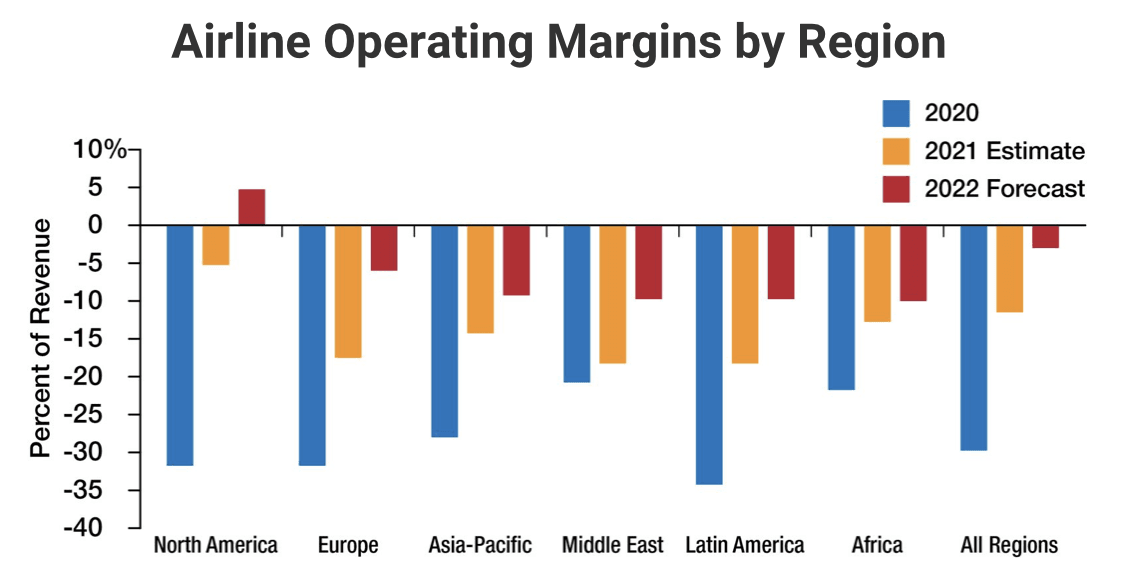

The International Air Transport Association (IATA) estimated in October that the airline industry will lose around $201 billion in 2020, 2021 and 2022. As a whole, it will not return to profitability until 2023, and North America will be the only profitable region in 2022. Overall, airlines will suffer another $11.6 billion net loss, following an estimated $51 billion loss in 2021, according to the most recent forecast (see chart). Should omicron have a serious and lasting impact, the outlook will be much worse.

Source: IATA Economics Airline Industry Financial Forecast Update, October 2021

Many airlines, including essentially all of the blue-chip carriers, have been on the brink of bankruptcy at some point since March 2020. Close to $250 billion in government financial support has kept companies afloat. But that support has been distributed unevenly, with most of it going to U.S., European and Asian airlines. There has been little if any such support for African and Latin American airlines.

The adverse consequences of this situation in these regions will be felt well into 2022. Latin America’s biggest airline groups, LATAM Airlines and Avianca, continue to undergo formal bankruptcy processes and could emerge from them next year. Cuts to their workforces, fleets and overall cost bases have been deep, but some argue that this positions them well for the post-crisis phase. South African Airways,

one of the industry’s iconic brands, is being relaunched with new investor backing at a fraction of its former size and envisions deep cooperation with Kenya Airways. Ethiopian Airlines is threatened by another major setback beyond COVID-19: an ongoing civil war in its home country.

According to IATA, North American airlines will achieve a combined 2022 profit of $9.9 billion, but that will be almost entirely wiped out by a $9.2 billion loss from European airlines (see chart). Carriers in the Asia-Pacific region will come closer to breakeven with a $2.4 billion loss, whereas airlines in Africa (losing $1.5 billion), the Middle East ($4.6 billion) and Latin America ($3.7 billion) remain far from profitability.

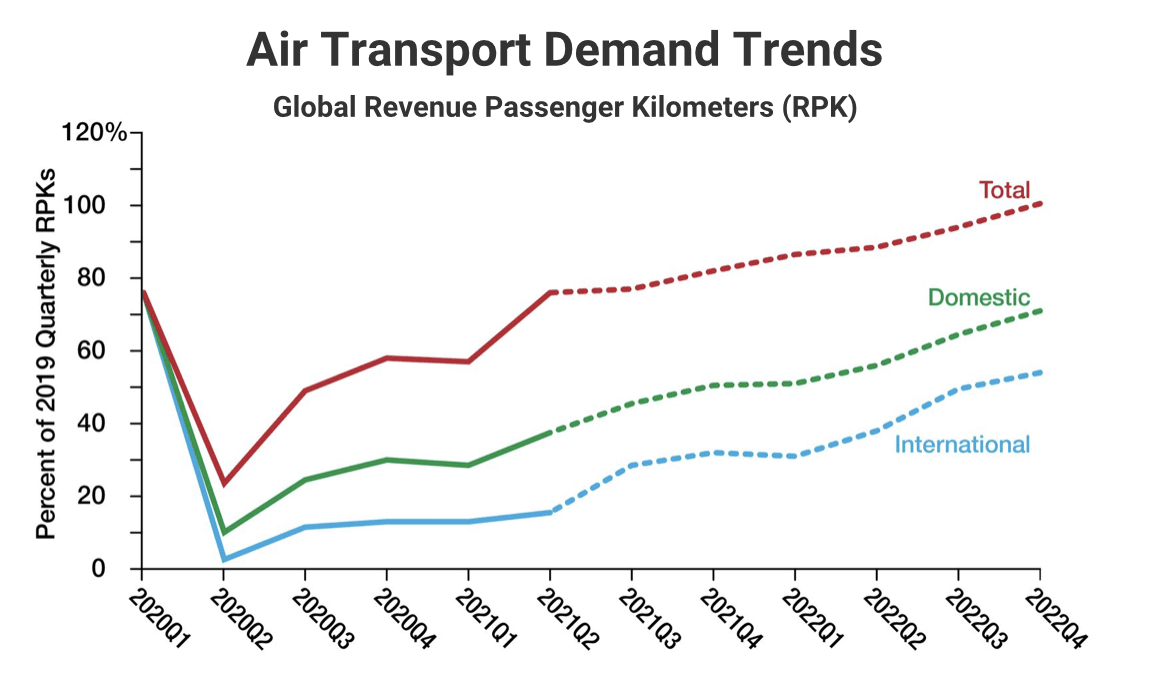

IATA estimates that traffic overall will return to 61% of 2019 levels in 2022, as measured in revenue passenger kilometers (RPK) (see chart). In 2021, the industry was at an average of just 40% of that level. Traffic will therefore grow by 50% if the predictions pan out. While there are signs in many regions that demand returns quickly when restrictions are relaxed, the industry is also facing massive cost headwinds for new aircraft, labor, fuel and infrastructure that are making the recovery harder to achieve.

When the pandemic initially unfolded in 2020, airlines cut aircraft deliveries in half, to 805 aircraft. The industry is expected to take 1,143 new aircraft in 2021, a figure that will jump to 1,622 in 2022, based on current contractual agreements. However, as demonstrated by the large number of parked aircraft, airlines have more than enough capacity already and may be reluctant to take on more, particularly if

financing remains challenging. IATA anticipates that “airlines will consider further cancellations or postponements,” the association writes in its most recent economic report. “The investment appetite for new aircraft is likely to remain subdued as the global demand for air travel is not expected to recover to pre-crisis levels before 2024.”

On the other hand, Airbus and Boeing are keen to raise production quickly and burn off parked inventory, particularly of the Boeing 737 MAX and 787. More behind-the-scenes debates about production levels are all but guaranteed.

Labor is another headache. Going into the crisis, almost three million people were employed by the airline industry globally. In 2020, half a million jobs were lost, and the rebuilding has only just begun—and only in some regions. IATA forecasts that employment will grow 10.8% next year. But hiring and training are turning out to be huge challenges. Some airlines have found that training staff is taking longer than expected, and former workers are not coming back to some carriers, having found more secure or better jobs elsewhere. The bottom line is that labor costs are likely to increase considerably, as supply cannot keep up with demand.

Another challenge is anticipating accurately the real level of passenger demand. While some airlines are struggling to find staff, there is also a risk of over-hiring if demand does not return as quickly as expected.

IATA forecasts that fuel prices will rise above 2019 levels next year as airline services grow back. In 2019, the average price per barrel of oil was $77. Given the traffic slump last year, the price dropped to $46.60 per barrel and rose back to $74.50 in the current year. In 2022, IATA projects that the price will increase slowly to almost $78. Based on the average price and the expected increase in the level of traffic, the industry is forecast to spend $132 billion on fuel in 2022, 32% more than in 2021. Fuel will also make up a growing share of airlines’ overall costs (19.5% versus 19% in 2021) but will remain below the 23.5% recorded in 2019.

Infrastructure costs are certain to rise, partly because of increasing traffic volumes but mostly as airports and air traffic management providers try to recover revenues lost in the pandemic. Some of the planned increases have set in motion a furious debate and were called “outrageous” by IATA Director General Willie Walsh. Luis Gallego, CEO of British Airways parent International Airlines Group (IAG), indicated that the group may have to reconsider its capacity plans for London Heathrow Airport, as airport fees there are planned to rise about 50%. In Germany, Lufthansa and other carriers are facing a near-doubling of air traffic control charges.

The recent Dubai Airshow provided a glimpse of what could be the airline industry’s future. The big Gulf carriers largely refrained from placing any new orders (or attending the show, for that matter); they instead renegotiated delivery schedules, deferrals or even cancellations of the huge commitments placed eight years earlier. Essentially all the orders for new aircraft in Dubai came from low-cost carriers (LCC) or from the lessor Air Lease Corp. (ALC), which is likely going to place a substantial part of its new aircraft with LCCs.

The air show in Dubai also showed that airlines are continuing their move up in average gauge, in spite of the short-term need to operate smaller aircraft in a down market. Indigo Partners bought 255 Airbus A321neos for the LCCs in its portfolio—Wizz Air, Frontier, JetSMART and Volaris.

Both Indigo Partners Managing Partner Bill Franke and ALC Executive Chairman Steve Udvar-Hazy pointed out that they were placing the orders now to lay the groundwork for years to come. Most of the aircraft will not be delivered until 2025 or later.

More of this strategizing could continue in 2022 as financially stronger carriers or lessors try to gain an advantage over their weakened competitors. This could come in the form of aircraft orders or—in the nearer term—intensifying activity in the leasing market, as long as rates are still attractive.

While there have been few bankruptcies—and complete market exits have been even more rare—consolidation has occurred, simply because many airlines have become a lot smaller and are not likely to return to their former size in the foreseeable future. Norwegian is a case in point: It charted a path of daring growth before the pandemic, aiming to break into the promising low-cost, long-haul segment that no one really had been able to make work profitably.

Now, after a brutal restructuring, what is left of Norwegian is a small LCC operating mainly in the Nordic countries, with moderate ambitions to grow back to a more sizable, but not long-haul, airline. Its competitors on both sides of the Atlantic are benefiting without having to do much themselves. Some, particularly U.S. carriers, have often acted differently in recent years. Delta Air Lines acquired stakes in LATAM Airlines, Aeromexico and Virgin Atlantic, while United invested in Avianca and Azul, but none of these moves paid off. It is therefore safe to assume that while consolidation will continue, airlines will be very careful about making any acquisitions, except in some unusual circumstances, such as the takeover of Asiana by its biggest rival, Korean Air.